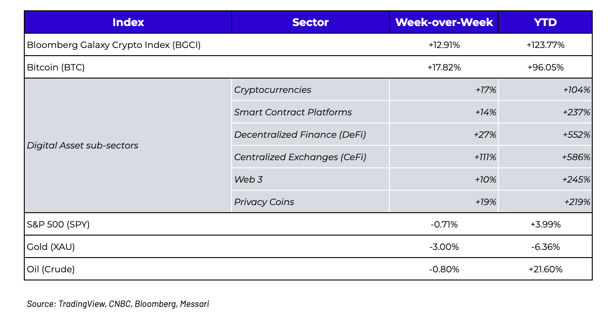

What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 2/21/21)

The Digital Assets Cash Shortage Has Led Leverage - But at Least it is Transparent

Like many terms in finance, the term “bubble” is thrown around way too carelessly. As Noelle Acheson of Coindesk pointed out recently, in her defense against Bitcoin bubble rhetoric, a bubble implies that the price of an asset is so far ahead of fundamentals or intrinsic value that it is infeasible for the asset to ever reach that valuation.

Just about every risk asset is showing strength this month, and it almost seems like a forgone conclusion at this point that this strength will continue. From equities to real estate to digital assets - you can certainly make an argument that prices are frothy, and perhaps even a bit stretched or overheated, but it is very difficult to definitively conclude that these valuations can’t and won’t eventually be justified by fundamentals. Instead, it’s possible that the market may simply be pulling forward inevitable long-term gains, thus reducing potential gains in the future. All of these asset classes have positive and growing fundamentals, so it is certainly feasible that valuations will catch up to price. Cheap? Probably not. Bubble? Most likely not.

That said, there is a difference between reaching for higher prices at stretched valuations, and desperately chasing higher returns with leverage. The market’s complete lack of fear, perhaps driven by 12 years of Fed-induced moral hazard, has resulted in some very scary charts.

The traditional finance world is awash with cash, yet it isn’t stopping market participants from wanting even more. According to the Felder Report, the level of margin debt has hit new highs, and the 9-month increase in the total amount of margin debt has also soared to a new record. Each of these peaks in margin debt has historically been met with a severe pullback in equity prices. These peaks can last a long time (i.e. is the current market 2006, or 2008), but they are definitely cause for concern. So much so in fact, Interactive Brokers Chairman Thomas Peterffy said financial markets came frighteningly close to breaking during last month’s Reddit-driven volatility. Between the repo failures in late 2019, and collateral / settlement failures of 2021, it certainly makes you wonder “what else don’t we know”?

Margin debt is at all time-highs

.png?width=563&name=unnamed%20(57).png)

.png?width=567&name=unnamed%20(58).png)

Traditional financial market participants are choosing to use leverage to amplify returns. In the digital assets arena, however, while leverage is also running rampant, it has historically been driven by a cash shortage more than a desire to amplify returns. Recall, there are no prime brokers in digital assets, and those that are trying to build these services still require a lot of collateral and very low loan-to-value ratios. Further, the market is so fragmented that in order to transact efficiently, you must hold collateral at a variety of exchanges and other trading venues, thus making it even more difficult to be productive with your capital. For example, an asset manager may be overcollateralized when measuring total assets, but at any one specific venue, they appear undercollateralized, as each exchange/dealer does not give the asset manager credit for assets that are not held directly with them. And finally, with all of the new entrants coming into the market, spot dealers are getting lifted so fast that they are offsides, often running out of both natural sellers and inventory.

This dynamic has resulted in a very robust and growing derivatives market. The growth in both the futures market and the options market has been phenomenal. The amount of open interest in Bitcoin and Ethereum options has risen over 1000% since the start of 2020, while OTC bilateral options are gaining traction in other large cap digital assets. Similarly, the growth in Bitcoin and Ethereum futures looks like a hockey stick, with BTC and ETH open interest quadrupling since 2020. And thanks to exchanges like Binance, FTX and Huobi, we are now seeing strong growth in futures open interest for other tokens as well (though this is harder to measure in a single graph).

Growth in Bitcoin and Ethereum Futures

Growth in Bitcoin and Ethereum Options

Source: Skew

This of course is a positive development, but it can also be abused. In the last few weeks, digital assets participants have turned greedy, perhaps because back-to-back-to-back weekly double-digit gains without a major setback encourages more aggressive behavior. Using Bitcoin as a proxy, the perpetual swaps funding rate, which is meant to encourage traders to take the opposite side to balance out risk, has been in positive territory for weeks, at one point costing traders as much as 100 bps per day for the right to stay long via futures (those who are short are thus paid 100 bps per day). Similarly, on the traditional futures curve, the annualized basis (spot/futures arbitrage) has been between 30-50% annualized in the front-month. In the options market, an at-the-money 1-week Bitcoin straddle costs $5500 (using $56k spot), implying almost a 10% break-even for one week. Lastly, borrowing US dollar stablecoins now costs as much as 10% annualized, as demand for dollar-based assets soars.

Surely a lot of this is speculation, but it’s also indicative of a real cash shortage. The traditional bank and brokerage world is still not fungible with digital assets, which means regardless of your total assets or cash, it's as if it doesn’t exist if it’s not fully integrated into the digital assets world. Moreover, unlike the shadow banking system in traditional finance, most of the leverage in digital assets is completely transparent. Of the three major ways to take on leverage (via DeFi, via OTC dealers, via exchanges), 2 out of 3 are on-chain and visible to the whole world if you know where to look, and the 3rd (OTC bilaterals) has the most onerous terms (overcollateralized).

Prices may be frothy, and there may be excessive leverage for the time being, but the growth is real. Bitcoin is hitting a tipping point in terms of adoption, and both user and revenue growth is driving the prices of pass-thru tokens in the gaming, DeFi, Web 3.0 and other sectors of digital assets. As such, there is a path to justify these prices, even if they are stretched today. The most likely event stopping the inevitable is an all-too-common leveraged, but likely short-lived, washout.

Source: Skew

Microstrategy Convert Opens the Door to More New Investors

Independent of your views on Michael Saylor, his sordid past, or his controversial Treasury management strategy, there is one undeniable positive about Microstrategy’s recent aggressive debt-fueled Bitcoin buying spree. By issuing another upsized $900 million of convertible bonds to buy Bitcoin, he is opening access to Bitcoin to perhaps the last remaining investor base that still does not have access --- fixed income investors.

We’ve highlighted previously how Bitcoin fits so many different investment buckets, and that no other asset in the world besides US Treasuries can be claimed by so many different types of investors. Bitcoin is now owned in some way by macro funds, equity funds, insurance companies, corporate treasurers, individual investors, central banks and plenty of other types of investors and users. Sometimes Bitcoin itself is being bought, and other times some proxy is being bought (like Grayscale’s GBTC, or publicly traded stocks with high BTC balances or correlations). But if you have a strict fixed income investing mandate, to date, you have been unable to participate in Bitcoin’s growth… that is, until Microstrategy began issuing converts to buy Bitcoin.

Whether Microstrategy is intentionally trying to become a “Bitcoin tracking stock” or a “backdoor ETF” is open to interpretation. And with a $9.4 billion equity market cap relative to just a $4.7 billion Bitcoin position, clearly you’d be better off just owning Bitcoin outright versus owning MSTR stock or converts as a proxy if your goal was just to own Bitcoin. But with Microstrategy’s low debt-to-cap ratio and high interest coverage, owning the MSTR convert as a “cheap call option” certainly has merit, especially if it’s the only game in town per your mandate. During the 2007 LBO craze, it was frowned upon to raise debt to pay equity dividends -- but the demand was there, so companies and investment banks took advantage of it anyway. Similarly, Microstrategy is taking advantage of an insatiable demand for Bitcoin, and Saylor is tapping into an audience that has previously been shut out.

Like it or not - it’s clever.

What’s Driving Token Prices?

With the whole market frothing, it is worth taking a step back and noticing the active rerating of both centralized exchange tokens (CeFi CEX) and Decentralized Exchange Tokens (DeFi DEX) due to the Coinbase Direct Listing announced on January 28th. Last week’s secondary market sale cleared at $373, implying a valuation of $100B (the first batch cleared at $200, ~$54B). This surge in demand for Coinbase shares points towards the increased demand for exposure in the digital asset market, as well as providing a surge in demand for all comparable digital assets:

- EXCH-PERP, a weighted index basket of exchange tokens (BNB, HT, OKB, LEO, and FTT), has been one of the best performers since the announcement of the direct listing:

- Since January 28th: +325% peak, +266% current

- Week over week: +93%

- Decentralized exchanges (DEX) also flourished:

- Uniswap (UNI)

- Since January 28th: +124% peak, +74% current

- Week over week: +38%

- Sushiswap (SUSHI)

- Since January 28th: +186% peak, +117% current

- Week over week: +16%

- Serum (SRM)

- Since January 28th: +194% peak, +125 current

- Week over week: +27%

- Using Bitcoin (BTC) and Ethereum (ETH) as a benchmark:

- Bitcoin (BTC)

- Since January 28th: +89% peak, +76% current

- Week over week: +18%

- Ethereum (ETH)

- Since January 28th: +65% peak, +43% current

- Week over week: +8%

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.png?width=391&name=unnamed%20(59).png)

.png?width=1076&name=pasted%20image%200%20(14).png)

.png?width=512&name=unnamed%20(60).png)

.png?width=512&name=unnamed%20(61).png)

.png?width=579&name=unnamed%20(62).png)

.png?width=571&name=unnamed%20(63).png)