What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 9/20/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+6.3%

|

+51%

|

|

Bloomberg Galaxy Crypto Index

|

+3.2%

|

+74%

|

|

S&P 500

|

-0.6%

|

+3%

|

|

Gold (XAU)

|

+1.9%

|

+30%

|

|

Oil (Brent)

|

+9.6%

|

-33%

|

Source: TradingView, CNBC, Bloomberg

Bifurcation and Volatility

U.S. stocks closed at a six-week low, driven once again by weakness in technology stocks. The Nasdaq 100 moved more than 1% on 13 of 14 days in September. And even though more than 70% of the S&P 500 stocks were higher, the index closed lower for the third week in a row. One of the market’s winners, Microstrategy (MSTR), continues to toe the line between tech stock and crypto stock, rising 13% after announcing another $175 million of Bitcoin purchases from their cash Treasury. As we noted last month, CFOs around the world are paying attention, if not to their declining purchasing power in cash, most certainly to MSTR’s stock price.

Similar dispersion and volatility emerged in digital assets. For the past few months, we’ve highlighted that Bitcoin and most legacy large cap tokens have not only underperformed the market, but have been quite uneventful relative to new up-and-coming tokens with better value accrual mechanisms. Last week, this trend reversed. Bitcoin untethered itself from its near-term correlation with tech stocks, and rose steadily throughout the week, ultimately gaining 6%, while Ethereum finally outperformed its Decentralized Finance (DeFi) counterparts, rising 2% vs the FTX DeFi perp -20%.

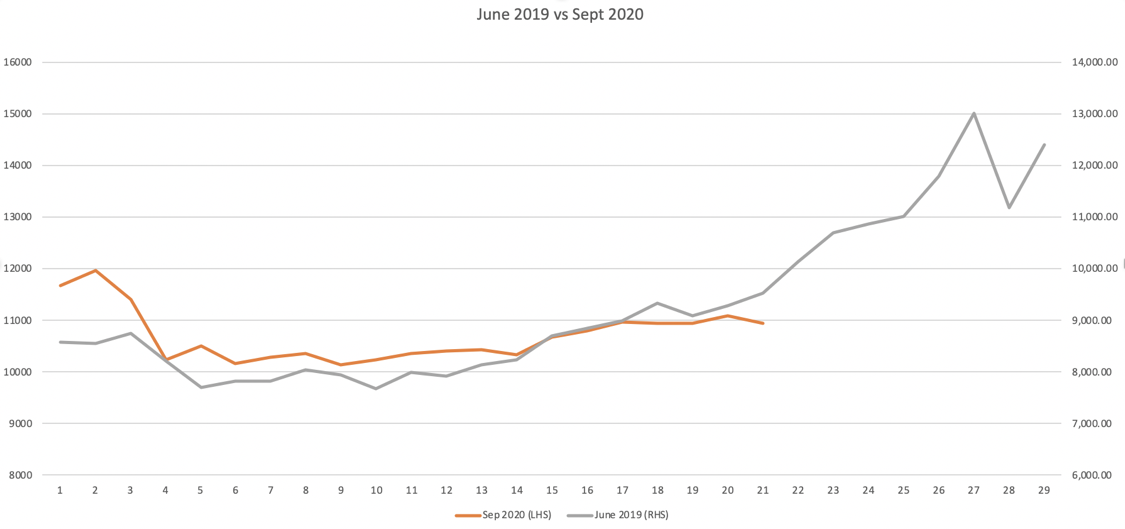

Bitcoin’s sharp decline to start the month, followed by a flat-line recovery and then a slow grind higher, looks eerily similar to that of June 2019, which of course culminated in an 80% rally from peak to trough in the final 10 days of trading.

BTC price chart - June 2019 vs September 2020

Source: Coinmarketcap.com / Arca

Uniswap Just Changed the Game, and it is VERY Exciting

Imagine if Apple gave every early adopter of the iPhone some shares of Apple stock, or if Amazon gave all Amazon Prime members some form of financial upside. Every new technology company, from LinkedIn to Facebook to SoFi, owes a great deal of gratitude to their early customers and evangelists, yet most have no way of benefiting financially from the success of the companies that they helped build.

Until now.

Uniswap is the largest Decentralized Exchange (DEX) by trading volume and is the first DEX to compete with its larger Centralized exchange counterparts, recently surpassing Coinbase Pro’s daily trading volumes. Last week, Uniswap issued its inaugural token, UNI. But instead of selling it to unsuspecting retail investors at egregious prices, or fattening the pockets of VCs, Uniswap simply gave 400 tokens away to every customer who ever used the Uniswap platform prior to 9/1/2020.

This might be the smartest and most groundbreaking token launch ever created by a team developing in the blockchain ecosystem, epitomizing the digital assets ethos that customers and investors can and should be the same people. And this was done without a single investment banker taking underwriting fees.

Following the token launch, UNI tokens are now held by more than 50,000 Ethereum addresses (wallets), making it instantly one of the most decentralized tokens in the entire marketplace. The Uniswap team minted 1 billion UNI tokens at genesis, which will become fully outstanding over the course of four years. The initial four-year allocation is as follows:

- 60% to Uniswap community members (600,000,000 UNI)

- Of this, 15% of the circulating supply was distributed via airdrop to reward past and existing users.

- 21.51% to team members and future employees with four-year vesting (215,101,000 UNI)

- 17.80% to equity investors with four-year vesting (178,000,000 UNI)

- .069% to advisors with four-year vesting (6,899,000 UNI)

As tens of thousands of early Uniswap users claimed their tokens, the token immediately listed on Uniswap and several centralized exchanges, allowing price discovery to begin. UNI tokens initially traded near $3, reached a peak of $8, and settled around $5 as of Sunday night. This was akin to a direct listing, where there was no underwriter setting an arbitrary price. Instead, the market decided where UNI should trade. New buyers began valuing Uniswap using traditional P/E analysis (Uniswap generates almost $250mm in annualized earnings, and thus trades at a very low P/E), presumably accumulating tokens from those who were happy to monetize their unexpected free gift. Ironically, at $3/token, this gift ended up being exactly the same amount as the stimulus check of $1,200.

Of course, the question of what UNI tokens are worth is up for debate. This is a governance token, meaning those who hold the UNI tokens have control over company decisions, including using the fee switch (Uniswap built in a fee switch that changed the 0.3% that currently goes to liquidity providers to now 0.25% to LPs and 0.05% to tokenholders). The jury is still out regarding whether or not the community owned project will correctly balance the rewards, but they should strive towards the goal of mutually beneficial governance decisions to ensure its users, investors and liquidity providers are all happy. That said, it is a step in the right direction towards a fully democratized ownership structure.

Decisions like this are a big reason why many of us left traditional finance and entered the digital assets space, and strengthens the argument that token issuances are the most innovative capital formation and bootstrapping mechanism ever created. Every other project in the ecosystem is studying this result, and every user of digital assets is now thinking about what other projects out there should be tested just in case they get rewarded years later. The digital assets universe really is blurring the gap between customers and investors.

Think about how many young kids began testing decentralized finance applications over the past few years. Many can’t even open a bank account or a brokerage account without an adult, but just received an immediately monetizable dividend simply for being an early customer. As Camilla Russo from the Defiant wrote, "if DeFi teams can learn anything, retroactive incentives to value-added actors is a clear path to decentralization."

The biggest difference between 2017 and 2020 is that many of the tokens today are being created AFTER a company has already found product market fit. Instead of tokens being issued simply to fund pipe dream “decentralized projects” with low probabilities of success, many of today’s leading tokens are being used to enhance already thriving ecosystems and growing customer bases. Many of these tokens are created and structured (and often restructured) in a way that furthers that product market fit by bootstrapping customer growth and better aligning incentives between company and customer. Companies and projects have had years of history to study both the successes and failures, and are thus responding by issuing tokens that accrue real economic value via revenue and fee growth that can be passed through to token holders.

Uniswap just proved this.

Binance May Have Answered “What is a Pass-Thru Token Worth?”

Binance is one of the largest centralized exchanges, though it’s more of a prime broker at this point given its wide array of product offerings. Binance was also one of the pioneers of “pass-thru tokens” -- tokens that exhibit both utility-like features and equity-like features. The Graham and Dodd of digital assets has yet to release an agreed upon framework for valuing unique investment structures like these, but last week we may have been given our first clue.

The key to valuing pass-thrus is to understand the utility value and the equity value, separately. The financial value comes from price appreciation, as well as expected dividends, while the utility value comes from how productive the asset is:

- Do you receive discounts for using the token?

- Can you stake the token to earn rewards?

- Can you use the token as collateral?

The BNB token already has a unique set of features and attributes -- the company “burns” tokens periodically using a portion of profits, the BNB token can be used as collateral for trading derivatives, it can be used to receive a discount on trading fees, and to participate in Binance Launchpad IEOs (Initial Exchange Offerings). Most recently, BNB announced “yield farming”, allowing users to stake their BNB tokens on the Binance Launchpool platform, entitling them to earn rewards in the form of other tokens. This is where it gets interesting.

Immediately following this announcement, the price of BNB jumped as investors rushed to accumulate tokens in order to stake them and earn a yield. However, the BNB curve traded in backwardation, with the December BNB futures contract trading at a 15% discount to spot. This spread may be viewed as the market pricing in the difference between financial value (futures) and utility (spot minus futures). The utility of the BNB token only benefits tokenholders who physically own the token, as you cannot stake synthetic long risk on the Launchpool platform. As more and more derivatives markets develop for tokens, we’ll be able to start interpreting how the market values different attributes of tokens separately.

Binance Futures Curve is in Backwardation

Notable Movers and Shakers

This was a week that would make the late Charles Dickens proud - for Bitcoin (+6%) and Ethereum (+1%), it was the best of times. For the rest of the market…not the best. Bitcoin dominance crept up 2% this week, with only 17 of the top 100 assets by market cap finishing the week positive. This week we focus on Bitcoin, whose metrics are very telling:

- Bitcoin Difficulty made a new all-time high this weekend, re-adjusting to 19.31 T.

- Bitcoin Hash Rate made a new all-time high this weekend, currently at 140.61 EH/s.

- Bitcoin Hash Price (miner revenue per Terahash) made all-time lows last night, currently resting at $0.0728 ($/TH/S/DAY).

- There are now 10,342 Bitcoin nodes distributed around the world.

What We’re Reading this Week

Libra Adds to its Rank While the EU Squashes its Efforts

Libra, the stablecoin project created by Facebook, was busy last week hiring an HSBC veteran as its new Managing Director followed by the addition of Blockchain Capital to its association. These positive strides were overshadowed, however, by a joint statement issued on Friday from five EU members regarding stablecoins. Germany, France, Italy, Spain, and the Netherlands announced that stablecoins should not be allowed to operate within the EU until regulatory, legal, and oversight challenges could be addressed. The European Commission is planning to release its regulatory proposals for stablecoins later this month and it is clear that they will directly impact the Swiss-based Libra project.

Last week, digital asset exchange Kraken was approved by the State of Wyoming to form a Special Purpose Depository Institution (SPDI), effectively becoming the first digital assets company to receive a U.S. bank charter. The charter is recognized under federal and state law and will be the first U.S. bank to provide services such as deposit-taking, custody and fiduciary services for digital assets. Although approved as a bank, Kraken will not use fractional reserve banking and will instead have 100% of deposits on hand. The approval is a huge stride forward in digital assets as Kraken will now allow customers to seamlessly transact between traditional fiat-based systems and the new digitized world of digital assets.

According to a study published last week, Alibaba is set to be the largest blockchain patent holder by the end of the year, exceeding patents held by IBM. Year to date, the Chinese tech conglomerate has published ten times as many patents as IBM, putting it on track to exceed IBM’s patent count by the end of the year. Broadly, the study found there has been a surge of blockchain patents published in 2020 compared to 2018 and 2019, with most of the patents published by Fortune 500 companies not smaller businesses rooted in the blockchain space. The race to patent the technology is counter to the open-source nature of the digital assets community, which has led Jack Dorsey of Square to set up a non-profit group to pool patents and preserve the industry’s open source ethos.

The Central Bank of the Bahamas is set to launch its central bank digital currency (CBDC), called “Sand Dollars”, next month, making it the first country to roll out a digital currency nationwide. The goal of Sand Dollars is to drive greater financial inclusion among the island's residents, 90% of whom use mobile phones as of 2017. Sand Dollar transfers are made via mobile phone and will still require AML/KYC to open an account. The new digital dollar will exist alongside and be pegged to the Bahama dollar which is pegged to the USD. The country plans to slowly retire the Bahamian dollars as Sand Dollars will only be issued based on demand from users. The Bahama’s digital currency launch will be interesting to watch as it may inform many other countries that are considering similar routes.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency