What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 2/28/21)

A Rough End to Another Great Month for Digital Assets

In retrospect, it was inevitable. No, we’re not referring to the cryptic Elon Musk tweet about Bitcoin’s ascent, but rather the 20-30% broad-based decline in digital assets last week.

For months we’ve discussed the risks building in the digital assets market. The dollar had stopped declining, interest rates were rising, leverage was building, and valuations (for those tokens that can be valued) were beginning to look very stretched. For months, none of this mattered -- until it did. Last week we finally saw a healthy correction.

The broad risk asset selloff started with rates. After stronger than expected economic numbers and a dismal Treasury auction, Treasury bonds continued their decline to a point where the S&P 500 dividend yield is now below the yield on the 10-year note for the first time in 20 years. Not to be outdone, the total return for investment-grade corporate bonds is now -2.8% YTD, the worst start in over 40 years. As rates rise, leverage unwinds. The digital assets futures market saw 24-hour liquidations reach over $6 billion early in the week as token prices fell 20-30% -- for context, that’s more liquidiations than the entire amount liquidated in March 2020 when Bitcoin fell over 50% in a single day. Similarly, the famous “Grayscale premium” turned negative -- when securities trade below Net Asset Value, it’s yet another indication that speculation and leverage is beginning to taper.

While the token market sputtered, the king that rules them all rose. Shares of Coinbase actually rose week-over-week on the Nasdaq Secondary Market. As we wrote last week, Microstrategy converts opened up Bitcoin access to bond investors. Similarly, the Coinbase direct listing is going to open the door to equity investors. Clearly there is going to be a strong bid for Coinbase shares. Perhaps less obvious though is that this new Coinbase offering opens the door to new interpretations of fundamental valuation approaches. There are plenty of Coinbase competitors, all of whom have similar business models but very different capital structures. Some have equity but no tokens, others have tokens but no equity, and a select few have equity and a token.

As a result, the term “Enterprise value” has to be adapted to take into account that tokens are now undeniably part of many company’s capital structures. Equity is a claim on profits, debt is a claim on assets, but tokens are now a claim on network growth, governance and pass-thru revenue.

To understand what we think of the Coinbase equity valuation, and how this analysis fits within our overall enterprise value analysis, we turn it over to Arca Senior Analyst, Alex Woodard.

Insights from the Coinbase S-1

Written by Alex Woodard, Senior Arca Research Analyst

The big news last week came on Thursday with the release of the Coinbase S-1. This is a pivotal moment for digital assets and with it came much-anticipated insights into the exchange’s business. As expected, this has received coverage across the board as analysts and reporters dug into their financials. Larry Cermak from The Block quickly reported top-line items, and The Block continued to release insightful pieces on Coinbase both before and after.

After reviewing the S-1 ourselves, we point out the Good, the Bad, and the Ugly from the Coinbase S-1.

The Good

Coinbase is in no financial trouble. From a revenue standpoint, they saw Y-o-Y growth of 139% from $533m in 2019 to $1,277m in 2020. With an operating expense of $868m in 2020 and $579m in 2019, Coinbase created a net income of $322m in 2020 versus -$30m in 2019. This shows a healthy profit margin of 32% for 2020, especially when compared against other major exchanges. Nasdaq has a profit margin of 16% and ICE, the parent company of the New York Stock Exchange, has a profit margin of 25%. Like most tech companies, profit margins likely vary heavily compared to their more established counterparts in traditional finance as Coinbase continues to reinvest their cash flow in order to focus on growth. As a result, revenues/sales will be an important metric to track in order to justify future valuations when their common stock becomes publicly traded. Additionally, these margins will likely compress as trading fees on the retail side come down via increased competition, both from digital-asset native competitors and the inevitable entrance from traditional Wall Street firms. Coinbase’s current profit margin indicates that they should be able to handle that fee compression and still have the ability to be profitable depending on their amount of reinvestment.

In terms of Coinbase’s Balance Sheet, there are no clear risks that would put them under financial strain. They have $1.1b in Cash and Cash Equivalents, no long-term debt, and minimal long-term liabilities.

Source: Coinbase S-1

Coinbase has an adequate amount of Cash/Net Working Capital to continue to invest in their own growth. Additionally, if they were to issue debt in the future, they should have no issue making interest payments, especially if issued in the current market environment.

The Bad

Though Coinbase has been pushing their subscription services for the past few years, 96% of their revenues still come from trading volumes. As a result, Coinbase will likely be a highly cyclical business for the foreseeable future. These products do not diversify their revenues and would thus not protect their bottom line over an extended drawdown in trading volumes that would inevitably come with a token bear market.

.png?width=690&name=unnamed%20(70).png)

Source: Coinbase S-1

Because of this high reliance on trading volumes, Coinbase revenues are essentially a function of Monthly Transacting Users (MTU’s).

.png?width=512&name=unnamed%20(66).png)

Source: Coinbase S-1, internal calculations

With the highly speculative nature of digital assets, and the market still heavily being made up of momentum trading, MTU’s are highly correlated with the BTC price. Again, this makes sense with 65% of Coinbase trading volumes also coming from BTC and ETH.

.png?width=706&name=pasted%20image%200%20(15).png)

Source: Coinbase S-1, internal calculations

Thus, Coinbase’s revenues, profitability, and cash flows would be negatively impacted by a drawdown in the price of BTC, and this will likely lead to variable cash flows for the foreseeable future until they successfully de-risk the business through diversification of revenue streams via subscription services.

Though that might not come soon, it is coming. Institutional customers grew to 7000 in 2020, up from 1000 at the end of 2017. Coinbase Trading volumes have seen significant growth from institutional activity with Y-o-Y institutional volumes growing 91% while the median trading volumes grew 50% suggesting that institutions are making up a growing portion of their business and revenues. With companies like Microstrategy and Tesla using Coinbase to gain exposure on their balance sheets, institutions will likely turn to subscription services such as Coinbase Custody, further diversifying Coinbase’s revenues and vertically integrating its business model.

.png?width=612&name=unnamed%20(67).png)

Source: The Block

Given how traditional investors use Microstrategy’s stock as a synthetic way to gain exposure to BTC, Coinbase equity is likely to become a more pure-play way to express exposure to BTC due to its revenues essentially being a function of BTC’s price. This will likely add additional upside during a bull market, but could weigh heavily on the stock during a bear market.

One additional issue that Coinbase will have to grapple with is fee compression -- with 96% of their revenue coming from trading fees, they are at high risk of a margin compression as competition grows.

.png?width=485&name=unnamed%20(68).png)

Source: Coinbase

Coinbase’s main competitors, such as Binance and DEXs, have significantly less in terms of fees, while Robinhood offers “No maker-taker fee”. As such, Coinbase will likely have to ditch the 399bps on debit card purchases if they want to remain competitive in the long-run.

The Ugly

The S-1 offered significantly more insights into the composition of Coinbase’s corporate structure. Coinbase created a staggered board of directors structure, where different classes of directors serve different term lengths and have different election dates. Staggered boards can often have a similar effect as a “poison pill” in eliminating a hostile takeover or any real challenge to management. At the same time, they all but eliminate any room for activist investing and shareholder rights since an activist investor must wait multiple years and have successful proxy votes to install enough directors to have any real control over the company to enact often necessary changes.

Over the past few years, there has been a growing trend of redoing staggered boards to enact shareholder rights within a company. This is because “companies with such boards have been found to have a lower value, a greater likelihood of making acquisitions that are value-destroying, and a greater propensity to compensate executives without regard to whether they actually do a good job.”

Coinbase’s board of directors consists of world-class investors so we hope that this will not be the case, but management will have significantly more control, and shareholders will have fewer avenues to enact shareholder’s rights and changes in management if they are ever necessary due to the staggered board structure. Additionally, Coinbase has introduced dual-class voting rights. According to the S-1, “Holders of our Class A common stock are entitled to one vote per share, and holders of our Class B common stock are entitled to twenty votes per share, on all matters submitted to a vote of stockholders.” This is again designed to entrench management in the operations of Coinbase and give them significantly more control during shareholder votes.

Dual-Class voting rights are not new, but it is taken to an extreme for Coinbase. As of December 31, 2020, there are 21,035,491 shares issued and outstanding of Class A common stock, and 164,950,620 shares issued and outstanding of Class B common stock. This heavily skews towards management and the Board of Directors.

