Source: TradingView, CNBC, Bloomberg, Messari

Bull Markets are Harder Than Bear Markets

You’ve heard me say it before, but bull markets are way harder to invest in than bear markets. It’s so tempting to sell when a token gains 50-100% in a week, and it’s even harder to buy after a token rises that much if you missed it. The liquidity of these tokens, and visible price moves, may actually be damaging investors’ abilities to process the moves objectively, and on longer time frames. In a bear market, you ration your cash, spend weeks or months investigating opportunities, and deploy money slowly into investment ideas that have plenty of time to germinate. In bull markets, you often have to make decisions in hours, with less information, higher opportunity costs, and hundreds of distractions, including other traders tripping over themselves to buy tokens you haven’t even heard of, with leverage.

I often think about the difference between credit and equity investors to understand market psychology better. Credit investors have asymmetric downside as their gains are capped but their potential losses are large, whereas equity investors have known downside and unlimited upside. That risk/reward backdrop alone often makes credit investors more defensive and makes equity investors more aggressive. It’s much easier for credit investors to invest in a bear market when they can point to depressed valuations. In contrast, equity investors thrive in bull markets and can seemingly justify any move higher. Digital asset investors are, therefore, the ultimate bull market investors, as there is seemingly no price too high given the potential upside and no real way to kill a bad project through bankruptcy, but also far fewer agreed-upon valuation anchors.

In August 2020, we

discussed a similar insane rally (it turned out not to be that silly as the market has rallied much more since). In March 2024, we

discussed a similar insane rally (once again, it turned out not to be that silly as the market has rallied much more since). And here again today, we’ll discuss another rally in digital assets that seems silly but may once again prove to be just the beginning.

So let’s check in on where we are in this crypto rally. The market has been yelling for 3 months (beginning September 6th), what the ideal portfolio construction should be:

- BTC

- SOL

- Blue Chip Memecoins

- SOL ecosystem tokens

- Base Ecosystem tokens

- Crypto Equities

- AI Tokens

- A few newer tokens that the market has latched onto (i.e. SUI)

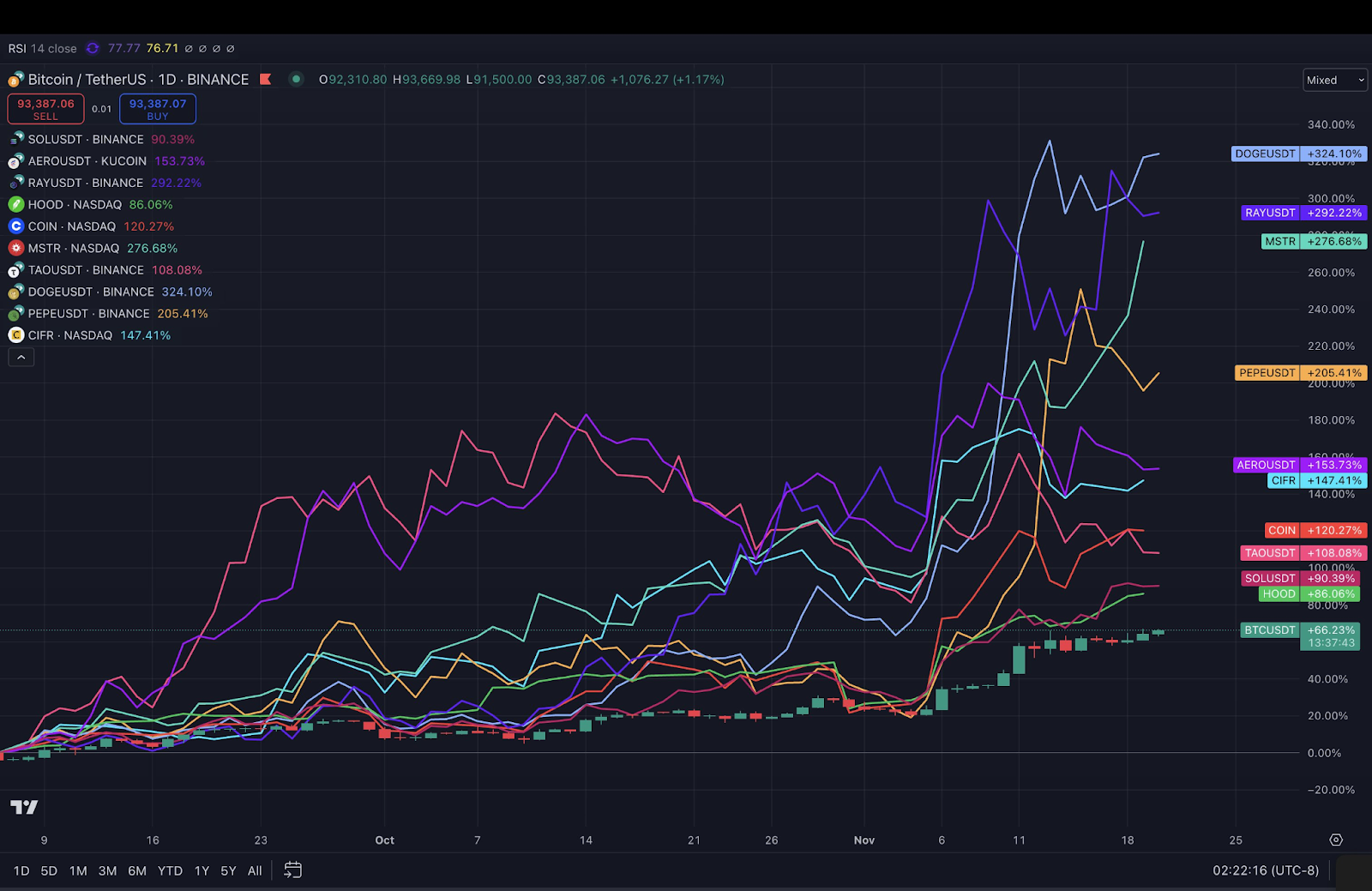

Up until this past week, these have been the consistent winners. A select few are shown below:

Source: TradingView

The market has also been very clear about what not to own:

- ETH

- Any of the seemingly endless number of ETH Layer 2 tokens

- ETH DeFi

- DePin

- Gaming

- NFTs

If you have tried to trade any of these laggards, you know there has been almost no consistent daily demand for tokens in these sectors.

And all of this, for the most part, made sense, even if only in retrospect. You could certainly justify the following:

- BTC = credit default swap: on continued deterioration of trust in banks and governments, including inflation and runaway debt

- ETH = Blackberry: Slow, outdated (or maybe Microsoft – better for Enterprise, not for consumers, but we have no real enterprise demand yet)

- SOL = iPhone: 10x faster than Blackberry, way better UX, more apps, social consensus

- Memecoins = the equivalent of trading daily options, and a middle finger to Wall Street and society

- SOL and BASE: growth engines.As measured by organic (non-incentive driven) growth, have been the two fastest growing chains (honorable mention SUI)

- AI Tokens: Rising star of blockchain integration. AI has been dominating attention since the rise of GOAT, and now we have hundreds of AI Agents spawning every day (perhaps we’ll write about the rise of AI agents next week)

Anyway, as I said, up until the past 2 weeks, this all made some sense. And then the silly season began:

- Ripple (XRP) +183% MTD

- Cardano (ADA) +212% MTD

- Stellar (XLM) +483% MTD

- Hedera (HBAR) +209% MTD

- The Sandbox (SAND) +231% MTD

The list of tokens with ridiculous monthly moves higher goes on and on. Coinbase is once again the

#1 finance app. Trading is gambling again. People I haven’t spoken to in 3 years are texting me asking if they should keep “fill in the blank” token, many of which I’ve never even heard of. Many tokens that have not had a pulse since 2021 are back en vogue. Remember Decentraland (MANA)? +147% MTD. How about VeChain (VET)? +104% MTD. Does Enjin (ENJ) still exist? Sure does, I guess, +104% MTD. Surely IOTA must be dead right? Nope, +104% MTD. EOS is definitely dead (+94% MTD). Basic Attention Token (BAT) hasn’t been used since 2019… +82% MTD. Axie Infinity (AXS), 2021’s crash and burn artist, +72% MTD.

We’ve had no less than 20 full-time employees at Arca for the past 4 years, working around the clock to understand tokenomics, sector growth, and future applications of blockchain technology, and few, if any of those mentioned above have warranted more than 5 minutes of discussion over the past three years, based purely on any visible metrics of adoption, growth or cash flows. At the same time, any one of these could easily resurrect themselves and become important again. The tokens will continue to trade no matter what happens to the team / project, and it's essentially impossible for any of these protocols to file for bankruptcy. Smart contract platforms are, in very basic terms, just app stores. They are blank canvases. As long as the blockchain produces blockspace, even if the app store is empty today, there’s nothing stopping developers and companies from deciding to build the apps of the future on these chains. Decentralized apps can be a ghost town for years, and then all of a sudden, users come back, and the flywheel starts up again. Said another way, most of the protocols and apps in this space are more “what could be” than “what has happened”, and there’s a lot of hope that “fill in the blank project” will be one of the ultimate winners.

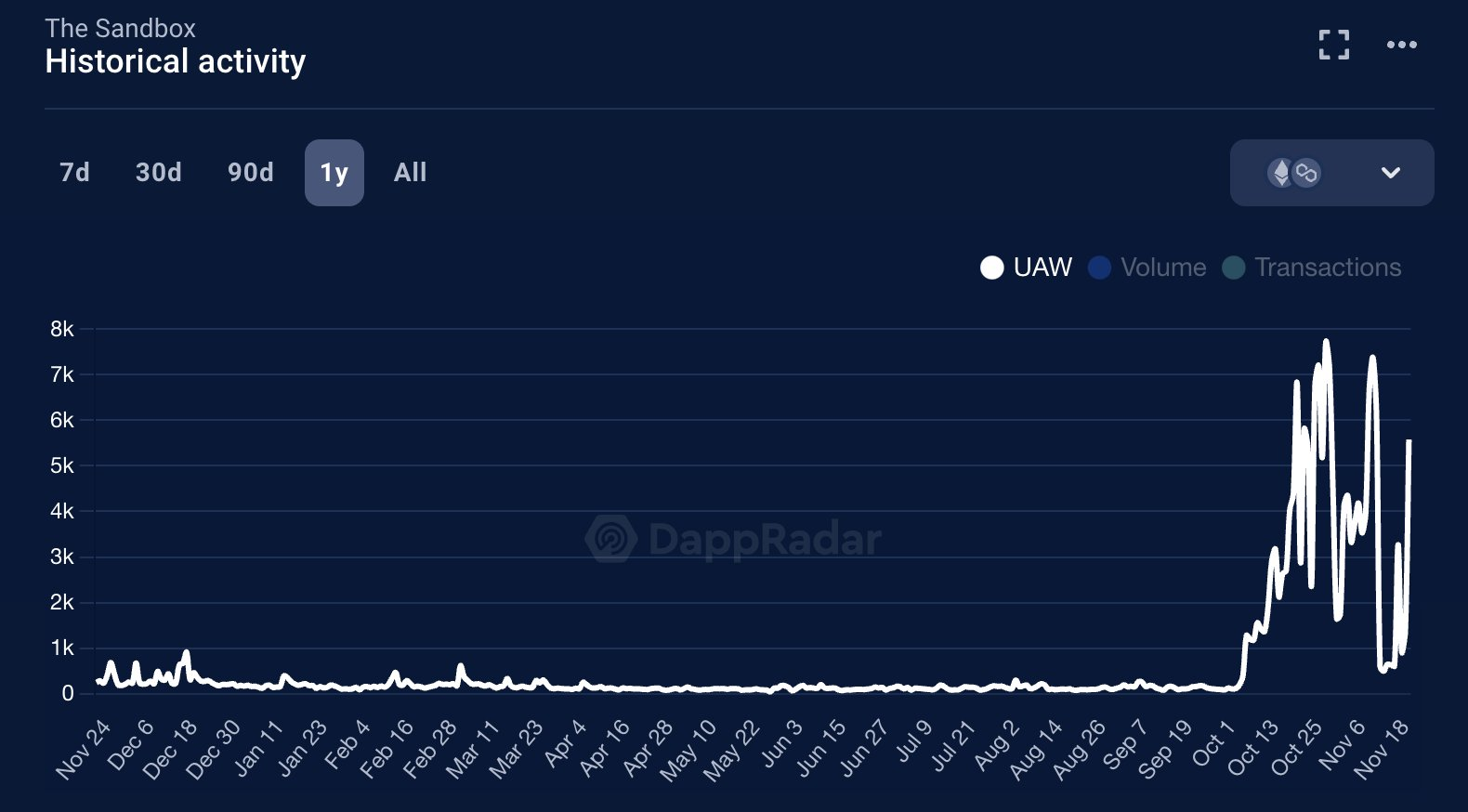

Am I predicting this will happen to the ones mentioned above? No. Would I be shocked if it did? Also no. This is what makes investing in a crypto bull market so difficult. Some legitimate blockchain projects are growing and increasing their value proposition, and anyone would agree with this if they looked at various metrics. There are others that no matter how you look at them, you’re still left clueless. Often, price attracts users rather than the other way around. I mentioned Sandbox (SAND) above – a once-hot metaverse startup with incredibly large VC backing in 2020 and 2021 that has been virtually dead for years. Daily wallets just went from 100 per day to 7000 last week, which sure sounds like a lot of growth, but in reality, that's going from flatline dead metrics to now only “mostly dead”. But there is a pulse, at least.

Source: DappRadar

So how the hell are you supposed to invest in a space with seemingly infinite tokens to choose from and no real rhyme or reason for why many of them are flying higher recently? As our friends at Bitwise Asset Management

suggested recently, one solution is passive index investing:

"As an investor, you’re faced with two options. You can try to pick and choose the winners, researching dozens of different blockchains and their unique tokenomics and fundamental drivers. Or you can bet the field, buying a diversified index fund that holds the leading assets on a market-cap-weighted basis."

And that’s certainly one option. However, the issue here is with “market-cap weighted”. It’s hard, using any sort of actual investment framework, to justify the prices of the majority of the Top 25 by market capitalization, which essentially means index weighting is just perpetuating a broken system of buying legacy tokens with no value proposition. This is no different than those who still buy Litecoin (LTC) or Bitcoin Cash (BCH) just because they were grandfathered onto so many platforms in the early days. Thanks for the great set of investment options, Paypal!

Source: Paypal

Another logical answer is active management (which, disclaimer, Arca focuses on). This is another viable choice if you want to at least have a rationale for the investments that you own. But it’s no secret that most actively managed funds have underperformed Bitcoin since the middle of 2023. While that’s the equivalent of comparing a small-cap equity manager to Nvidia, it is the standard that many in this space are held to, and many active managers have exhibited major style drift trying to keep up with the memecoins and high flyers.

Which leaves the third option that many investors have chosen – just ignore this space completely. And, well, that certainly hasn’t been the right answer either. We’ll let Rick Wurster, incoming CEO of Charles Schwab,

tell you how that plan has gone:

“I have not bought crypto, and now I feel silly.”

And he should feel silly. The technology, and the crypto investment landscape, is real. But at the same time, we certainly understand the trepidation and confusion and understand many who feel paralyzed by the inability to separate signals from noise. There are no barriers to entry in this industry, and everything from legit growing companies to outright scams gets the same coverage and airtime.

Bull markets are hard. But make no mistake, we are in one. There are decades where nothing happens, and there are weeks

where decades happen. The political, regulatory, and sentiment shift post-election is the biggest positive event in the industry. Which means both real growth and nonsensical growth will continue. Whether or not your investing strategy is the right one is challenging to know in real-time. But it has been pretty well established that no allocation at all is the wrong choice. Separating the wheat from the chaff has never been more challenging.

A Quick Check-In on DeFi

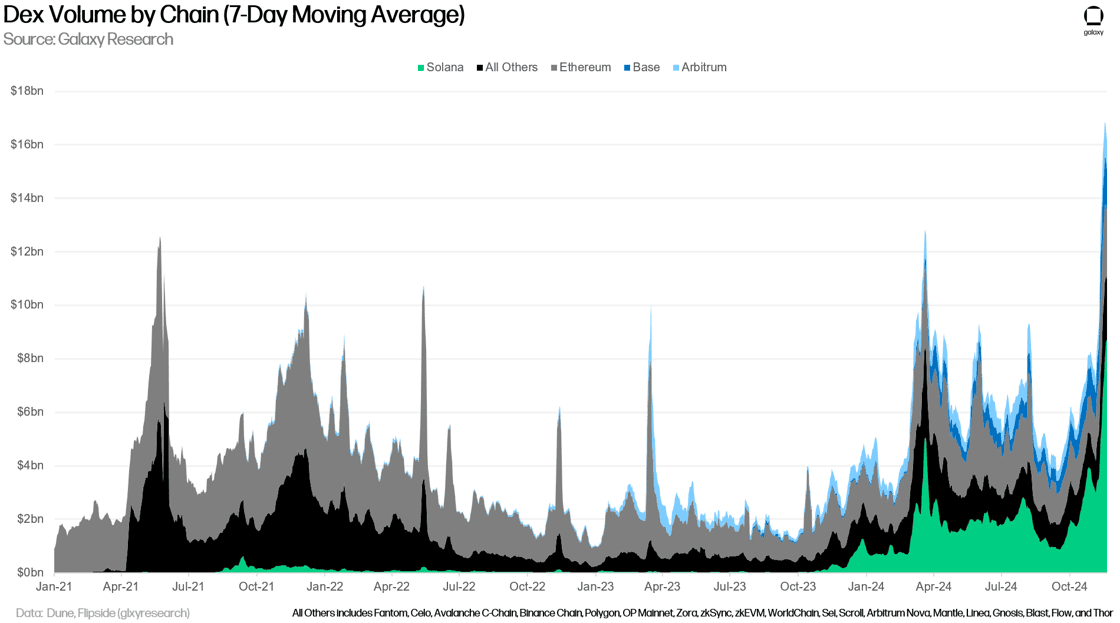

Decentralized Exchange (DEX) growth is real. The combined on-chain DEX volume of 23 chains reached an all-time high of $16.8 billion last week. Additionally, four of the top 10 outright single-highest days of DEX volume (the fifth, sixth, seventh, and ninth) came in the nine-day period ending November 20, 2024, with $19.8 billion being the highest day over the period. The highest single day of DEX volume ever was set on May 29, 2021 at $28.2 billion, and hasn’t been closely rivaled since March 12, 2023 when DEX volumes reached $23.2 billion.

Source: Paypal

Meanwhile, on-chain lending is hitting all-time highs as well. Aave crossed $30 billion in deposits, making it close to a Top 50 bank. All of this is being done without the majority of the world’s assets even being able to participate in DeFi rails yet. Imagine what will happen when your stocks, bonds, and hard assets can be used for collateral.