The “CCC Rally”

Digital assets are on fire to start the year, but we’ll get back to that in a minute. Unfortunately, 2022 was such a difficult year for digital asset investing that most investors could be forgiven if they assumed the sky was falling and completely missed this hot start to the year. The only problem is that the data just doesn’t suggest that to be true.

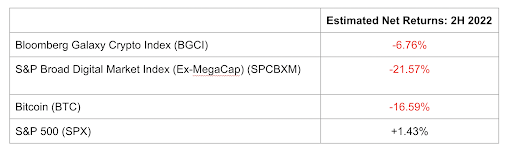

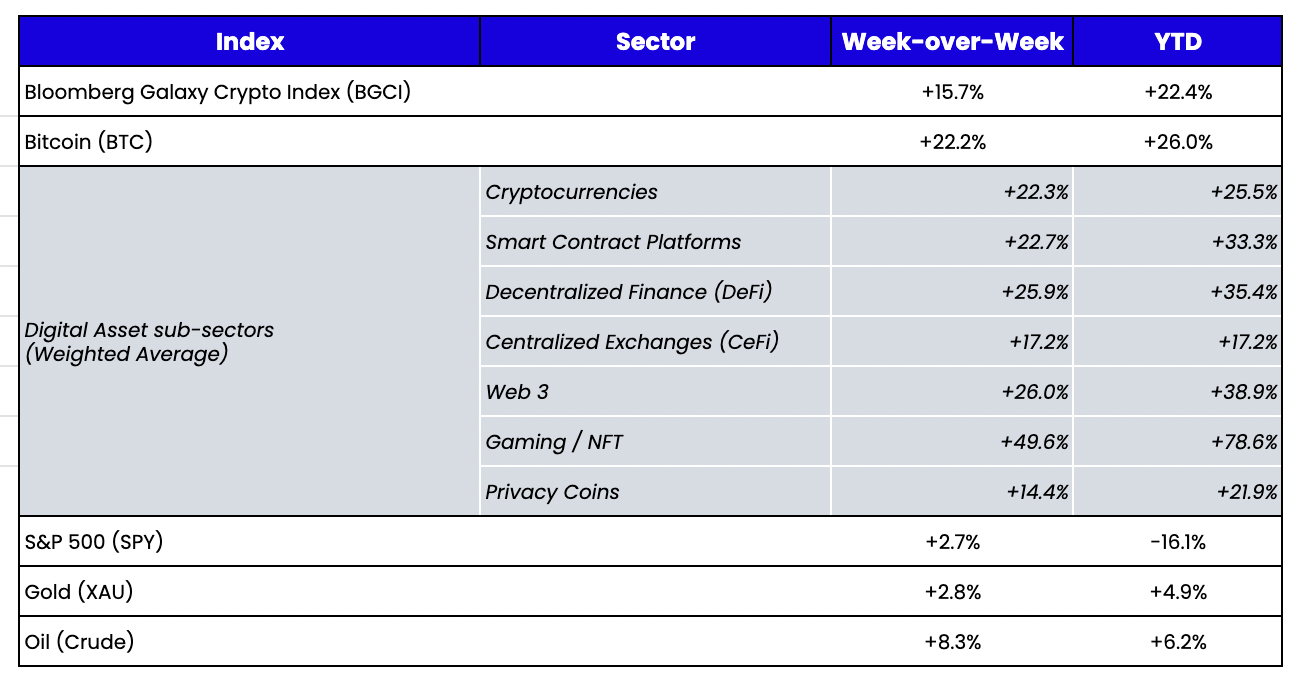

If you read the news, you would think the second half of 2022 marked the end of digital assets. Pack ‘em up, everyone—it’s over. But if you just looked at returns, the second half of 2022 was actually pretty benign. The Bloomberg Galaxy Crypto Index (BGCI) was only -6.76% in the second half of the year, largely dragged down by Bitcoin’s poor performance (-16%). Meanwhile, ETH (+13%), UNI (+5%), BNB (+13%), and MATIC (+61%) were a select handful of large-cap tokens that performed well in the face of an imploding system. There were, of course, some negative outliers—namely the tokens of companies that actually did go bankrupt (FTT, VGX, CEL)—as well as anything tied to the Solana ecosystem (SOL -66%). But in aggregate, most of the damage was done in the first half of the year when LUNA/UST collapsed and when macro events still influenced price (hint, they don’t anymore and haven’t mattered to digital asset performance, excluding Bitcoin, since June).

Most of the bankruptcies and fraud happened in the second half of 2022. Still, the investments in digital assets themselves are quite separate from the equity of companies that trade, lend, and custody these investments—many of which are failing and/or bankrupt and now worth zero. The irony, of course, is that most digital asset naysayers hide behind a "digital assets have no intrinsic value--equities are much safer" trope. But now the equities are zeros, while tokens remain call options with no expiry and no ability to get primed/zeroed in a restructuring. So perhaps tokens actually do provide more downside protection.

Source: TradingView, Bloomberg

Now, what does this have to do with the broad-based 20-100% rally we just saw last week? Well, everything, really. A quick math reminder:

- Up +100% after down -90% gets only gets you back to down -80%

- Up +50% after down -80% only gets you back to down -70%

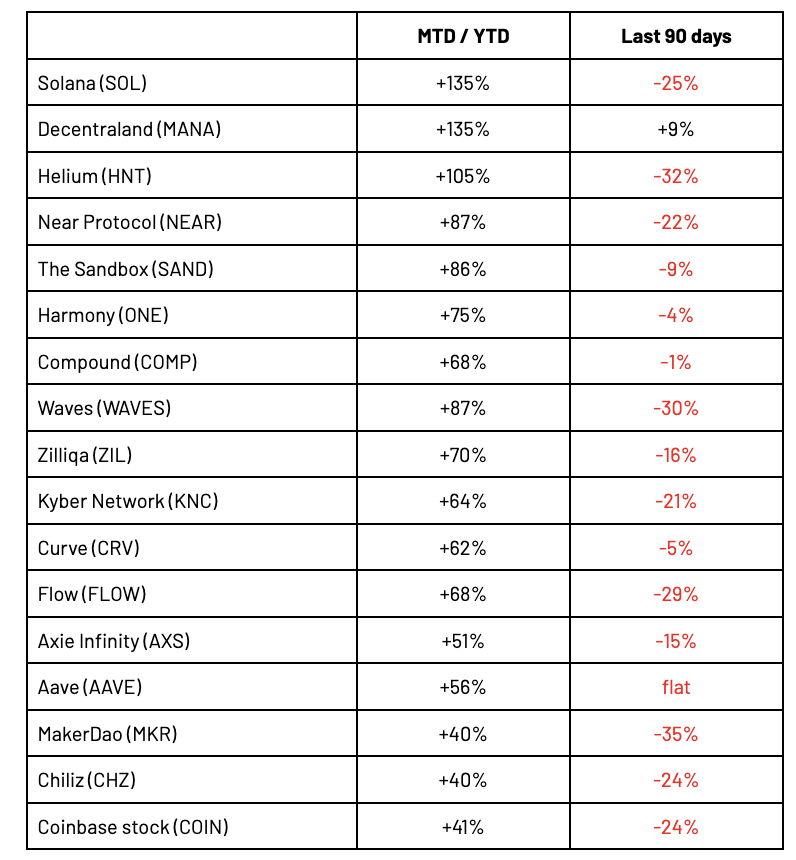

So if you ever believed that 2021 market caps were appropriate relative to the upside potential and that prices would one day return to these levels, many weeks/months like this past one must happen to get there. And while the absolute returns YTD look silly, it’s important to look a little bit further back to contextualize. Most of the biggest winners so far this month/year are actually still the biggest losers over the past 90 days. Why do the past 90 days matter? Because FTX imploded in the first week of November, killing what looked to be a promising recovery in digital assets at the time. Last week’s positive price action and “rip your face off rally” really just feels like a retracement of the post-FTX move (and the significant year-end window dressing selling).

For context, BTC and ETH are now up 9% and 19%, respectively, over the last 90 days (from pre-FTX levels). Both are up a very respectable +27% and +31% YTD but are massively underperforming some of the lower-quality tokens that are up +50-150% YTD. This is equivalent to a corporate bond rally, when the CCC-rated names rally harder and faster than the BB-rated names simply because they have higher betas and more room to run from lower levels. A few examples:

- BTC: +27% MTD / +9% last 90 days

- ETH: +31% MTD / +19% last 90 days

Source: Messari

It remains to be seen whether this rally is sustainable. We’ve been calling the bottom since mid-December, but admittedly only had a few tangible thoughts regarding what would first take the market higher or when it would happen. Some of the gains thus far are from short-covering, and some are due to actual news and announcements (i.e. LDO +106% on liquid staking, AVAX +56% on partnership with AWS). But most seem to be based on a broader risk rally that extends far beyond digital assets.

If this rally does have legs, some investors will inevitably stay sidelined far too long because they mentally cannot get past buying an asset after it already went up 50%-100%. It’s important to have a price target and not just look at path function right now. Expecting 5-10x returns is not unreasonable, and helps prevent selling too early at the first sign of strength. Looking beyond just the last two weeks also helps prevent shorting into this strength expecting an immediate fade. But that’s what makes markets. There is now a clear and significant disconnect regarding how market participants view this rally (often based on preconceived biases). Whereas we see pushes to reclaim pre-FTX price levels, others see unsustainably high double/low triple-digit returns in just two weeks that demand a retracement.

Meanwhile, if there was ever a doubt about the efficacy of blockchain itself, a 3-day weekend with banks and brokerages closed serves as a good reminder.

The World Computer The Trust Machine:

An ELI5 of the Poorly Understood New Vision For Ethereum

Written by Arca VP of Research: Nick Hotz, CFA

Sometimes technology moves so fast that it's hard to keep up with the pace of innovation. Sometimes technology overpromises, with rapid adoption making even evangelists' most lofty forecasts seem possible. And sometimes, technology pivots as certain goals appear unachievable with deeper research or when better ideas prevail.

In its short history, Ethereum has experienced all three.

In his original 2014 white paper, Vitalik Buterin described Ethereum as a "protocol for building decentralized applications." This vision has largely been realized as Ethereum now houses many of the applications he initially imagined: decentralized autonomous organizations (DAOs), decentralized file storage, decentralized finance (DeFi), and decentralized identity systems. In addition, The Merge finally implemented early hopes about a shift to a proof of stake consensus mechanism in 2022. Despite increasing competition in the blockchain infrastructure space, the Ethereum Virtual Machine (EVM) remains the de-facto standard for developers, and Ethereum is the hub for users and investors.

All this success, however, has bred a new set of problems. In 2017, as usage fees for the first time rose beyond negligible amounts, Buterin (in)famously quipped, "The Internet of Money should not cost 5 cents per transaction." In 2021, that statement appeared all the more out of touch with reality as costs to perform simple token swaps regularly reached $20—and often higher. As a result, other blockchains that offered the promised low transaction fees but more questionable decentralization quickly sprung up to take market share.

As its reputation as “the rich man's blockchain" grew, Ethereum's inability to quickly ship its scalability plans worsened matters. Ongoing research revealed fundamental flaws in its original intentions and strict improvements to its former roadmap. The coincidence of these increasingly tugged at the wheel of the Titanic that is Ethereum’s research efforts, encouraging a pivot away from its iceberg-ridden course.

Ethereum: The World Computer

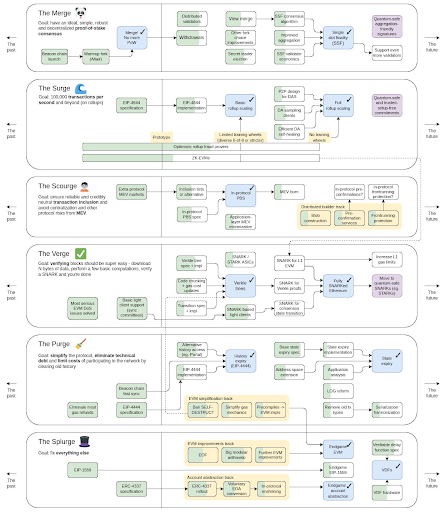

Buterin originally envisioned Ethereum to be a "world computer." Its long-awaited upgrade, Serenity, a.k.a. Ethereum 2.0, was devoted to making sure applications were widely accessible to anyone, anywhere, and could be built on Ethereum at infinite scale with low environmental impact. The key pillars of Ethereum 2.0 were:

Proof of stake: Using staked ether tokens rather than miners for "skin in the game" to ensure no one could cheat on the Ethereum blockchain. It is much more economically efficient (less token inflation needed) and environmentally efficient (no need for huge electricity expenditures to secure the chain), and is the only major component of the Serenity roadmap in place today.

Shard chains: Splitting Ethereum into many separate chains (1,024 planned!) to massively increase speed and reduce fees. However, shard chains also fragment Ethereum's security because each chain needs its own set of staked ether to secure it. This is in contrast to the current proof of stake Ethereum where all staked ether contributes to securing all transactions. Sharding effectively reduces Ethereum's decentralization and makes it more susceptible to attack. Sharding also makes it more difficult for the individual chains to "talk” to each other, which can worsen the user experience.

eWASM (Ethereum Web Assembly): Allowing Ethereum to support several different coding languages, not just Solidity. This would massively increase the potential developer base of Ethereum since aspiring developers would not be required to learn the previously unpopular Solidity language. However, this upgrade would make fundamental changes to Ethereum that could break compatibility with current applications, potentially leading to a very difficult and fraught development process.

With the issues of this roadmap in mind, the pivot in developers’ mindsets was first exemplified in Vitalik's late 2020 post, "A rollup-centric Ethereum roadmap," and further clarified in a late 2021 diagram depicting the various research efforts underway. Finally, an updated roadmap posted in late November brings us to today. The new roadmap is a fundamental change from Ethereum's original vision of a world computer. It has not been well articulated outside researcher/developer circles.

The New Vision For Ethereum

Ethereum's new path has several changes from the old model that acknowledge and actively integrate the most cutting-edge blockchain and cryptography research. The crux of the shift is the acknowledgment that it's difficult for individual blockchains to properly do all of the things Ethereum was attempting to do. The new vision slowly abandons Ethereum's role as a platform for applications in favor of becoming a sort of settlement layer for other blockchains. It plays to Ethereum's strengths as far and away the most decentralized and secure smart contract platform blockchain. It also outsources its weak points (speed, user costs) in a way that still allows users to benefit from Ethereum's security and the ease of running a node to check that everything happening on the blockchain is legitimate.

Let's dive in. (Don't be scared!)

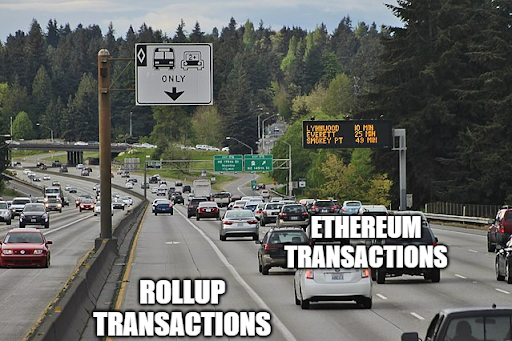

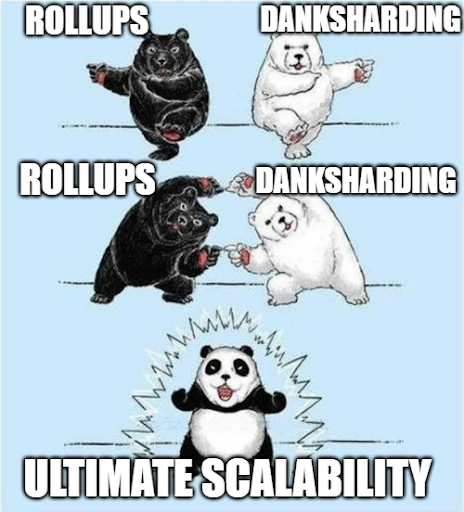

Ethereum will host fewer transactions; Layer 2 rollups will host more. Rollups are separate blockchains that are optimized to run really fast. Unlike other blockchains that typically trade off security and decentralization to run faster, rollups can do this without tradeoffs. This is because they prove all transactions to Ethereum. So if you trust the correctness of Ethereum, in general, you can trust the rollups, too. Rollups also bundle and compress transactions, meaning the total computational power it takes to process them is much lower than if Ethereum itself had to do it all. Rollups can even stack on top of one another, with a Layer 3 rollup bundling transactions to send to the Layer 2, which then puts together many Layer 3 bundles to ship back to Ethereum. The big concern with rollups is that these bundles require massive data space on Ethereum. This is an issue because the more data Ethereum processes, the harder it is to run a node, which worsens decentralization.

Danksharding replaces sharding. Sharding was the original way to solve this data problem. By splitting up Ethereum into many chains, people checking the legitimacy of some transactions would only need to check one shard, which represents a small portion of all the data Ethereum processes. Sharded blockchains are almost like separate chains completely. As previously mentioned, while they would have allowed Ethereum to process way more transactions at a lower cost, they also significantly reduce security.

In just the last year, researchers conceived a much more elegant solution—danksharding—that would still allow massive scalability benefits while still guaranteeing the full security provided by all Ethereum stakers to every transaction. The one catch: the extra capacity is only offered to users of Layer 2 rollups, not to users of Ethereum itself.

Danksharding gives rollups their own dedicated space in each Ethereum block that regular Ethereum applications can't use. Like using an HOV lane in heavy traffic, this dedicated space means that rollups can run much more efficiently (cheaply) than regular applications. And because Ethereum lets nodes delete their memory of rollup data after a month or so, it doesn't make Ethereum nodes harder to run, meaning Ethereum maintains its strong decentralization.

Because danksharding will offer rollups a lot more capacity (think: 1000x), and rollups themselves are already able to securely run much faster than Ethereum, their combination will mean dramatically lower costs and faster transaction speeds to users.

User fees on Ethereum are up only. On the other hand, a lack of focus on scaling Ethereum itself and an increased emphasis on subsidizing costs for Layer 2 blockchains mean that the cost of using Ethereum directly isn't coming down any time soon. Since other blockchains will be able to bundle thousands of transactions at a time to post back to Ethereum, they will be able to justify paying much higher fees than the typical Ethereum user. Further, as Ethereum increasingly solely verifies transactions that occur on other blockchains, regular users will continue to be priced out and forced to migrate to Layer 2s.

Solidity and the EVM are good enough. While Serenity/Ethereum 2.0 intended a move away from the EVM and its compatible Solidity language, this is no longer top of mind for developers. This isn't necessarily because researchers now suddenly believe the EVM is the pinnacle of blockchain developer and user experience. Instead, it has achieved such a strong network effect that research has shown it can do the things developers have in mind to improve the chain. Additionally, there are many more important components of the roadmap on which to focus.

Don't doubt the power of network effects. Well after the invention of the QWERTY keyboard in the 1870s, August Dvorak invented a keyboard that placed the most used characters close to the center for optimal typing efficiency. The fact that I'm not typing this from a Dvorak is a testament to the fact that the best tech doesn't always win. EVM and Solidity are a QWERTY keyboard—good enough to get the job done and have the network effects of adoption to back it up. (Hat tip to Bankless for the analogy.)

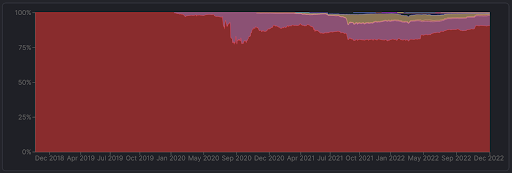

Code from Ethereum languages Solidity (red) and Vyper (pink) store 98% of all value on blockchains.

Source: DeFiLlama

Censorship resistance is a top priority. While I won't get into the messy details here, the key point is that without changes, Ethereum's neutrality as a platform will be threatened as it continues to grow. Most ETH stakers use entities like Coinbase, Kraken, and Lido to do so, which creates centralization risk. If a large entity like the U.S. government can influence these entities—and by proxy, a large swath of these stakers—it can reduce Ethereum's ability to treat all transactions the same as long as their senders pay the proper fees. Fortunately, brilliant researchers have been working on this for years and have a good plan to ensure censorship is not tolerated, as outlined in The Scourge.

Now, some of you may be thinking, "Who cares if Ethereum censors transactions? We already need to KYC with banks anyways, and I'd rather see those North Korean hackers not be able to use Tornado Cash!" This sentiment certainly resonates with me. However, for every illicit user of blockchains, there is another one that is forced to use blockchains to defend their rights:

People rely on these blockchains to be credibly neutral and resist manipulation by their respective governments. Blockchains can only provide these benefits if they can be resistant to every centralized actor's influence, regardless of the goodness of their intentions. This insight is why Ethereum is prioritizing credible neutrality so highly.

Zero-knowledge (ZK) proofs permeate every aspect. ZK cryptography is about proving a select piece of information to someone or something else without revealing any other information. This allows blockchains to compress thousands of transactions together and prove their validity to Ethereum. As long as the other blockchain is running legitimately, it can submit a ZK proof to Ethereum demonstrating that a bundle of transactions that occurred on it are legitimate. A blockchain that does this is called a Zero Knowledge Rollup (zkRollup). zkRollups also have the major perk of seamlessly interacting with one another as easily as applications on Ethereum do today. The advent of Layer 2 zkEVMs from the teams at Polygon, Scroll, and zkSync read code in the same way Ethereum does. They will ensure easy porting from Ethereum to these rollups.

Research in ZK cryptography contributed heavily to the current plans for danksharding and censorship resistance. ZK technology can also immunize blockchains from the risks of potential hacks by future quantum computers. Farther down the road, Ethereum itself can even become a zkRollup (to itself—wild, I know), facilitating low-cost transactions for users at nearly infinite scale. This technology made massive strides in 2023 and will continue to be a hugely important idea in the crypto space going forward.

Ethereum: The Trust Machine

While still encompassing Vitalik's original vision as a platform for applications, in the future, Ethereum will increasingly pivot away from directly hosting users. This doesn't mean the scope of Ethereum's potential impact has shrunk. Rather, the new vision recognizes the need for multiple protocols to perform different functions (much like the architecture of the Internet today), in which Ethereum plays a fundamental but not all-encompassing role.

Instead, it will become a global settlement layer—a trust machine that other blockchains use to ensure legitimate transactions are broadcasted to the world and illegitimate ones are impossible. By combining rollups, danksharding, and zero-knowledge cryptography, Ethereum will be able to provide these services at nearly infinite scale, while maintaining high decentralization and making it easy for individuals to verify transactions. In addition, an emphasis on neutrality means end users can be confident that their transactions have not been censored or influenced in any way. The changed roadmap is a recognition of the role Ethereum is best equipped to serve in a potential blockchain future—a global source of truth and legitimacy in a space that sometimes could use a lot more of both.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari