The Digital Assets Rally Continues Despite Regulatory Crackdowns

For the last two weeks, we’ve discussed the U.S. regulatory crackdown on digital assets, which is no joke. The efforts have targeted stablecoin providers, exchanges, crypto banks, staking providers, and now, run-of-the-mill RIAs. You can’t even sneeze in digital assets land right now without a government agency or regulator giving you the stink eye. And yet, digital assets broadly gained again last week and have now been green for 6 out of the first 7 weeks of 2023. Last week’s rally was especially impressive, given a sideways equity market, rising Treasury yields, and a rising U.S. dollar.

Something has changed.

Those looking for a reason to sell, or stay uninvested on the sidelines, can certainly find plenty of reasons in Washington. But additional context helps to justify this rally:

1) As

we discussed in January, while the headlines in 2H 2022 were all negative, the equities of service providers suffered the most (likely zero recovery in bankruptcy). Tokens (Web3, Layer-1 and Layer-2 protocols, DeFi, etc.) were much more resilient and continue to show more upside and less downside than "crypto stocks." This resiliency has not gone unnoticed.

2) Most digital assets are still

"dot cryptos," much like the early "dot coms." The first crop of blockchain protocols and companies are infrastructure businesses that only exist because of blockchain. They are heavily levered toward user, transaction, and volume growth—all of which are flying right now. In 2022, low usage led to price declines, which led to a further lack of interest on the way down. Thus far in 2023, high usage has led to price increases, leading to more interest on the way up.

Source: Internal Arca Calculations

3) U.S. regulators’ attack on digital asset companies (which further segregates them from traditional banks and brokerages) is

short-term bullish for token prices. Fear of stablecoin regulation, specifically, is resulting in a rush to exit BUSD and USDC

in favor of BTC, ETH, and other tokens. As

Coinbase pointed out, the

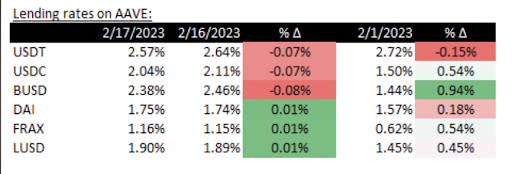

“high stablecoin dominance ratio of 18.0% (vs the total [digital assets market]) to start 2023 has likely enabled excess cash on the sidelines to be put to work. Indeed, the total stablecoin market cap has fallen by a net US$3.3B over the last six weeks.” Centralized stablecoins, specifically, are treated as riskier holds than decentralized tokens, which can be seen in the cost to borrow BUSD, USDT, and USDC versus what it costs to borrow DAI and FRAX.

Source: Aave

4) Basic Economics 101 suggests that an industry with perfect substitutes will never see an impact on price when one player is displaced. The U.S. regulatory crackdown on Kraken, Paxos, BUSD, USDC, and whoever is next has no long-term effect on prices, just like previous crackdowns. For example, when China exited Bitcoin mining (from 75% market share to 0%), there was no impact on price/hash rate as others filled the gap (for example, Texas). Similarly, when Bitmex was charged by the DOJ (going from a derivatives market share of 40% to 4%, there was no impact on derivatives/price as volumes just went to other venues. When FTX went down, Binance and dYdX immediately took its market share. When BlockFi and Genesis went down, Aave and MakerDao took that market share. The same is happening today.

5) The digital assets industry is global. Therefore, the actions of the U.S. are less important than the people in the U.S. think they are.

The entire industry continues to prove its anti-fragility. The latest crackdown may cut deeper, though, as it is a broad-sweeping proposal that seems impossible to carry out—the SEC last week

proposed new rules for the custody of client assets. While this will affect much more than just digital asset inventors (for instance, any fund that holds art, taxi medallions, or real estate that a qualified custodian cannot physically hold), it once again leans pretty hard on the blockchain industry. As

Matt Levine at Bloomberg writes:

“First, the effect of this rule is to ban registered advisers from trading crypto on most exchanges: To trade crypto on most centralized exchanges, you need to deposit the crypto on the exchange first, which destroys custody. You can trade stocks on the stock exchange because the stocks live at DTC and you own them through a qualified custodian, but if you trade crypto on Binance then the crypto lives at Binance and the SEC might have concerns.”

These rules bring up an interesting debate. Blockchain finance, by definition, relies on real-time settlement. The whole point of peer-to-peer trading and blockchain rails is instantaneously sending and receiving assets. So, if you want to trade, you pretty much have to:

- hold your tokens where you trade (e.g., an exchange)

- use self-custody and transact via DeFi (e.g., MetaMask to Uniswap)

- trade OTC and settle the transaction later (e.g., with Cumberland)

The custody rule, and other actions from Washington, D.C., indicate they will force T+1 (or T+3) settlement, or they don't fully understand that blockchain is T+0. It would be cleaner to say they do not intend to let individuals trade using blockchain rails.

So Where Is the Growth Happening?

Investable dollars continue to move quickly from theme to theme. Last week, liquid stakers, decentralized storage/computing, and Asia-based tokens noticeably outperformed the rest of the market. Additionally, airdrops, like from the NFT platform BLUR, had two noticeable effects:

- Activity surrounding this airdrop contributed significantly to ETH's most deflationary day to date

- Market participants feel richer when they receive an airdrop and are more willing to reach further out the risk curve

Activity begets activity. As ETH leans more deflationary -> ETH token price goes up -> more money to invest -> the flywheel is in motion. Separately, there has been a lot of talk about strong Chinese bidders. Chinese QE has money flowing into real estate and speculative assets, and we are seeing some of this affect token prices. With

Hong Kong potentially reopening as a crypto hub in June, bidding out of Asia may stay strong for a while.

Finally, dealers and funds expressed more bullish bets last week than we’ve seen since last summer. There were significant flows in derivatives last week, mainly looking for upside via futures and calls. In options land, we heard about all types of buys—BTC and ETH calls outright, covering short leg of call spreads, buying ratio 1x3s. These buys have resulted in a big move in skew as calls become cheaper than puts.

Between macro and regulatory concerns, you can climb a wall of worry and find plenty of reasons to stay sidelined. But looking specifically at digital assets through a micro lens, it’s a pretty clear risk-on rally.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari