What happened this week in the Crypto markets?

The 1st Quarter Closes on a Very Positive Note

Somehow, the S&P 500 Index posted its best quarterly price return (+13% YTD) since the third quarter of 2009. Yet, stock market activity was overshadowed by the inversion of the Treasury yield curve, followed by more downward pressure on interest rates. Something just isn’t right here.

With stocks and bonds booming, not to mention the constant theatre in Washington, it’s no surprise that many failed to notice the crypto rally in 1Q 2019. If a tree gains 20% in the forest, and no is around, did it still happen?

1Q Crypto Performance by Market Segment

So why didn’t anyone notice? Well, for starters, the media continues to focus solely on Bitcoin (BTC), which has “only” gained 11% YTD. Moreover, most narratives focus on the death of Bitcoin rather than the growth in the ecosystem. Even those who do look beyond Bitcoin may only recognize a few passively managed Indices, all of which largely focus on the Top 10-20 digital assets by market cap, and are thus significantly underperforming most actively managed funds.

Beneath the surface though, crypto as an asset class is booming. According to Messari, 24 altcoins including major projects like Binance Coin (BNB), Tezos (XTZ), Ontology (ONT), Basic Attention Token (BAT), and more have posted gains that surpass 100% in the last 90 days. And while a rally in “small caps” normally wouldn’t move the needle much, it’s worth remembering that just about every asset manager in crypto is small enough to take advantage of these small cap moves. And there is reason to believe that this may continue as there just aren’t enough motivated sellers. Aaron Brown, former Chief Risk Manager at $225 billion fund manager AQR, said it perfectly:

The run-up and crash pulled in about $20 billion in investor funding. It did a lot to clarify legal and regulatory issues, and it pulled in a lot of financial institutions. It raised public awareness and stimulated a lot of developer ideas. The boom pushed crypto forward three to five years in my estimation. The price spike brought in lots of investor money which are still financing useful innovation, and the collapse drove out a lot of schemers, fraudsters and delusional optimists.

Overall, it's a "risk on" environment at the moment. Negative risks are still out there of course, as another big exchange hack happened over the weekend, the Bitcoin ETF was delayed yet again, and very few market participants understand how OTC market manipulation in private tokens attempts to cover up the deep ICO losses from 2017/2018 that are still marked too high on many investors’ balance sheets (HINT: quotes aren’t executable prices). But many digital assets act like call options. The more time a project has, the more value can be created as network activity increases, and so in turn does the token price. The positive sentiment in crypto has bought crypto projects, and investors, a lot of time.

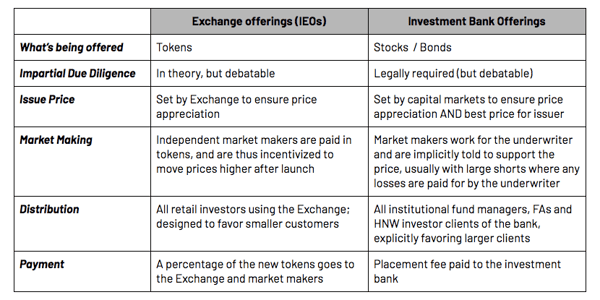

Initial Exchange Offerings (IEOs) - A Fancy Term for “Crypto Investment Banking”

Part of the 1Q rally can be attributed to the strength in centralized crypto exchanges. While Coinbase, Gemini and Kraken garner much of the attention in the U.S., achieving massive equity valuations, most crypto volume occurs on Binance. And as we mentioned last week, Binance and other copycat exchanges have executed a remarkable “token pivot” to unlock new value for their token holders. Tokens from Binance and others in the “Exchange sector” are up almost 200% YTD, on average.

The launch of the Initial Exchange Offering (IEO) is the reason behind the rally. IEOs have flourished thus far in 2019, taking over for the now defunct Initial Coin Offerings (ICOs), which were popular in 2017 and 2018 but have largely fizzled out. The big difference between IEOs and ICOs can be explained with one word: Distribution. In an ICO, the issuing firm/project spends a lot of time and money marketing its own coin to investors and network users, often racking up large and ongoing legal fees, and burdensome IR needs. In an IEO, the firm/project simply pays the exchange to do the work for them. If this sounds familiar, it’s because this is exactly what Investment Banks do.

In the traditional corporate world, most companies issues stocks and bonds to investors via an Investment Bank, which “underwrites” the offering and distributes it to investors (with the occasional exception like Google which went with the dutch auction approach). This underwriting feature is expensive, but gives investors comfort because there is a presumption that adequate due diligence was performed, and a fair price was achieved. The “direct to consumer” approach is rarely even discussed in traditional markets.

In an IEO, however, non-regulated exchanges are now taking on this role, albeit without the necessary broker-dealer licenses that would be required in the United States and other regulated jurisdictions. There are only a few differences:

For investors in IEOs, the outcome is largely the same as it was when buying directly via ICOs. But it’s just a lot easier, and there is perceived safety in numbers and centralization. The irony of course is that this is directly at odds with the decentralized ethos embedded in crypto, but this has been conveniently ignored as long as it’s working. And thus far, IEOs have performed incredibly well (up 150-300%), with both Exchanges and investors rewarded handsomely. Everyone involved is highly motivated not to kill the golden goose.

But people are greedy (i.e. Lyft IPO - raising price target from $62 to $72, and now trading below new issue price). Eventually one of these exchanges/issuers will price an IEO incorrectly, or sell too much of a token flooding the market, leading to immediate losses when the token is “free to trade”. When that happens with a stock or bond issue, the issuer may be punished, but the underwriter rarely is. The underwriter may even eat some of the losses by buying it back, or price their next new issue a little cheaper to “make it up” to their clients. It remains to be seen how Exchanges will react when this happens since they continue to try to avoid broker/dealer regulations.

March Madness

Congratulations to Auburn, Texas Tech, Virginia and Michigan State fans. For the rest of us just cheering for our brackets, think back 15 years ago when one person in your office would physically collect the brackets by hand, and you’d know the results 3 days after the tournament concluded because it was being calculated by hand. Then the internet flourished, which allowed everyone to see each others’ brackets in real-time, via a centralized 3rd party site (ESPN, CBS, etc), who made a ton of money off of this increase in web traffic. Now, the entire tournament challenge can happen via decentralized smart contracts, where no one benefits except the participants. This may not seem like the most important use case of blockchain technology, but it’s a nice reminder that even simple applications can be modified to eliminate the middleman.

Notable Movers and Shakers

The crypto market continues to be very bifurcated, but overall, it's "risk on" and no one seems scared at all anymore (which of course, is scary).

- Eos (EOS) made an announcement about an announcement that raised its price 15%. The project has been quiet for months, so even ambiguous news has investors excited. The aforementioned announcement is expected in June.

- In a bizarre set of events, an article published Friday claimed that OmiseGo’s (OMG) parent company, Omise, was purchased for $100m. Hours later, the founders of Omise claimed the story was false and that no such acquisition had occurred. The news caused OMG to bounce, ending the week up 8%.

- Privacy-focused smart contract platform, Enigma (ENG), rose 52% last week with the launch of its “discovery mainnet” phase on Sunday. The launch was originally slated for September last year but was delayed “in the interest of building out the Enigma ecosystem and continuing to work with the project’s stakeholders.”

- Tezos (XTZ) saw another week of massive gains (up 60%) after Coinbase announced they would stake custodied XTZ for their customers, essentially allowing investors to earn “interest” while assets are stored with the exchange.

- Basic Attention Token (BAT) saw gains of 32% last week after an Ask Me Anything (AMA) session with Brave CFO, Holli Brohen. During the AMA, Brohen explained what an acquisition of Brave would look like for the BAT ecosystem and token holders.

What We’re Reading this Week

In a not-so-surprising turn of events, the SEC has delayed ruling on the Bitwise and VanEck ETFs. The SEC now has until May 16 to make a final decision. The decision has been pushed back several times as has other decisions, with the CBOE actually withdrawing its application during January’s government shut down. The recent report from Bitwise Asset Management (see below) regarding faked Bitcoin exchange volume is not helping the case for a registered product.

Late Friday, news broke that Bithumb, a South Korean crypto exchange, experienced a hack for $13m worth of EOS from its hot wallet. The hack appears to be an inside job, as no “external exploits” have been found, rattling the crypto community. The exchange has moved all its assets to cold storage as it investigates the hack with local authorities.

M&A News

This educational article discusses the importance of tokens existing within blockchain networks. Traditionally, innovation is protected by businesses in order to maximize ROI, however, in crypto networks, innovation is shared and accessed via digital tokens. For those who hear, “I like blockchain, not Bitcoin”, remember that blockchains are not secure or censorship-free without tokens.

LVMH, the powerhouse behind designer brands such as Louis Vuitton and Christian Dior, announced last week that it would be launching a permissioned blockchain to track and authenticate luxury brand items. Although many will argue that permissioned (closed) blockchains aren’t the answer, this is an important first step for mainstream adoption.

Last week Bitwise Asset Management released this 227 page report to the SEC that detailed the volume manipulation that occurs on digital asset exchanges. They found that only 10 exchanges, that adhere to local regulations, actually accurately reported their volume. While this may be viewed negatively by some, it’s actually meant to be a positive as it shows there is a real underlying market even after you strip out the noise.

Following the Bitwise report, research firm, Messari, released their “Real 10 Volume”, which contains volumes from the 10 exchanges named in the Bitwise report, and the “Liquid Market Cap”, which provides a market cap that reflects what amount of a token is liquidly traded and available. We are starting to see real firms like Messari attempting to institutionalize crypto by providing tools and metrics that give an accurate snapshot of the ecosystem.

According to Anthony Pompliano, no. In his analysis (paywall), he discussed how distribution is the key to cracking the crypto adoption puzzle:

Apple Card is a great reminder that distribution is king. Tens of millions of people are going to be on-boarded into a new, digital financial ecosystem through Apple (Apple Pay, Apple Cash, Apple Card, Apple Wallet, etc). Rather than sitting around and praying that Apple will support Bitcoin and cryptocurrencies, we need more companies building products that can gain mainstream adoption.

This distribution advantage that many tech giants hold is why I continue to say that Facebook is the most important company in crypto today. Whatever they release, positive or negative, will immediately be one of the most used products in the industry. The large user base available to Facebook means that hundreds of millions of people will have their first experience with “crypto” throughout whatever product Facebook launches, making it imperative that the social media giant gets it right. (Apple is likely to be in this position within the next 24 months).

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Chief Investment Officer

Katie Talati — VP, Research

Hassan Bassiri, CFA — VP, Portfolio Management

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)