What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 8/30/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+0.6%

|

+61%

|

|

Bloomberg Galaxy Crypto Index

|

+3.5%

|

+99%

|

|

S&P 500

|

+3.3%

|

+8.6%

|

|

Gold (XAU)

|

+0.6%

|

+28%

|

|

Oil (Brent)

|

+1.5%

|

-30%

|

Source: TradingView, CNBC, Bloomberg

Bitcoin is Undoubtedly a Global Macro Asset Now

After gaining another 3% last week, the S&P 500 is now up 7% for the month of August, on pace for the best August since 1984. It’s not surprising that US equities rose during a week when Fed Chairman Powell spoke, as that has been a pattern during “Fed weeks” for most of the past two decades of easy monetary policy. Every equity, bond, macro and commodity desk was glued to the screens while Powell spoke, after years of Pavlovian training. Last week was no different.

What was surprising and different is that every Bitcoin trader was also glued to the screens last week. If there were any doubts left that Bitcoin is now a global macro asset, this past week cleared that up definitively. Bitcoin and gold tracked each other almost perfectly, with a 3-day correlation of 0.76 before, during, and after Powell’s speech.

BTC & Gold Prices Last Week Before, During and After Powell’s Speech

Source: Bloomberg

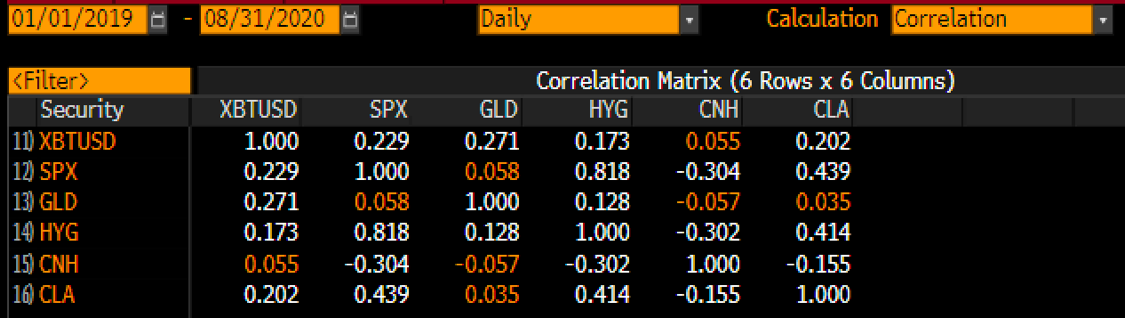

Before we make too much of this, it’s worth noting that Bitcoin has spurious relationships with a lot of risk assets. At times throughout the past few years, we’ve highlighted Bitcoin’s strong short-term correlations with the S&P 500, Gold, the Chinese Yuan, and even Avocados. None of these correlations have held over longer-term horizons, as Bitcoin’s longer-term correlations with risk assets remain close to 0.

BTC Correlation to SPX, Gold, HYG, CNH and Oil Since 2019

Source: Bloomberg

That said, these correlations should begin to rise as the investor types converge, and the investment thesis narrows (store of value / inflation hedge). When the same traders / algos are involved in all asset classes, and are focused on the same narratives, it makes sense for correlations to increase. In the past 6 months alone, we’ve seen public companies, institutional investors, large macro hedge funds, prominent banks and brokerages, and regulated exchanges get further involved with Bitcoin. While a long-term investment in Bitcoin may remain differentiated and uncorrelated, as a tradeable asset, last week cemented Bitcoin’s status as a legit, global risk asset.

It’s ironic that many investors left Wall Street and came to digital assets specifically to get away from the “don’t fight the Fed” manipulated equity and debt markets, and yet a few years later, Bitcoin investors are now hanging on every word from Powell too.

Stop Comparing the Current Digital Assets Bull Market to 2017

Bitcoin’s 1% rise last week sure was cute. But keeping with this year’s trend, Bitcoin was once again not the top story in the Digital Assets market last week. Neither was Ethereum or any of the other large-cap legacy “cryptocurrencies” that rose to prominence years ago. Once again, many small-cap tokens and privately traded tokens outperformed handily, with thematic focuses on decentralized Finance (DeFi), file storage and archiving, decentralized autonomous organizations (DAOs) and non-fungible tokens (NFTs). According to Messari, 53 digital assets with market caps over $25 million rose more than 10% last week, with 25 tokens gaining over 25% week-over-week. It’s worth noting that this is not a “student body right” bull market, as over 50 assets also fell more than 7% last week, with 28 dropping by 10% or more.

While Bitcoin is on pace to gain just 3% in August, many crypto indexes are on pace to gain closer to 7-10% month-over-month, and actively managed research-focused fundamental funds will likely blow away both as over 125 assets have gained more than 10% in August, and over 60 have gained more than 50% this month alone. Due to the outsized nature of gains across small-cap tokens, we’re beginning to hear a lot of comparisons between the current market and that of 2017, when prices shot up like a cannon only to fall precipitously over the next 24 months.

Let’s be perfectly clear here. Today’s market resembles nothing close to that of 2017.

The biggest difference between 2017 and 2020 is that many of the tokens today are being created AFTER a company has already found product market fit. Instead of tokens being issued simply to fund pipe dream “decentralized projects” with low probabilities of success, many of today’s leading tokens are being used to enhance already thriving ecosystems and growing customer bases. Many of these tokens are created and structured (and often restructured) in a way that furthers that product market fit by bootstrapping customer growth and better aligning incentives between company and customer. Companies and projects have had years of history to study both the successes and failures, and are thus responding by issuing tokens that accrue real economic value via revenue and fee growth that can be passed through to token holders. And investors are no longer blindly guessing. Third-party research firms like Delphi Digital, Messari and The Block have emerged as a form of “checks and balances”, and data providers like Digital Assets Data, Flipside Crypto and the Skew have provided investors with knowledge sets that back-up investment theses.

This evolution of token structure, which lends itself to traditional financial analysis, is why fund managers with actual asset management experience are able to confidently invest institutional LP money today. This is a far cry from the developers and programmers in 2017 who took friends and family money to bet on any newly issued token issued by a technologically sound team with a white paper filled with promises.

We recently had the opportunity to speak to several groups of investors hosted in round-table fashion by a few leading traditional brokerage firms. This conversation was not about Bitcoin, cryptocurrencies, rapid price increases, or technical analysis. Rather, we focused on the other types of Digital Assets that are capturing most of the value in today’s market. While blockchain technology itself is revolutionary, the instruments we’re now able to invest in are evolutionary -- hybrid equity/utility securities that are among the most novel capital formation and bootstrapping instruments ever created. Digital Assets are now the third part of the capital structure for companies who want to pass through their growth directly to customers.

Evolution is hard to grasp. I still can’t quite come to terms with the fact that humans, whales and bats share a common ancestor. But as crazy as this new hybrid token structure may sound to those who aren’t privy to the small incremental changes each and every day, remember that “sure things” are often anything but.

We firmly believe investing in this evolution has staying power. Forget 2017.

Source: Zerohedge via Twitter

Notable Movers and Shakers

If you blink, you might miss it. If you dare to go to bed, you will undoubtedly miss it. The Cambrian Explosion of digital assets this year coming off the heels of a worldwide quarantine and drastically shifted work environments shouldn’t come of great surprise - programmers, developers, builders, and thinkers were given a mandatory seclusion period from social interaction(s) to focus on iterating the future of this asset class. For context, we look towards Decentralized Finance:

- DeFi boasts some of the most exciting developments in this space - from the Food Pyramid of Yield Farming (YAM, PASTA, SUSHI, etc.) to Automated Market Makers (CRV, Uniswap, KNC, Matcha, etc.) to Lending Platforms (LEND, COMP, MKR) to Derivatives (SNX) to Insurance (NXM) to Aggregators (YFI). Many of these are in their infancy (and should be treated as such); but where there is smoke, there is fire. Right now, there’s quite a bit of smoke.

- Weekly moves: YFI (+155%), SRM (+87%), BZRX (+48%), NXM (+48%), LEND (+39%), BAL (+35%), and SNX (+28%) highlight an impressive week for the entire sector.

- 2017 legacy tokens like OMG (-15%), CKB (-14%), ZRX (-12%), and REP (-9%) round out the laggards in the sector.

What We’re Reading this Week

The biggest news last week was that the SEC finally released its expanded definition for accredited investors. Previously, the accredited investor definition was based solely on an individual’s wealth: they either had to make $200,000 per year ($300,000 if filing jointly) or have $1 million+ in net wealth. The narrow definition excluded anyone else, including individuals that might be considered to have industry knowledge or expertise in an area. The updated definition works to rectify this by adding a new category that allows “natural persons” to qualify for accredited investor status if they have “certain professional certifications, designations or credentials or other credentials issued by an accredited educational institution”. To start, the SEC has identified the Series 7, Series 65, and Series 82 licenses as these credentials, with promises to potentially add other professional designations in the future. The expanded definition will open-up private market access to more individuals, something that has long been reserved for the wealthy. The changes are slated to take effect in 60 days.

Last week, Fidelity filed a Bitcoin fund product with the SEC, making it the financial giant’s first Bitcoin product. The fund will be a passively managed closed-end fund offered only to qualified purchases, such as family offices, registered investment advisors, and other institutions. Of note, this Bitcoin fund is not being launched through Fidelity Digital Assets, the division of Fidelity that offers custody and trading of digital assets to its clients. The distinction is important as it signals that Fidelity Investments as a whole is invested in the future of digital assets and believes in its long-term growth trajectory.

FTX, a digital asset exchange that focuses on offering derivative products, last week announced it had acquired Blockfolio, the largest mobile cryptocurrency tracking and news app. The $150m deal is not merely an acquisition of intellectual property for FTX but an acquisition that presents “synergy and scale up” according to FTX’s CEO Sam Bankman-Fried. Specifically, the purchase of Blockfolio will allow FTX to scale its mobile effort and grow its user base as Blockfolio has a large audience with over 150m impressions each month. We expect to see more deals like this one between small picks and shovels businesses and exchanges as the digital assets industry continues to grow.

Following the announcement from Microstrategy a few weeks back, it appears that other companies are following suit and hedging their dollar risk with Bitcoin. Canadian software startup Snappa announced it allocated 40% of its cash reserves to Bitcoin last week, describing inflation and global economic uncertainty for the cash management strategy. Snappa’s CEO discussed the strategy in a blog post, stating that “we now have a far superior savings technology available to us, that technology is Bitcoin.” Although Snappa is far smaller than NASDAQ-listed Microstrategy, we’re beginning to see a trend of Bitcoin becoming a viable alternative to cash for many businesses.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency