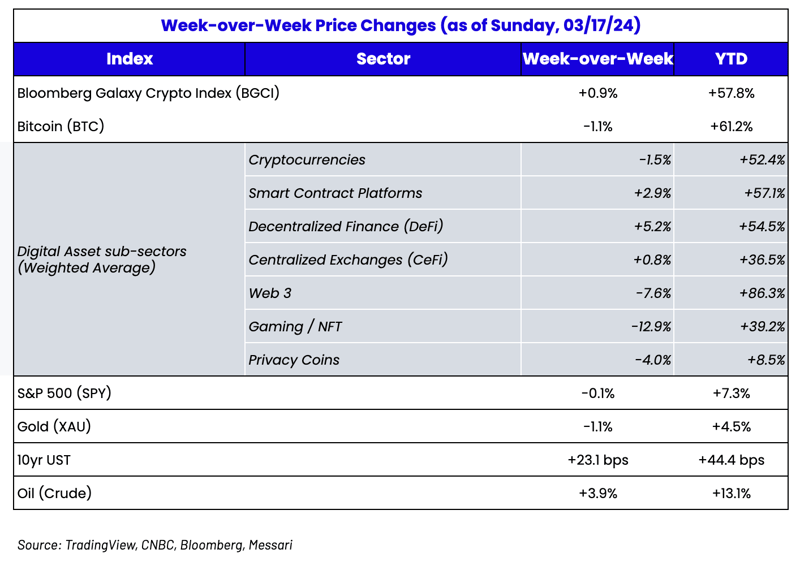

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari

A Much-Needed Reversal

Bear markets are easier to trade than bull markets. Not to say that bear markets are more fun than bull markets because they most certainly are not- and are definitely not more profitable. But they are easier. In a bear market, you ration your cash, spend weeks or months investigating opportunities, and deploy money slowly into investment ideas that have plenty of time to germinate. In bull markets, you often have to make decisions in hours, with less information, higher opportunity costs, and hundreds of distractions, including other traders tripping over themselves to buy with leverage.

There’s no debate that we’re currently in a bull market for both equities and crypto. Forgive me if I, for one, take comfort in a little pause.

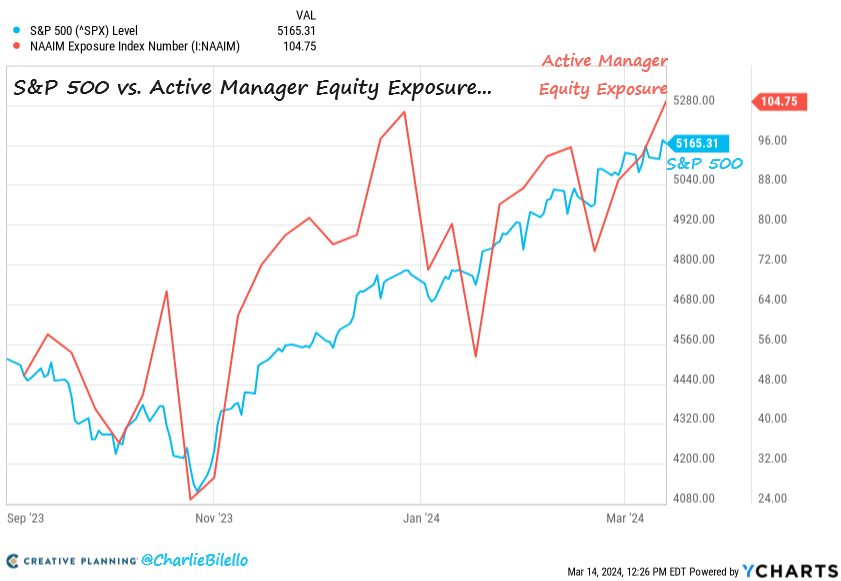

The S&P 500 declined moderately last week, registering its first back-to-back weekly decline since October, and Treasury yields were again higher. Active managers had less than 25% exposure to equities in late October when the S&P 500 was at 4,100. Today, their equity exposure has jumped to 104% (leveraged long), with the S&P 500 above 5,100.

This is their highest exposure since Nov 2021. The 10-year U.S. Treasury yield is now 45 basis points higher than at the start of the year, which is perhaps a bit odd in a year marked by higher stock prices due to some degree of expected rate cuts. Recent hot inflation data has spooked markets slightly ahead of this week’s FOMC and BOJ meetings.

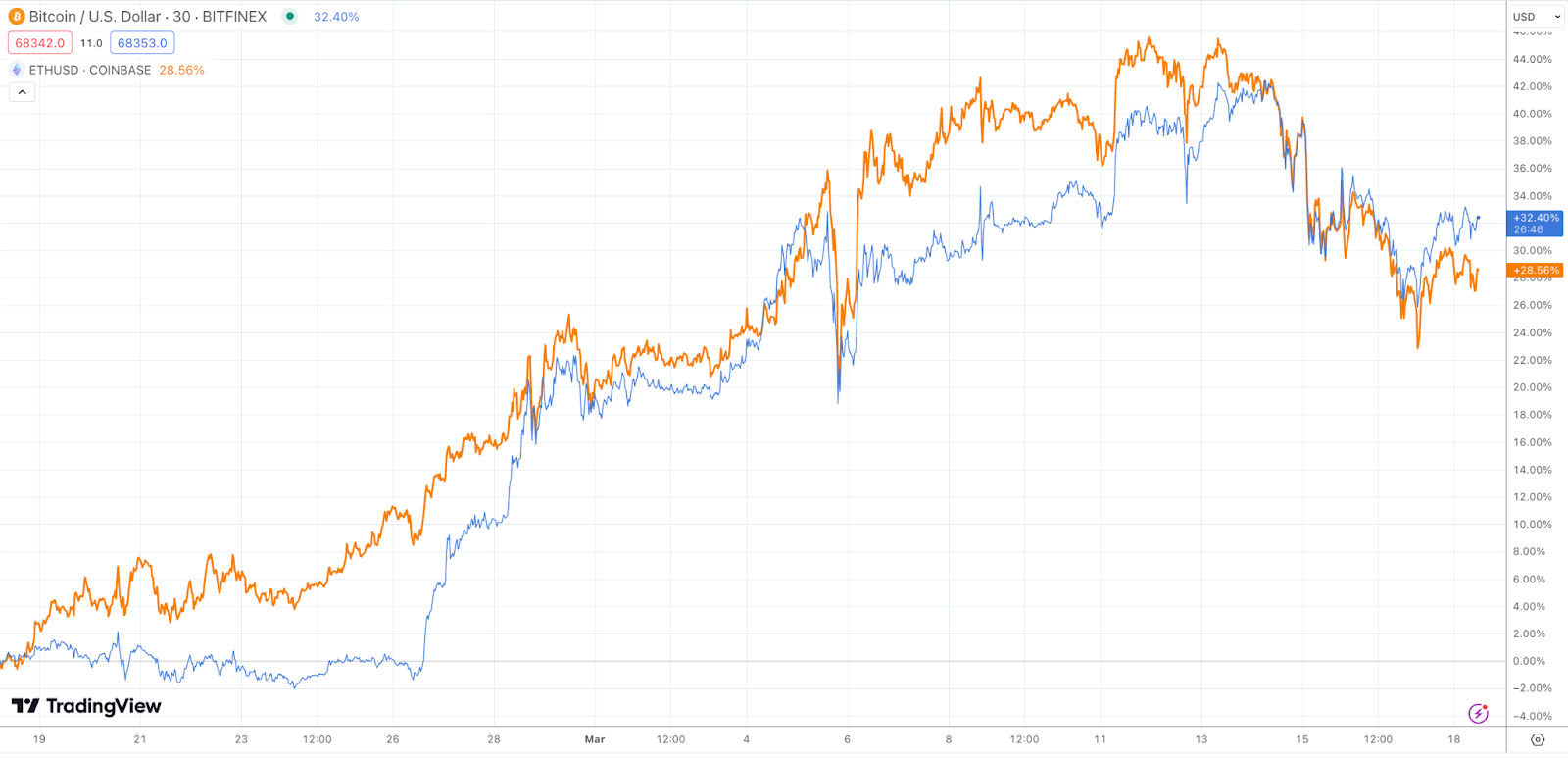

The digital assets market paused as well. After the total crypto market cap touched the $3 trillion mark, the overall digital asset market pulled back sharply, registering the first down week for the Bloomberg Galaxy Crypto Index (BGCI) since the end of January. While broad-based double-digit declines and large futures liquidations occurred late in the week, the week-over-week decline was much more modest, thanks to a good start to the week.

Source: BTC and ETH price via TradingView

These declines triggered another round of futures liquidations, similar to the one a few weeks ago after Bitcoin first re-touched its all-time-high Most of the liquidations came from the long side, though the whipsaw price action liquidated many shorts as well. It’s worth noting, however, that this correction was much smaller than the leverage washout in late February. Last week, futures liquidations were roughly half what we saw after BTC crossed its all-time high.

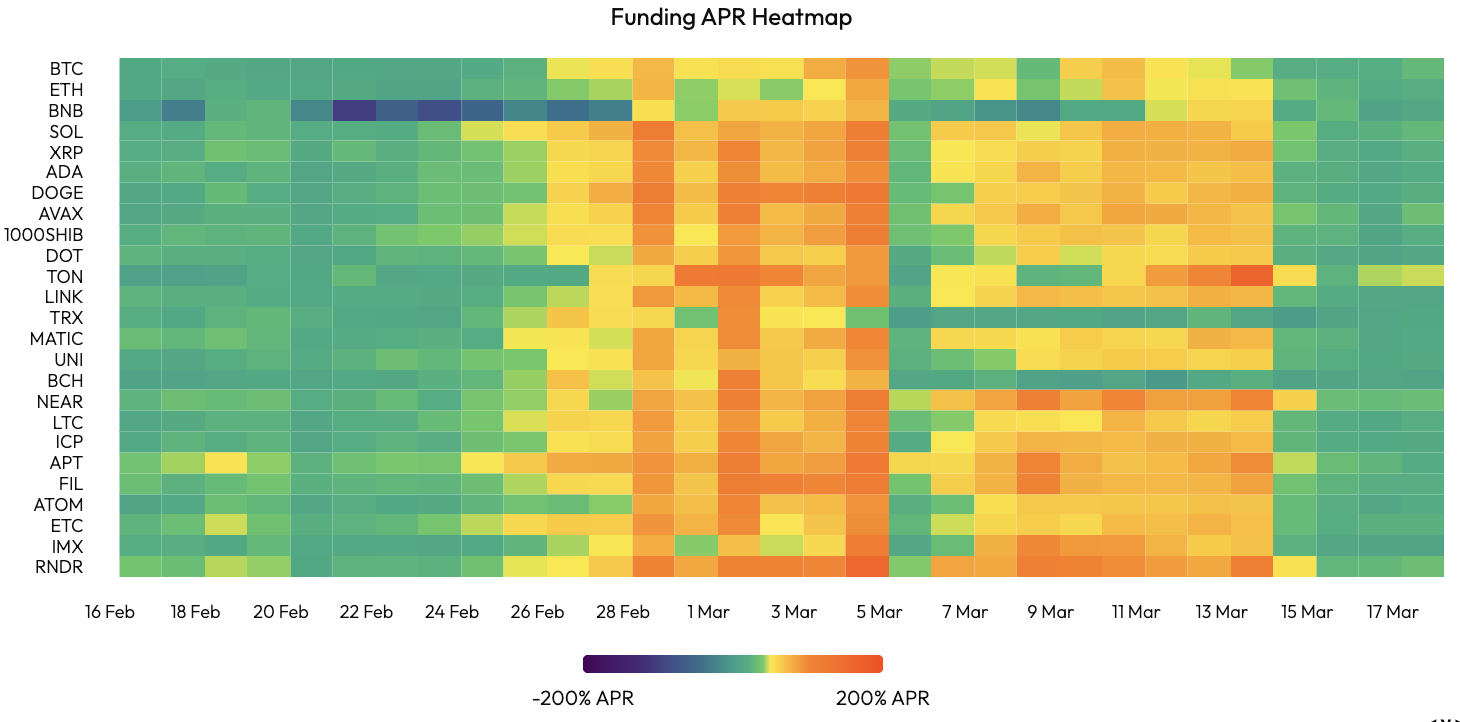

Naturally, these liquidations reset funding rates. Green is considered healthy and balanced. Similar to a sports bookie that tries to set the gambling line at a level that encourages equal action on both sides, a neutral funding rate encourages both long and shorts to participate equally. Orange means longs pay upwards of 50-100% annual rates to stay long, encouraging shorts to take the other side to receive this high rate. Orange is scary because it means all parties are on the same side of the boat, cash is in short supply, and no one is afraid to be long. Historically, these leverage washouts are a healthy reset for the market and give an “all clear” to resume an upward trend until, of course, sentiment rises so fast that animal spirits lever up again, and we rinse and repeat.

Liquidations have been a driving force of the increased volatility over the past month. BVIV and EVIV, volatility measures of BTC and ETH, respectively, have been on the rise even as the VIX has flatlined and MOVE, the bond market volatility index, has declined.

Source: TradingView

As I said, bull markets may be more fun than bear markets, but they are sure can be tricky to trade.

Solana Bucks The Trend!

While the sharp correction led to mostly lower prices, there were flurries of upside. Near (NEAR) got a boost ahead of this week’s Nvidia AI conference, as the NEAR CEO, Illia, will speak at the event. Other AI tokens also got a boost, with Bittensor (TAO), Render (RNDR) jumping higher over the weekend. Meanwhile, Solana (SOL) and its ecosystem have been strong in the wake of the announcement of the Tensor airdrop and the future launch of Parallel's Colony game on Solana. Parallel's Colony whitepaper announced the game would be built on Solana. Additionally, Tensor announced they would be airdropping their token soon. Solana's fees rose 146% week-over-week as memecoin trading ran rampant.

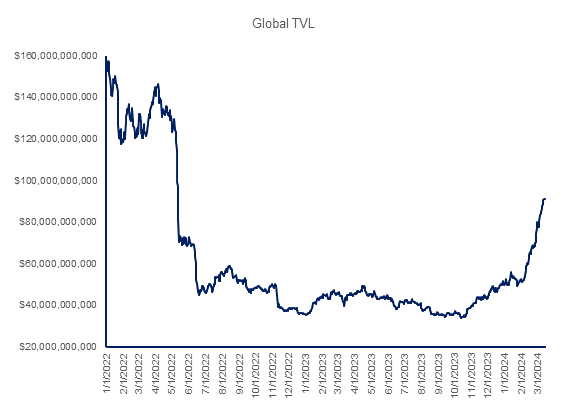

Global TVL has continued to advance sharply since early February and is now at its highest levels since LUNA.

Sources: DefiLlama and Artemis

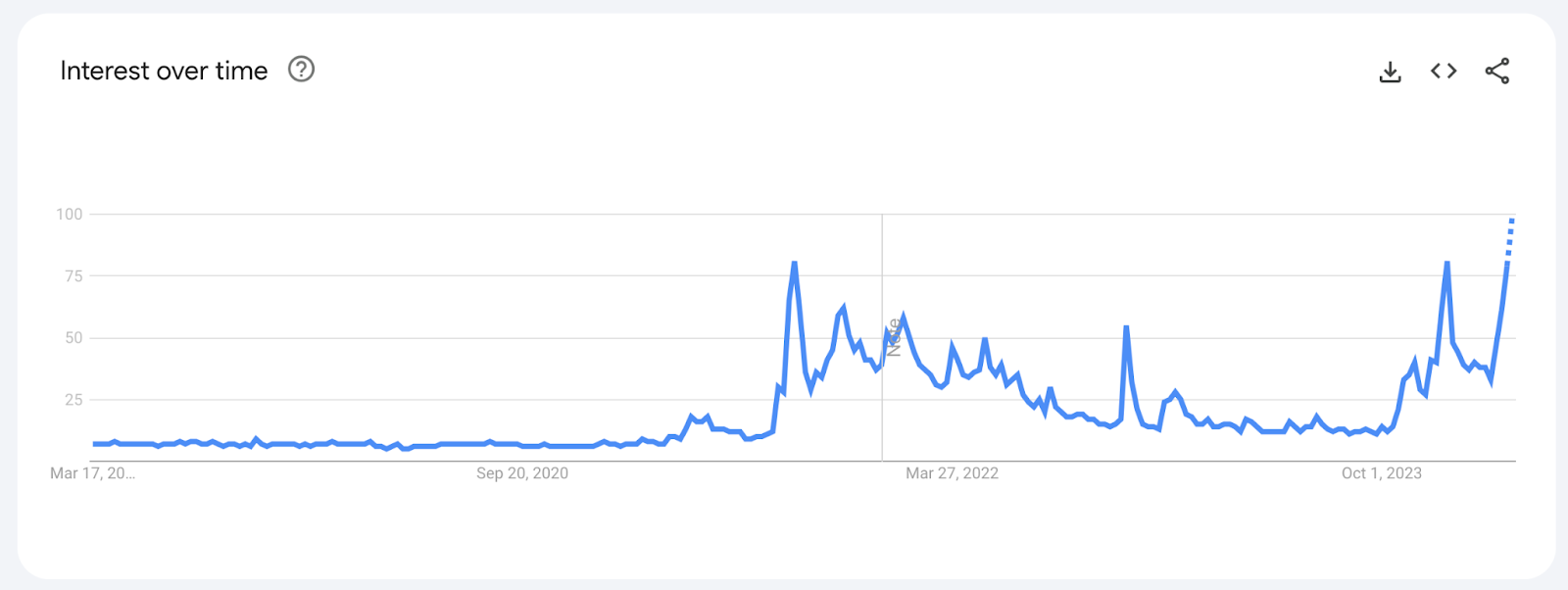

As the price of SOL exceeded $200, the search popularity of the word “Solana” in Google Trends reached 100, setting a record high in its 5-year history and eclipsing September 2021.

It’s also no secret that the FTX estate is shopping a large block of locked Solana (SOL) tokens, with some funds

even raising SPVs specifically to buy portions of this supply at a large discount to spot. When this block of tokens was initially shopped around by Galaxy Digital, who is running the FTX bankruptcy estate sale, SOL was under $100 and traders rushed to short SOL upon news of this impending supply.

Sound familiar? We wrote about this exact same fallacy in September 2023, and once again, SOL ripped higher as traders positioned short.

“It’s also worth noting that market makers and traders almost ALWAYS sell more ahead of known block sales than what actually comes to market. For example, if you know PIMCO is selling $100M of bonds, and ten funds sell $50M each to make room for it, how much of the $500M sold to make room for $100M actually cover their shorts profitably? Most of the time, those who sell early end up buying back higher.”

The irony in the SOL move higher is that it came on the heels of a significant upgrade to Ethereum, which was explicitly designed to lower fees to, in part, compete more with Solana. Last week’s decline in price came on the heels of one of the largest and most successful technical upgrades. Ethereum protocol developers successfully executed another network-wide upgrade on the world’s second-most valuable blockchain. The Dencun upgrade is designed to lower fees, and while it is still too early to gauge how much cost savings Dencun will bring to Layer-2 scaling blockchains, most market participants have been expecting up to 80-90% reductions. It is perhaps ironic that ETH fell -10% week-over-week, and Layer-2 chains like Arbitrum (ARB) and Optimism (OP) fell -16% and -24%, respectively, while SOL jumped +40%.

Again, bull markets are hard to trade.