What happened this week in the Crypto markets?

Bitcoin Crypto is Acting like a Leading Indicator for Risk

Another 6 million Americans filed for jobless claims last week, and the Federal Reserve reacted with another $2.3 trillion in stimulus. These bailouts have enraged those who believe in free markets, with some even pointing out that this new round of asset buying from the Fed is actually illegal.

The economic picture and subsequent news flow continue to drive prices globally, with correlations between asset classes remaining higher than normal. We’ve been highlighting the below week-over-week chart for the past few weeks and have noticed a trend. Bitcoin seems to be acting as a leading indicator for equities during this bout of volatility. A few theories for why this might be happening:

- 24/7 trading in crypto has turned Bitcoin into the best real-time barometer of information, especially over weekends.

- Bitcoin is being traded more actively by macro hedge funds, which has removed some of the natural barriers between crypto and other asset classes.

Like the correlation spike, this is unlikely to hold in the long-term. But it’s becoming harder and harder for traditional investors to ignore Bitcoin.

| Week Ending |

3/15/20 |

3/22/20 |

3/29/20 |

4/05/20 |

4/12/20 |

| S&P 500 |

-9% |

-15% |

+10% |

-2% |

+12% |

| Bitcoin |

-34% |

+11% |

Unched |

+13% |

+2% |

| Gold |

-8% |

-2% |

+9% |

Unched |

+4% |

| Oil |

-33% |

-28% |

Unched |

+25% |

-9% |

Source: CNBC, TradingView, CoinMarketcap

“Not Bullish” Doesn’t Have to Mean “Bearish”

We wrote last week that many traders are growing increasingly frustrated, as they continue to short stocks, bonds and crypto into a brick wall of cash that will not let equity and debt markets fully re-price. So we were not surprised when equities jumped 12% last week, and investment grade bonds rallied close to record highs. We think this frustration may continue for a few months, but not because stocks or bonds are cheap. In fact, quite the opposite. Stocks, for example, are VERY expensive. From Peter Cecchini at Cantor Fitzgerald:

"The S&P 500 is +22.4% from the 3/23 lows, pushing P/E multiples to 19.0x forward earnings (based on fresh downwardly revised earnings estimates). This is the same P/E level as on Feb 19, the all-time high for stocks. According to Factset, after being stubbornly sticky for the past month, full-year 2020 earnings estimates growth finally dipped into contraction (current reading of -3.2% YoY). This contrasts with hopes for a 7.5% expansion as of the end of February, and nearly 10% growth expected at the start of the year. Recall this follows flat 2019 earnings. As companies start to report earnings for the Covid-19-shutdown quarters, we expect analysts to further downgrade their expectations. We foresee a 10% EPS contraction as easily possible, especially when you incorporate the fact that stock buybacks, perhaps the most persistent supporter of expanding EPS over the past decade, may vanish as companies will no longer have the extra revenue to manufacture higher earnings.”

Profits and cash flow look bleak, which of course is negative for asset prices. But 1Q earnings won't matter much since most of 1Q was pre-quarantine, and the outlook for 2Q doesn't matter much either since everyone knows it will be horrific and are now expecting the worst. We may have to wait until we get forward guidance from companies for the 2nd half of the year (which won’t be given until AFTER 2Q earnings), before we get new and relevant information, since that is when the divergent options start. Some think we will see a fast V-shaped recovery in the 2nd half, others don't. What companies say about 3Q and 4Q outlook will likely drive markets for the remainder of the year, which means the next significant catalyst is not until July. That's a long time from now in trading terms.

Asset Classes That Have Been Expensive for a Long Time

Just because stocks and corporate bonds are expensive doesn't mean shorts will work. These asset classes have been expensive for a long time. Keeping a short on from now until July is going to be a tough and expensive trade, in any asset class, without a near-term catalyst for prices to really go lower. The effects of this crisis may take 2-3 years to play out -- but many are trying to force the market lower in 2-3 months.

Investors who panicked and pulled all of their money out of the markets have likely already done so, while those that are still left are going to be more methodical. And in the meantime, cash builds:

- Coupons still get paid on bonds, so fixed income funds will be flush with cash to redeploy

- Dividends still get paid on some stocks, which means equity funds are flush with cash to redeploy

- 401ks still auto-deploy to equities, for those that still have jobs

It doesn’t take inflows to support equity or debt prices, as long as there aren’t outflows. Specific to crypto, unless global equity and debt markets crater, Bitcoin seems to have a higher floor now. Not only is the long-term fairly secure due to record monetary and fiscal stimulus in addition to reduced supply pressures (Bitcoin’s supply halves in a few weeks), but in the short-term, Bitcoin and other digital assets are supported by similar cash balances and negative sentiment, along with a lack of sellers. Three things worth watching in crypto:

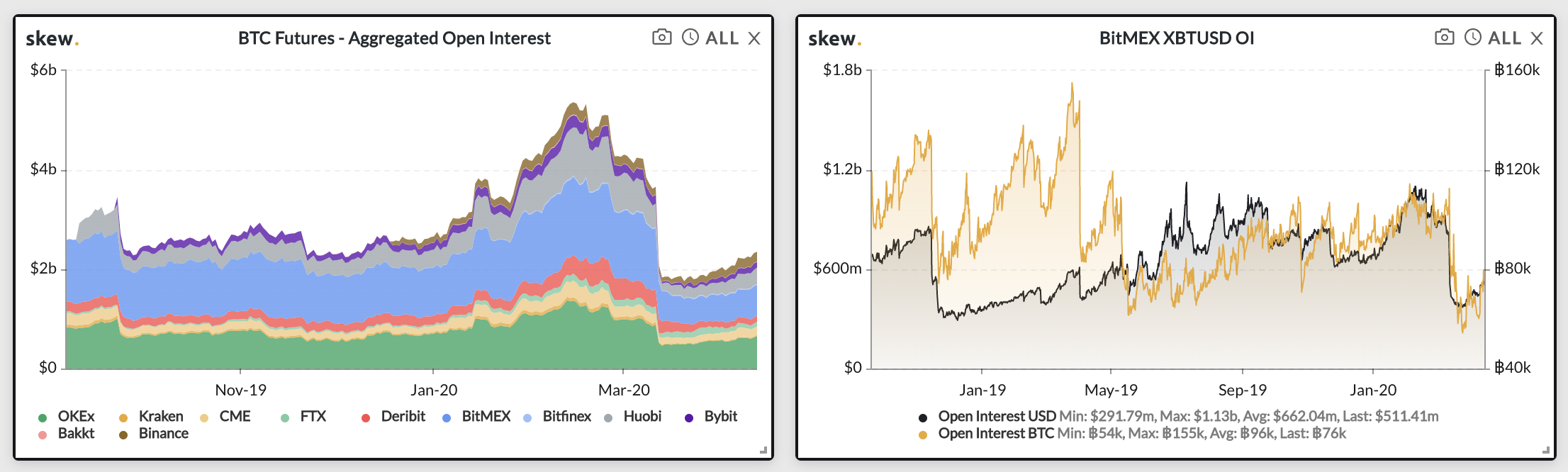

Open interest on Bitcoin Futures exchanges is at all-time lows

Source: Skew

Source: Skew

These metrics are very supportive of prices. With this backdrop, it is VERY hard to short risk assets into a wall of cash right now, including Bitcoin. Prices can certainly go down, but it would not be surprising if they keep melting up.

Financial Advisor Response to “Digital Assets are Recession Proof”

We recently wrote an op-ed for Coindesk suggesting that Digital Assets may be recession proof, and we received a lot of feedback. Perhaps the most interesting came from a Merrill Lynch financial advisor, who pulled out the following quote: “These tokens are claims on future services, not claims on revenue, profit or assets. As a result, most of these digital projects and companies appear to be immune to demand shocks and supply shocks. One day we may even say “digital assets are recession-proof.”

And responded with:

I think this may be the comment that could change how people think about “saving” for the future. Because in reality, all we do as financial advisors is bridge the gap between assets/cash flow now, to future liabilities (house and retirement needs), by investing in equity and fixed income which in theory should go up over a specific time period. But what if we knew the exact cost now for the future liability? If Health Care could be paid for up front in the form of a digital asset, or vacations, or housing expenses? This could change the formula.

This is the kind of ‘out of the box’ thinking that we expect from Wall Street (as soon as they figure out how to profit from it of course). We’re a firm believer that the use of digital assets will ultimately be utilized more by real companies and institutions, not just decentralized projects. We believe the inefficiencies caused by investing to meet a long-term cash need will be closed by blockchain technology. We look forward to more great ideas like this.

Notable Movers and Shakers

While Bitcoin finished the week close to where it began (+2%), alternative digital assets showed some outperformance, with Bitcoin dominance falling 150 basis points. This week we focused on two projects whose news stood out from the pack:

- Chainlink (LINK) is slated to be listed on Gemini on April 24th, according to a blog post released Thursday. Gemini works closely with the NYDFS to obtain approval for listing assets, which bodes well for Chainlink and its tokens use case in the viewpoint of the United States. Chainlink also partnered with Cypherium, an enterprise focused blockchain platform, in an effort to enhance the functionality of the Cypherium blockchain. Chainlink continues to make strides as a pick and shovel product via partnerships, and the token price reflects that: LINK finished the week up 51%.

- Matic Network (MATIC) announced on Monday that 100% of tokens set to be unlocked for the Team and Foundation in April will be allocated to staking on the MATIC network, as well as at least 50% of all unlocked tokens set to go to Advisors (1.3%of total supply, 0.65% full unlocked). The net result is 12.18% of the total supply being unlocked, but only 0.65% of it being released without staking obligations. As more and more projects see their tokens vest, there will be pressure for those tokens to be re-locked in some way, shape, or form. MATIC received a bump on the news, finishing the week up 7%.

What We’re Reading this Week

Last week, a class action lawsuit was filed against several large crypto exchanges and token projects, alleging that the groups sold unregistered securities. The lawsuit names 42 defendants including crypto exchanges, Binance and Bitmex, and token issuers, Tron and Block.One. According to filings, which were submitted to the Southern District of New York, each of these groups are accused of selling unregistered securities and taking advantage of investors’ lack of understanding of cryptocurrencies. It is unclear what the outcome of such a large lawsuit will be, especially with so many different parties involved, but this is likely a case that will hang over the industry for some time.

The Bank of International Settlements (BIS) released a report pushing for the adoption of Central Bank Digital Currencies (CBDCs) and digital payments in light of the COVID-19 pandemic. In places such as the UK, ATM withdrawals have fallen steeply as consumers fear transmission of the virus through banknotes. Many countries should consider what contactless payment methods consumers might turn towards during this time, such as mobile and online payments. However, BIS also warns that a move to digital payments could inadvertently cut out the unbanked and elderly from accessing financial services leading to a “payments divide”.

PwC last week released its 2019 Crypto M&A and Fundraising Report covering capital raising trends within the ecosystem. Highlights from the report show that the number of deals (fundraising and M&A) and dollar value of those deals declined sharply from 2018 to 2019. In addition, activity saw a geographic shift from the Americas to Asia / EMEA, likely a result of the regulatory uncertainty surrounding the US. The report also posits that 2020 will likely bring further consolidation as the industry contracts with the global market turbulence.

Last week, Visa joined Fintech startup Fold to issue a debit card that rewards users with Bitcoin instead of airline miles or cash. Unlike other crypto cards which allow users to spend their current crypto holdings, the Fold card is aimed at non-crypto users as a way to get them involved and simplify the process of acquiring Bitcoin. Fold is also planning on allowing users to spend the Bitcoin earned from rewards to purchase gift cards on their platform for businesses such as Uber or Starbucks.

Forbes’s Billionaire List now includes four crypto entrepreneurs who have a combined net wealth of $8.7b. Named to this year’s list are Bitmain co-founders Micran Zhee and Jihan Wu, Ripple co-founder Chris Larsen, and Coinbase CEO Brian Armstrong. What is interesting about these individuals being named to the list is that they all built their wealth from their current crypto-based businesses and have done so within the past decade. These executives might be following a similar path as the “PayPal Mafia”, who amassed their wealth and legacy at the payments giant before going on to pioneer an entire new tech era.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)