What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 8/9/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+3.2%

|

+62%

|

|

Bloomberg Galaxy Crypto Index

|

+7.6%

|

+94%

|

|

S&P 500

|

+2.4%

|

+4%

|

|

Gold (XAU)

|

+5.0%

|

+35%

|

|

Oil (Brent)

|

+3%

|

-32%

|

Source: TradingView, CNBC, Bloomberg

Bull Markets Are Hard to Analyze

Behavioral finance is on full display right now. To understand market psychology better, I often think about the difference between credit and equity investors. Credit investors have asymmetric downside as their gains are capped but their potential losses are full, whereas equity investors have known downside but unlimited upside. That risk/reward backdrop alone often makes credit investors more defensive and makes equity investors more aggressive. It’s much easier for credit investors to invest in a bear market when they can point to depressed valuations, whereas equity investors thrive in bull markets and can seemingly justify any move higher.

With the Federal Reserve, the Treasury Department, the President and foreign leaders all promoting loose monetary and fiscal policy, every asset class is now in a bull market. The Nasdaq set another record last week, so did Gold. Other commodities hit multi-year highs and even oil hit a post-March high. Every inflation-protected and/or technology asset has been on fire, fueled further by the Fed’s commitment to hit its inflation target, despite a long history of never hitting any targets or goals. Somehow, Treasuries rallied to new highs as well.

This is making some investors very comfortable, while making others extremely uncomfortable. The bulls are pointing to better-than-expected economic data, improved trends in U.S. coronavirus cases, expanding business activity for the services sectors, and better than expected growth in jobs. Equity analysts are raising price targets just to keep up with the fact that their old bullish price targets are now ridiculously low compared to current trading levels. SPACs are being raised at record levels, which is basically an advertisement for “we’ve run out of ways to invest our money”. Apple (AAPL) alone added $1 trillion in market cap since March. It’s hard to even comprehend a number like that.

The bears, meanwhile, are focused on the fact that all of these “beats” are off extremely depressed levels and expectations, and fundamentals don’t justify prices. While this may of course be true, it’s really hard to make sense out of bull markets.

Digital Assets - The Ultimate Bull Market

Digital assets check the box for both technology and inflation-protection. As such, it’s not entirely surprising to see such rapid price growth. In a recent note, Coinbase noted, “institutional applications continue to rise and are almost 3X what we were seeing this time last year.” Technological progress combined with new money typically leads to large price increases.

Yet many investors are either flummoxed by, or completely unaware of, this asset class’ growth, largely because the areas that are driving the price gains don’t fit traditional media’s agenda and aren’t represented in traditional investors’ portfolios. To see why, it’s helpful to split digital asset investors into equity-like bulls and debt-like bears.

There are essentially four types of investors in digital assets:

- Bitcoin-only investors

- Algorithmic / Quant funds

- Venture Capital investors

- Liquid, research-driven fundamental investors (like the strategies we run at Arca)

The Bitcoin-only investors seem uninterested in the evolution of this asset class. The Algo/Quant investors don’t really care what constitutes this asset class as long as the underlying assets are liquid and can be modeled with predictable correlations and betas. The VCs can see so far into the future that they sometimes miss what is right in front of them, preferring to place long-term bets with lockups long before a company or project has proven product market fit (a seemingly unnecessary legacy strategy in a liquid and ever-changing asset class). The liquid, research-driven fundamental investors, meanwhile, have adapted constantly and in real-time to where the growth is occurring.

There are many unhappy digital asset investors right now, as the bull market continues at a torrid pace but is leaving many of the early investors behind. New, open-minded “Equity”-like investors are justifying the moves, albeit by constantly moving the goalposts to keep pace. “Credit”-like investors are finding excuses for why this rally makes no sense.

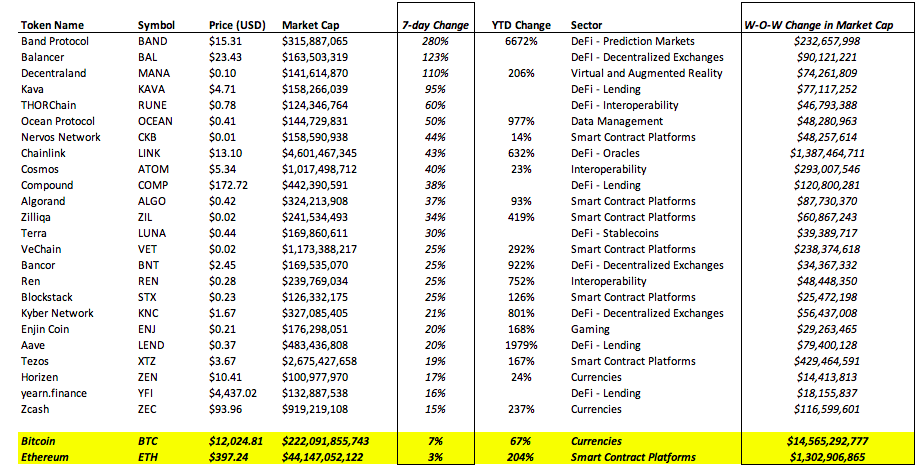

Largest Prices Gains Amongst Digital Assets Last Week

The price moves for many digital assets last week were, in some cases, silly. And very few of the high-flyers are owned by three of the four types of investors mentioned above (the exception being a few VCs and the fundamental research investors), and most certainly are not represented in the ill-constructed “crypto index” products. As such, there are a lot of “credit-like” investors waiting for Bitcoin to catch up or downplaying the strength in small cap tokens and projects. However, a rational investor with no preconceived notions might look more objectively at the facts. The growth in market cap of the entire digital asset ecosystem grew by just $26 billion last week (from $338 billion to $364 billion), and the top movers shown above gained only a paltry $3.7 billion in market cap. May I remind you that Apple alone gained $1 trillion in market cap since March? A $26 billion gain across an entire asset class is literally nothing. These small cap tokens are gaining in market value in many cases directly in line with their increased usage, and are heavily represented by the fast-growing Decentralized Finance (DeFi) sector. While market cap is not a great measuring stick for digital assets, the increased wealth created by these moves might actually be understating both the actual growth and growth potential.

Bull markets are much more challenging than bear markets, and behavioral finance is again on full display. It’s hard not to sell when a token you own is up 100% in a week, and it’s even harder to get involved after a token rises that much if you missed it. The liquidity of these tokens, and visible price moves, may actually be damaging investors’ abilities to process the moves objectively. For context, with leading private companies, the growth in valuations year-over-year is often huge. But we only get these data points a few times throughout the trajectory of the company, usually only after a successful capital raise. When a leading private company has a massive jump in valuation, we tend to look at the bigger picture. But objectively, the only way to get billion dollar jumps in valuations year-over-year is to have several $10-100mm weekly moves up and down throughout the course of the year. For instance, Robinhood just raised money at an $8.6 billion valuation, up from $7.6 billion a year ago and up from $1.3 billion just 3 years ago. However, back in March 2020, the company had so many outages and forthcoming lawsuits from unhappy customers that it’s conceivable that the company’s true valuation may have dropped by several hundred million dollars during this time, only to bounce back with record user growth and volumes in the Q2 and Q3 this year. A daily or weekly price monitor of RobinHood’s equity would have likely looked very similar to what we’re seeing in digital asset prices today.

Growth in RobinHood Private Valuation vs User Growth

.png?width=719&name=unnamed%20(35).png)

Source: Robinhood Company Presentation, Crunchbase, Arca Estimates

It’s worth noting that RobinHood is simply reinventing one oversaturated and expensive area of finance, while digital assets are reinventing the entire financial ecosystem, capital formation and customer bootstrapping process. Bull markets are very hard to justify, but stepping back to see the forest through the trees will likely serve investors well in the near future.

Notable Movers and Shakers

One might think that Bitcoin finishing the week up 3% would lead the outside world to believe that digital assets had a good week, and they wouldn’t be wrong. However, the rest of the space offers some telling statistics as to just how well it fared last week: 92 out of the top 100 assets finished the week positive, 61 out of 100 finished the week with higher gains than Bitcoin, and 35 out of 100 assets outperformed Bitcoin by over 10%. This is even more impressive when you take into consideration that 7 assets are stablecoins, which are designed to remain relatively stagnant. Writing about all the moves from last week would convert this section into a paperback book, so instead we focus on two that particularly caught our attention:

- Band Protocol (BAND) is the latest beneficiary of a Coinbase listing, which caused it to gain 43% intraday on Wednesday. Band Protocol benefits from the surge in DeFi lately (as it is a cross-chain oracle service provider using the Cosmos-SDK), coupled with the high beta between BAND and LINK (which had a week of its own, gaining 66%). BAND rode the listing throughout the end of the week, finishing up 271%.

- Nexus Mutual (NXM), a decentralized blockchain-based solution to traditional insurance mutuals, saw its token rise 150% week-over-week. Nexus ensures the risk of critical bugs in smart contracts across many DeFi applications. As second level thinking goes, when DeFi rises, the need to ensure the risks rises as well.

What We’re Reading this Week

According to financial statements from Square, the company made $875m in Bitcoin revenue during Q2, over a 150% increase from Q1 2020. The company, however, only profited $17m from its Bitcoin operations with costs totaling $858m. The financial statements also indicated that Square believes the increased activity was the result of an increase in Bitcoin activity and an increase in customer demand. It further mentioned that transactions across its platform were up during Q2, which it attributes to government relief programs (stimulus checks and unemployment benefits) related to the coronavirus pandemic. Regardless, the increased activity indicates there is an ever-increasing appetite for Bitcoin exposure among retail investors.

Last week, Goldman Sachs appointed Matthew McDermott, a financial markets veteran and prior head of internal funding operations, as the new digital asset global head for the investment bank. McDermott is very favorable to the future of digital assets and the digitization of financial markets stating, “In the next five to 10 years, you could see a financial system where all assets and liabilities are native to a blockchain, with all transactions natively happening on chain”. In addition, McDermott also confirmed in an interview that Goldman is looking into launching its own digital asset and may partner with JPMorgan or Facebook in the process. The appointment and these statements show that Goldman is taking a revamped approach to the digital assets market and will likely be a key player to watch among traditional players.

INX, a cryptocurrency and security token exchange based in Gibraltar, has decided to conduct an IPO offering to U.S. investors before the end of 2020. Originally filed as an offering to non-U.S. investors in a $130m offering, the firm last week refiled its offering to target U.S. investors with a raise amount of $117m. Despite the scaled back offering, which will be offered to investors in tokens, INX will still be the largest crypto IPO and the largest token IPO if successful.

The newest commissioner of Japan’s Financial Services Agency (FSA), Ryozo Himino, spoke last week about his concerns about loosening restrictions on cryptocurrency trading and activities saying “deregulating bitcoins and other cryptocurrencies may not necessarily promote technical innovation, if doing so simply increases speculative trading.” Japan is known to have one of the most comprehensive set of digital asset regulations worldwide, with licensing requirements for exchanges. However, the FSA has been keenly watching exchange activity after the 2018 hack of Coincheck and may introduce further regulation to crypto trading.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency