What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 3/07/21)

Buying the Dip Only Works When There is a Dip to be Bought

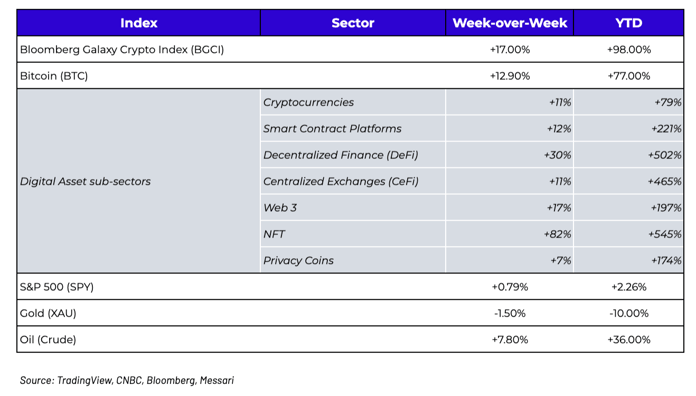

If you were looking to buy the dip in digital assets, you couldn’t have asked for a better setup to do so. The yield on the 10-year US Treasury note backed up another +16 bps, gold fell -1.5%, the Nasdaq dropped -3%, the US Dollar gained +1%, investment grade credit spreads widened 5 bps, the VIX breached 30, and “crypto stocks” broadly declined 10-30%.

There was only one small problem with the “buy the dip” plan… the digital assets market didn’t even hiccup last week, let alone decline. Digital assets snoozed their way towards another double-digit weekly again, acting as if the increasing risks around the world were completely isolated from this new digitized financial system. It appears as if past correlations (which we’ve noted previously have been spurious at best anyway) have given way to a complete asset class re-allocation, where newfound interest and money flocking to this space has completely overwhelmed any moderate selling pressure.

That said, digital assets did have a large correction the week before, indicating that digital assets may once again be acting as a leading indicator for risk assets rather than a lagging indicator. This happened quite frequently in the 2nd quarter of 2020. We’ve also previously seen periods where digital assets simply lag broader markets, as it takes a bit more time for the news that affects equity bots and algos to permeate the digital assets arena. But it’s far more likely that this is simply the new norm. Digital assets are operating on an entirely different playing field than the interconnected and interdependent financial system, allowing asset prices to adjust idiosyncratically, and this past week there were simply more buyers than sellers. Larry Cermak from the Block’s research division put out a monster, data-fueled Twitter thread illustrating why it’s hard not to be optimistic when looking at the growth in digital assets. Narratives are important, but data simply tells a much better story.

A booming asset class is the result of new investors not only investing their money, but also their time. As more investors learn about this space, they begin to recognize that it is not as intimidating as perhaps previously thought. Arca for example does not employ a single software developer. That’s not a source of pride per se, but rather a reality -- the technology skills once needed to invest in early stage protocol tokens in 2017 have simply become less relevant than the financial skills needed to invest in Bitcoin (macro/trading), and pass-through tokens of revenue generating companies and protocols (financial research/modeling). A tech background has taken a back seat to a finance background, especially pertaining to decentralized finance and other revenue-producing entities.

And many of the old school traditional finance investors are not shy to point this out. When an old guy learns new tricks, he proudly shows the world how easy it really is.

There are very few valid excuses left at this point, lest you want to become this guy.

The Rise of NFTs - More than Just Art and Collectibles

The fear of crippling inflation may be far-fetched. But in the mean-time, many investors are so concerned about inflation that they will invest in just about anything to eliminate holding cash on their balance sheets. When investors become too scared to hold cash even for a short-period of time, you know the world isn’t quite as it used to be.

With that backdrop, it’s not terribly surprising that a lot of non-financial assets are trading at astronomical prices, from sports cards to real estate to the recent non-fungible token (NFT) craze. The only way to decrease cash is to park that cash into something else, and when everyone is doing it at the same time, there is a good chance that prices will go higher. In short, an NFT is simply a unique asset represented entirely in digital form. While the media has covered NFTs purely from an art and collectibles standpoint, the NFT space is more far-reaching than just that one small niche. As we wrote in our 2021 predictions:

“Gaming is still the most natural non-money use case for blockchain, and with the rise of Non-Fungible Tokens (NFTs), there will be strong growth in specific games and ecosystems. These gains will most likely not come from the platforms built to facilitate this growth, but rather from the individual games and NFTs themselves. Finding these opportunities will be lumpy, with a few huge winners and a lot of losers (similar to financing a movie). And since one will have the ability to see growth metrics in real-time via public blockchain data, the winners will be obvious and investable. Further, NFTs will expand beyond current use cases such as collectibles, art and gaming into more traditional use cases like KYC, asset-backed loans (i.e. putting the value of your house/car on chain to collateralize a loan), and fractional ownership of specific properties.”

From an investing standpoint, there are investable companies and projects that facilitate the growth and trading of NFTs, and there are the individual NFTs themselves. Prices of both have shot through the roof in recent weeks. According to Messari, tokens affiliated with NFT businesses gained on average +82% last week,

and have now increased +545% YTD.

Whether a digitized tweet, a digitized moment of an NBA dunk, or digital art is really worth tens to hundreds of thousands of dollars is entirely up to the buyer willing to pay this price. But conceptually, there’s nothing weird about non-fungible tokens.

Let’s take video games for instance. In-game assets (like swords, skins, or characters) used to be confined to the game itself. If you stopped playing, you lost all of the value you created inside that game. But as these in-game assets turn into NFTs, you own the asset whether you continue to play the game or not. Let’s say you’ve spent a year playing a game but then one day decide to play a new game. You can now sell any assets acquired in the first game to those still invested in that game, and use the proceeds to acquire different assets in the new game. Or, users can monetize their sweat equity in the game into real world value as they take advantage of “play to earn” economies. There may even be a scenario in which there is cross game compatibility, where NFTs can be utilized in more than one game, creating true composability of in-game assets in a digital ecosystem. Essentially, NFTs begin to quantify time spent on playing games into equity.

That’s not that strange; in fact it’s pretty exciting. But when that equity goes from $0 to $1,000,000 in a matter of days, it can naturally trigger the emotions of those invested, and those left behind on the sidelines. Sure, some of these prices are crazy and unsustainable, but there are plenty of even crazier things happening in society that don’t result in emotional swings of millions of dollars of net worth, and thus don’t trigger the same media onslaught and investor uptake. For example, I recently saw that my wife had accidentally purchased lavender-scented Swiffer cloths that I was supposed to use to clean my hardwood floors. Unless there is an entire cohort of people who smell hardwood floors that I’m not aware of, this seems like a crazy and completely unnecessary product. Yet this is probably adding millions of dollars to Proctor and Gamble’s revenue, ultimately flowing through to PG shareholders. I doubt anyone really cares about how silly this product is because no single person is getting rich off of lavender Swiffer cloths. However, when an NFT investor or creator makes millions, there is an uproar. Similarly, it makes no sense to me why Live Nation (LYV) stock is at all-time highs even though no one has gone to a live sporting event or concert in over a year. I’ve spent zero time analyzing LYV, but I’m sure there is someone out there who has done the work and can give a very concise reason for why this stock is trading where it is. For me to opine on LYV stock would be just as uneducated as everyone calling digital assets, NFTs and Bitcoin a bubble.

Challenging our own views without assuming others are crazy is an important aspect of investing. In a recent memo, Howard Marks wrote:

“The natural state for the value investor is one of skepticism. Our default reaction is to be deeply dubious when we hear “this time it’s different,” and we point to a history of speculative manias and financial innovations that left behind significant carnage. It’s this skepticism that reduces the value investor’s probability of losing money. However, in a world where so much innovation is happening at such a rapid pace, this mindset should be paired with a deep curiosity, openness to new ideas, and willingness to learn before forming a view. The nature of innovation generally is such that, in the beginning, only a few believe in something that seems absurd when compared to the deeply entrenched status quo. When innovations work, it’s only later that what first seemed crazy becomes consensus. Without attaining real knowledge of what’s going on and attempting to fully understand the positive case, it’s impossible to have a sufficiently informed view to warrant the dismissiveness that many of us exhibit in the face of innovation.”

NFTs may be a fad. But they also may be how all assets are owned in an increasingly digital future. Regardless, it’s worth opening our minds to find out.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.png?width=902&name=pasted%20image%200%20(16).png)