What happened this week in the Crypto markets?

We’ll Get to Bitcoin in a Minute, but Let’s Not Ignore the Full Blown “Risk-on” Rally

You may have heard… Bitcoin jumped 25% last week. Everyone from full-time crypto enthusiasts to the most casual and uninvested observer took notice.

Despite what you may have read from journalists who attempted to pinpoint the exact cause of the rally, it’s important to note that this rally actually began 3 months ago. The media’s obsession with Bitcoin is understandable, given the size and importance of this currency, but an entire crypto ecosystem lives under the radar. For those that read “That’s Our Two Satoshis” every week, this sudden spike was actually foreshadowed by the price action of other crypto assets months ago, and the positive sentiment that has been built over this time. Said another way, this Bitcoin explosion almost seemed inevitable, even if the violent speed and size of the move still caught everyone off guard.

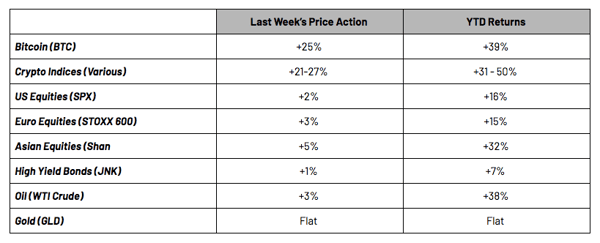

Before we dive deeper into crypto, however, let’s not lose sight of the fact that we are now in a full-blown “Risk-on” environment across the board. Take a look at the week-over-week numbers below and you'll see that this is a risk-on rally of massive proportions. Crypto, equities, commodities, high yield debt, and everything else that isn't nailed down is simply flying. Meanwhile, as investors’ risk appetites explode, the Treasury yield curve steepened, quieting recent chatter about a potential recession.

And yet, President Trump still felt the need to throw gasoline on a bonfire.

So what actually happened to Bitcoin last week?

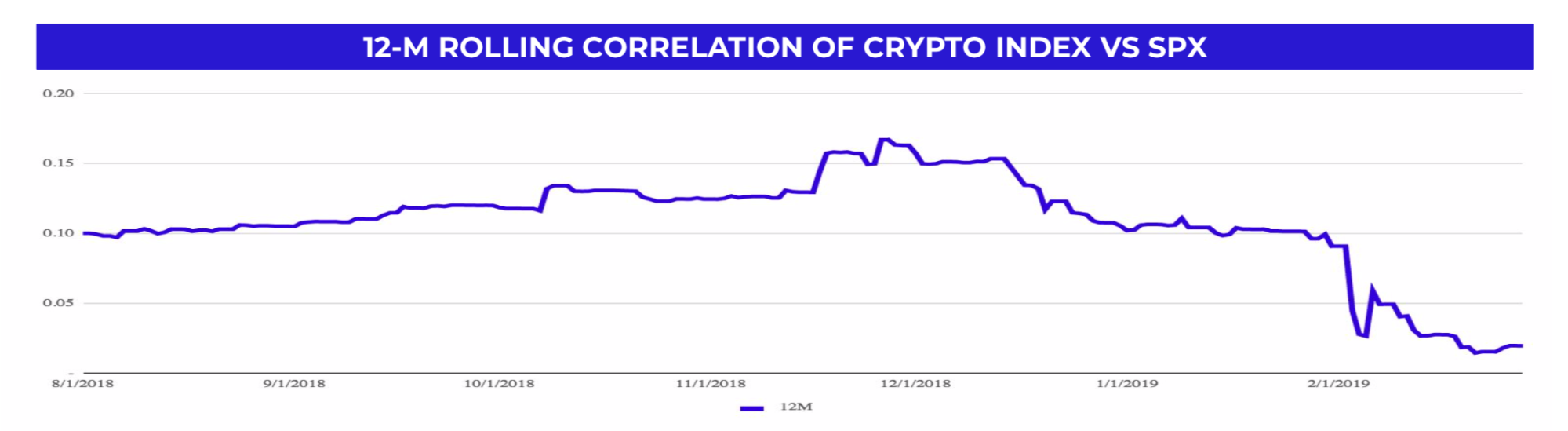

While the table above suggests all risk assets are highly correlated, in reality, the crypto markets have been completely uncorrelated to most other risk assets for the past 12 months.

Crypto Indices are still not correlated with US Stocks

Source: Data from General Risk Advisors

Source: Data from General Risk Advisors

As such, we believe the Bitcoin rally last week was fairly isolated to crypto. And this isolated asset class has been rallying long before last week’s explosion. In fact, the first quarter finished as one of the strongest on record, even if almost no one noticed. A flood of new money and companies entering the space, coupled with a fast growing infrastructure, has created a positive market environment that was already starting to spill over the top.

Last week the dam finally broke.

There have been a lot of hypotheses for why the dam broke (CME Futures expiration, large “Whales” purchasing, algos gone crazy, etc), but the simplest answer is usually the correct one. Just like any large spike up or down in any asset class, it’s caused by a simple buy or sell imbalance, and all of the positive factors mentioned above lead to this imbalance. The large magnitude of the moves in crypto over the last few days makes for an incredibly interesting story, and the headline number itself of a 25% week-over-week move is certainly unnatural, but it’s really not that different from any other asset class. Buyers outweighed sellers, and market makers felt the imbalance pressure so they took their markets higher, which triggered algos and stop losses, forcing liquidations, which added even more fuel to the buying pressure. Eventually, the price moves sparked retail buying, leading to even more buy interest that the market can’t fill.

Crypto makes more sense when compared to High Yield or Emerging Bond Markets

The Arca team has roots in many traditional asset classes, and the Crypto markets make a lot more sense when viewed through the lens of other illiquid markets like High-Yield bonds and Emerging Market bonds/equities, rather than comparing crypto to highly liquid benchmarks like Oil and US equities. These other illiquid asset classes “gap” up (or down) all the time on no liquidity, as market makers have to move their markets fast to avoid getting taken short (long) at levels where they know they can’t replace the risk. This happens until a new equilibrium occurs, similar to how a casino sports book will adjust their betting lines until they achieve equal betting activity on both sides. It just so happens that this new equilibrium for Bitcoin didn’t occur until prices moved up 25%.

Consider a high yield bond trader making markets in a very liquid bond (i.e. $2.6 bn outstanding, HCA 5.375% 2025). This bond may be liquid 90% of the time (like Bitcoin), but every once in awhile, there are just too many buyers, and the dealers can feel it coming. It starts like this:

HCA dealer makes a market 101-102 5x5, and immediately gets checked by 5 buyers who are willing to pay 101.5. The dealer can’t possibly sell to all 5 of these buyers simultaneously, so she pretends she already got lifted, and then moves her market to 101.5-103. But what happens if there are still buyers at 103, and no sellers in sight? Well, next stop is 104-106. A $2.6 billion issue may move up 5 pts or more without a single trade happening. Moreover, this can’t possibly only effect HCA. Inevitably, another dealer (or buyside investor) who is short HCA bonds is also long Tenet Healthcare bonds. So now that HCA just gapped up on no volume, it’s time to drive Tenet bonds higher to see if there is any resistance, and who is going to sell Tenet after seeing what just happened to HCA? Pretty soon, the entire High Yield market is up 5 pts on no volume.

So while Bitcoin has a $90 billion market cap, and you’d expect reasonable liquidity for something so large that trades on so many exchanges, the reality is, liquidity is only there until you need it. And short-sellers just learned a painful lesson on perceived liquidity. The overall size of the crypto market ($180 billion) is dwarfed by the size of the High Yield bond market ($2 trillion), yet these same market dances happen all the time without anyone batting an eye, effecting much greater wealth. The headline number is simply smaller (a 5% move doesn’t attract eyeballs in the same way as a 25% move does).

As a result, not only did Bitcoin gap higher, but large “out of favor” crypto assets like Litecoin (LTC), Ethereum Classic (ETC), Bitcoin Cash (BCH) and Stellar (XLM) also rallied, some moving 50-100% higher in a single week even if these “alt-coins” have less convicted buyers (they simply don’t have enough sellers). This price action may not seem healthy, but it may also continue until market participants feel the urge to take advantage of these higher prices.

What can we expect next for Crypto prices?

Rather than focusing on why Bitcoin and the rest of Crypto gapped higher, what matters more is what happens AFTER the rally. Thus far, most crypto investors haven’t felt the need to immediately sell into this strength. Calling a top or bottom is impossible, but focusing on probability weighted outcomes is more reliable. And the fact that investors have bought every small dip immediately over the past few months shows that the specter of sell-offs does not scare them. In fact, many are hoping for more sell-offs so they can buy assets at lower prices. This raises the near-term floor, which in turn gives investors even more confidence, leading to less selling.

Of course, this sentiment can change on a dime too. In February, the crypto market rally was led by real idiosyncratic events, as a few digital assets rose from the ashes and differentiated themselves from the pack (for example, LTC, RVN, ENJ, BNB all outperformed following specific catalysts). In March, many more digital assets played catchup, but for the most part, the "haves" still rallied more than the "have nots". All of this was orderly and made sense. But in April thus far, we've gone straight from lightspeed to ludicrous speed, and now everything is flying without a real rationale other than the buy imbalance outlined above. What we look for next is whether or not token-by-token differentiation can occur again at these higher levels.

What can ultimately derail this market?

Again, we look to the high yield bond market. Much like the LBO-fueled debt wave of 2007 and 2008, where large dealers were hung with huge amounts of bonds that they couldn’t sell and had to wait until market conditions improved before leaking these bonds out to the market, the same thing is about to occur in crypto. Many 2017 and 2018 ICOs are still “hung” on investors’ balance sheets. Most are mismarked, and all are mispriced. At some point, these privately issued tokens are going to have to come out to the public as the notion of liquidity was (and still is) a big part of the story of these ICOs. When and if these tokens start to get launched on exchanges, the inevitable price drops may cause a bit of a ripple effect through the market. Many of these projects are good, solid tokens with strong teams, and this should sort itself out over time. But the near-term fallout could lead to a change in the current strong tone.

Notable Movers and Shakers

Last week’s market didn’t show much dispersion among tokens as everything not nailed down went straight up in line with Bitcoin. Active management in a market like this is difficult since just about any investment will drive positive returns, and news does not necessarily impact price. Despite this correlation, we’ve pulled out a few of last week’s interesting tokens.

- Dogecoin (DOGE) saw an upward move of 57% resulting from an April’s Fool joke that went on for too long. On Monday, Dogecoin tweeted out a survey requesting users to vote on a fictitious CEO. After winning by a landslide, Elon Musk began tweeting about the token, describing it as “pretty cool” causing further price appreciation.

- Salt (SALT) the token for lending platform Salt Lending saw serious price action last week of 26%. Crypto lending has been a hot topic in recent weeks with discussions around lending platform such as SALT, MakerDAO, Compound, BlockFi and more.

- Ripple (XRP) CTO made comments on Stellar-IBM partnership announcement: https://twitter.com/CryptoAmb/status/1114142367374761987

- Binance (BNB) was fairly flat last week compared to the rest of the crypto market rallies. Despite the lack of price action the company announced the launch of their DEX mainnet will happen this month and they are opening a new fiat-to-crypto exchange which will use Singapore dollars.

What We’re Reading this Week

Lack of trust is cited as one of the largest hurdles to blockchain adoption, and indeed this makes for an interesting paradox: how do you build trust in a trustless system? The article explores the different areas where trust needs to be built (regulation, security) and what groups are positively contributing to building trust in blockchains (EY, Elliptic, Binance).

The SEC was certainly busy this week releasing a token framework and No Action letter to Turnkey Jet Solutions. The framework and no action letter have been analyzed at length by individuals such as Katherine Wu and Arca’s own Phil Liu. While the SEC did not provide new insight, they confirmed what most knew -- that the majority of token issuances are security offerings.

The most talked about news last week is that Andresseen Horowitz is shedding its venture capital roots and becoming a registered investment advisor (RIA). Venture funds are permitted an exemption from RIA registration as long as 80% or more of their investments are in private companies (FYI tokens are not considered private companies). With the changing venture landscape however, many firms like a16z are finding it difficult to produce superior returns and revenues without branching outside of private investments. As a firm, a16z already acts like an investment bank, offering advisory, fundraising, and M&A type services. Registration as an RIA will now allow them to earn fees on this activity.

Tom Jessop, who heads up corporate development for Fidelity Digital Assets, discussed what crypto adoption the firm is observing with the roll out of its custody offering. As expected, many of their early adopters are crypto hedge funds, with family offices following close behind as interest in the uncorrelated nature of crypto increases. However, Jessop explains that 401(k)s - Fidelity is a 401(k) pension wholesaler - are not ready to invest.

As Coinbase continues on its path to institutionalizing its business and appealing to a broad user base, it announced last week that it had secured insurance coverage from Lloyd’s of London. It is important to note, that insuring assets on exchanges is different than just insuring custodied assets as they fall into two different risk buckets for insurers. Coinbase as an exchange has to purchase from the “crime” insurance market for assets in hot wallets, which are at higher risk for insider theft, hacking, and fraudulent transfers.

Tatianna Koffman explores five projects in sub-Saharan Africa that are utilizing blockchain in a variety of use cases including payments, banking, wildlife protection and education opportunities. In terms of development, Africa as a continent has been considered “left behind”, however, blockchain technology stands to make the largest impact here and is already gaining traction and adoption at much higher rates than in the rest of the world.

The town of Innisfil, Ontario announced last week that they would accept Bitcoin as a form of payment on property tax payments. The municipality reported that they may consider accepting BCH, LTC, ETH and XRP in the future.

Wien Energie, Austria’s largest energy provider, unveiled a “blockchain-driven” fridge last week. The fridge, developed in partnership with Bosch, allows consumers to track via blockchain the appliance’s manufacturing origin and the origin of its ongoing energy consumption. Wien Energie’s goal is to make consumers more aware of what energy sources are used to construct and run these appliances.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)