The takeaway: management will be around for a long time and shareholder rights activists will have an incredibly hard time enacting any change within Coinbase if the need ever arises.

The Opportunity Set for Coinbase going forward

Throughout the risk section of the S-1, Coinbase highlighted its plans to expand internationally. With interest in digital assets continuing to expand around the world, this makes a lot of sense from a business perspective. In 2020, only ~24% of revenue was derived outside of the US. Further expansion would allow Coinbase to continue to grow Revenues and compete on a global scale for lucrative trading volumes.

Source: Coinbase S-1

At the moment, very little of Coinbase’s PPE is segmented outside of the US. This indicates that in order to grow internationally, they will need to invest in infrastructure abroad. Coinbase has the Net Working Capital to do so, but between infrastructure and regulation, Coinbase will likely have heavy one-time expenses that will bring them in and out of profitability.

.png?width=628&name=image%20(31).png)

Source: Coinbase S-1

Overall, it can not be understated how much of a watershed moment Coinbase going public is for the digital assets industry. They are financially healthy and their Y-o-Y growth is outstanding. One, however, can feel slightly unenthused by the plain vanilla equity offering. Coinbase could have used its power and influence to force the world into owning digital assets by tokenizing its shares, thereby forcing equity investors to learn how to own and custody digital assets. Instead, they are enabling equity investors to continue to avoid learning how to actually use digital assets. Fortunately, there was an Easter Egg in the filing, setting up a potentially interesting future dynamic. This juicy line on page 68 of their risk section hints at potentially issuing a token in the future: “if we issue additional shares of capital stock, including in the form of blockchain tokens, in connection with customer reward or loyalty programs''. The only risk, in our opinion, would be to not go down this path.

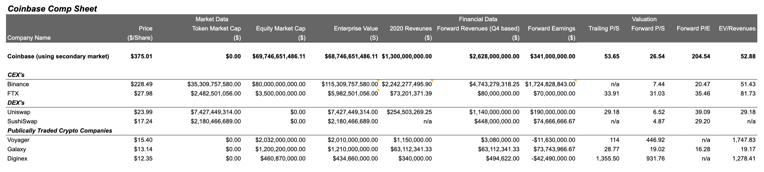

Enterprise Value -- A Case Study for Future MBA Students

With the Coinbase S-1, we now have clear insights into one of the largest digital asset exchanges in the world. However, it’s not very straightforward how you would use Coinbase equity as a comp to other large private exchanges that don’t necessarily have the same capital structure. In terms of Digital Asset exchanges, we have 3 very differing cap structures.

- There is Coinbase where cash flows directly to equity holders

- There are DEX’s such as Sushiswap and Uniswap (once the fee-switch is live) where cash flows directly to the token

- And then there are CEFI exchanges that have both an equity structure and tokens, where value flows to both

So how do you compare apples to oranges to bananas outside of strictly looking at volumes? One technique we have been utilizing at Arca is to look at the Enterprise Value of these businesses, combining both the market cap of the token with an estimated equity value in the private exchange.

Source: Coinbase S-1, internal Arca estimates

This is riddled with assumptions. For instance, what is the private equity of other exchanges worth? Well FTX CEO Sam Bankman recently told the Block that FTX is worth $3.5b with $80m in revenues and $70m in profits. In terms of Binance, it is still a guessing game, but their volumes far exceed Coinbase and they don’t have the same regulatory overhang that Coinbase must operate in, giving us a good guess as to what its equity valuation might be. A similar valuation to Coinbase at $80b does not seem unreasonable. Additionally, we don’t have any insights on either company’s cash or debt to actually follow a traditional Enterprise Value calculation, but this seems like a half-decent place to start when creating a comp sheet.

There are lots of questions, and lots of assumptions. But as we have discussed in the past, we believe every company will introduce a token into its cap structure in the near future. As such, we need to start thinking through a new type of financial analysis that takes into account new securities and evolving balance sheets.

Disclosure: Arca is an investor in BNB, FTT, UNI, and SUSHI.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.png?width=498&name=unnamed%20(64).png)

.png?width=1814&name=image%20(30).png)

.png?width=628&name=image%20(32).png)