.jpg)

With global equities up nearly 20% year-to-date, it’s hard to fully appreciate the rally that the crypto markets are experiencing (which has continued into April). But most other risk assets are highly correlated to each other; whereas crypto continues to exhibit near-zero correlations to global equities and other asset classes. The true test of course will be how the crypto markets respond if/when the rug finally gets pulled out from under global stocks. Until that happens, crypto investors and non-crypto investors are both enjoying a pretty remarkable first half of the year.

Specific to the crypto markets, after the euphoria caused by 25% gains in the first week of April, most digital assets traded down pretty aggressively last week. While the overall market only declined 5%, a mild pullback following a torrid start to the month, that doesn’t tell the full story. Bitcoin outperformed all other digital assets last week, ending -1%, while many small-caps fell 15-25%. This is a stark reversal from the first few months of 2019, where small-cap cryptos were outpacing BTC by a significant margin.

Importantly, this wasn’t a slow drift lower fueled by profit taking. It was accompanied by another fast 10% correction, this time early Thursday morning before U.S. markets opened. BTC itself tested the $5,000 psychological barrier multiple times, each time bouncing off this level fairly easily. While we’re not technical strategists, we feel this resistance demonstrates that investors are more interested in buying dips than panic selling, even when we see a large and quick move lower. Further, volumes remain very healthy, with the CME even reporting record BTC Futures volumes.

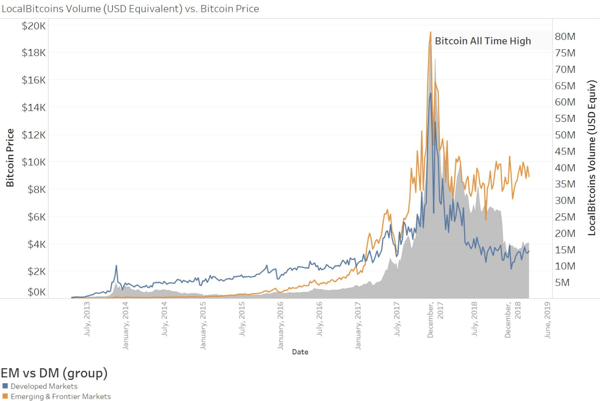

To understand why, recall that BTC matters a lot more outside of the U.S. where it is used as a safe-haven currency or banking alternative; versus BTC usage in the U.S. where it is mainly a speculative asset. As Passport Capital explains, volume in Developed Markets is tracking price (speculation) while volume in Emerging Markets has stabilized and is growing despite price (utility).

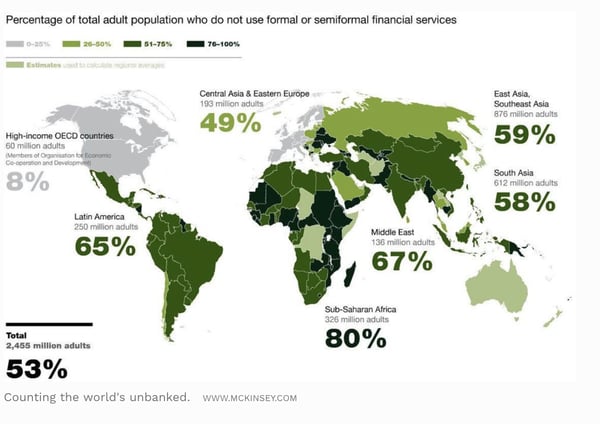

A recent Forbes article goes even deeper, looking at the areas of the world where formal banking services are not the primary means of storing wealth or transacting. As Eric Gravengaard put it:

Their entrance into the global financial world won't be via centralized financial services firms sponsored by their governments [much like] they didn't enter the worldwide telephone system with landlines. Leaping over ineffective systems is what the developing world does. When the middle class wants to invest I expect that in 10 years they will be buying index fund tokens and maintaining custody of them. They aren't unbanked because there aren't banks. They are unbanked because they don't trust them.

It remains to be seen how the rest of the market will react if BTC continues to leak lower and pushes through this resistance level. But for now, fear seems to be largely absent from investor psyche, which allows investors to keep risk limits high and look for other growth tokens and catalysts that can create outsized returns.

Exchange Risk - Under the Radar but Rearing its Ugly HeadDuring the crisis of 2008-2011, most investment committees focused less on what was IN the book, and instead focused on WHERE it was owned. Between Bear Stearns, Lehman Brothers, Merrill Lynch and even Knight Capital, Jefferies and MF Global… asset managers were terrified of counterparty risk. And rightfully so.

In crypto, this is once again rearing its ugly head. The media tends to focus only on large cases of fraud (like QuadrigaCX and Mt. Gox), or the fake volumes that often accompany unregulated exchanges, but exchange risk can be much simpler than this. In the past 2 weeks alone:Custody concerns are often cited as the biggest impediment to institutional investor growth, but a lack of institutional grade trading options is arguably more limiting. As our good friend Avi Felman of Wave Financial eloquently put it (and we’re paraphrasing):

If you’d like to buy an asset, there are usually two questions that you have to answer before you become a proud owner. (1) Do you want to buy this asset and (2) where can you buy this asset. These are normally very easy questions to ask for someone buying a stock.

Cryptocurrency is a bit different. Here’s a look at the different ways you can buy XRP.

You can buy XRP with BTC.

You can buy XRP with BNB.

You can buy XRP with ETH.

Or maybe let’s just use a stablecoin. It’s basically the dollar.

Ok - now where do I buy it (there are literally hundreds of exchanges and OTC dealers)?

Cryptocurrency has a fragmentation problem. It has a choice problem. When you’re buying something like XRP — all you care about is the price. You don’t care what you buy it with or where you buy it. For the active traders this exchange arb can be nice. All sorts of price discrepancies. But most people don’t have the time or systems to take advantage.

This is the reason we are seeing platforms like Bakkt, ErisX, Tagomi and others spring up. They are all trying to create liquidity pools to make it easier for investors and consumers to buy into the market to ensure they’re receiving a fair price.

Once again, we’ll draw the analogy to High Yield bonds and Emerging market bonds, all of which function perfectly fine without numerous exchanges. OTC desks dominate the flows, and provide a valuable service in addition to just liquidity (underwriting, research, price discovery, etc). Fortunately, many full-service crypto firms are getting better at the services they offer. We’re seeing real market color, research, and ancillary services from places like Galaxy Digital, Cumberland, Circle, Genesis and Galois Capital. Utilizing these services not only eliminates much of the exchange risk, but also creates workflows more akin to what traditional investors are accustomed to.

Bitcoin was born 10 years ago to rid ourselves of systemic risks -- the Exchanges and the investors utilizing these exchanges need to remember that.

Notable Movers and ShakersThe first half of the week was clouded by the steep intraday drop of the market as a whole, making it difficult to see the forest through the trees. However, the tail end of the week offered legitimate differentiation within the market as Bitcoin regained stability. As such, certain projects stood out: