Relative Strength

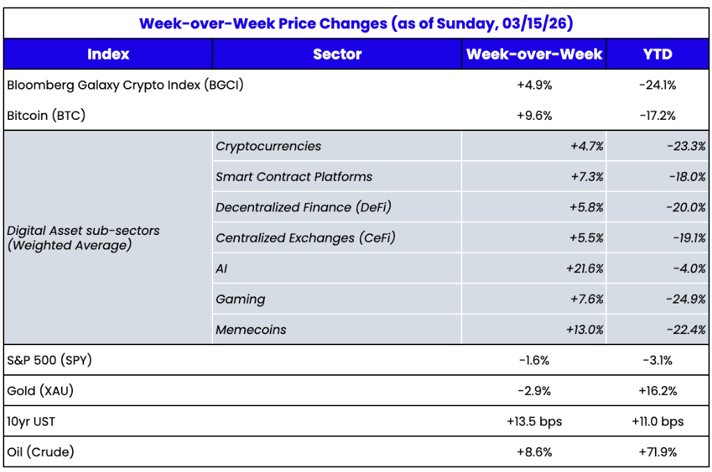

It’s been a long time since digital assets broadly outperformed any markets, let alone gold, equities, and Treasuries in the same week. But last week, we saw a little bit of everything from digital assets, for example:

These are modest moves higher relative to the volatility we’ve seen in crypto historically, and equities YTD, but still a welcome sign. We’d like to see a little more dispersion and volume within digital assets before we deem this a healthy recovery, but it’s definitely a good start.

By now, we all know that crypto and blockchain adoption are happening at a record pace, but prices of most digital assets have not followed suit. The optimistic, hopeful rationale is that crypto prices lag news. The more pessimistic reason is that most of this adoption doesn’t actually benefit the majority of tokens. This is perhaps a controversial opinion, but in my opinion, one of the biggest reasons for the massive disconnect between crypto prices and crypto adoption is that 4 of the top 5 assets (by market cap) are largely uninvestable. Now, that doesn’t mean that prices can’t go higher, and that you can’t trade these assets from the long side. A rising tide lifts all boats, and these 4 assets are so large and well-known that they could go higher at some point. But in my opinion, they are uninvestable because every single thesis for owning these 4 assets has been debunked over the past few years. And if you can’t underwrite a consistent thesis, then it’s difficult to invest in these with any confidence for long periods of time. Said another way, it’s difficult, if not impossible, for these assets to show consistent strength because the assets are only loosely tied (at best) to the success of the underlying companies/projects. So all we’re left with is short-term trades on sentiment. Let’s dive under the hood:

#1 Bitcoin (BTC):

While I believe BTC may go higher over time, it has failed to hold on to ANY of the narratives it was built upon.

Further, the quantum fear is not going away (even though it's a fairly easy technical fix, it's a much harder governance fix).

Conversely, I think Bitcoin has never been less risky as an investment (since we know it isn’t going to be illegal, and it is being adopted by Washington and Wall Street). But underwriting it as an investment has never been harder. While that may sound contradictory, it is how most professional investors think. It’s not enough for an asset to go higher; you need to understand WHY it will go higher to justify a reason for owning it. And all of the reasons and rationales from the past 17 years have largely failed. Bitcoin is still entirely narrative/faith-based, and while that can change on a dime, it’s very difficult to build an investment foundation on it.

#2 Ethereum (ETH) and #4 Solana (SOL):

Ethereum and Solana have largely been deemed the “successful” Layer-1 blockchains, but neither has had meaningful traction relative to the size of the financial industry, and neither has sound investment theses. Another way to say this is that Ethereum and Solana’s success to date are largely irrelevant to the future of blockchain, since 99% of the world’s assets (stocks, bonds, and real estate) are not on-chain yet. Any lead based on $300 bn of stablecoins and endless memecoins is not super relevant compared to where the on-chain world is headed. Further:

For the record, I'm bullish on both Solana and Ethereum's prospects for further growth (relative to most other L1s), but I just don't think their tokens capture much value from that growth. If you cannot confidently say that “ETH and SOL will do well as Ethereum and Solana grow”, then the investment thesis is largely busted.

#3 Ripple (XRP):

Ripple is no stranger to token controversies, but even the least educated crypto investors are now realizing that this token does nothing and has almost no ties to Ripple Labs.

So while the recent strength is encouraging, crypto will likely remain broken until we break the reliance on these 4 assets. The entire industry was built on 4 assets that are either impossible to underwrite as investments or that require insane growth to justify lofty valuations. This, of course, is why all exchanges and brokers cater only to fast-money traders, macro funds, and CTAs, rather than targeting real fundamental investors, even though fundamental investors make up the majority of the investor world. This strategy is good for extracting trading profits, but bad for building sustainable wealth for long-term investors.

Can this change? I hope so. It's very hard for an industry to grow when the top assets are the least interesting, but not impossible. It would require a massive rotation, but that is exactly what we're seeing in equities right now - a rotation out of Mag 7, private credit, and tech and into healthcare, energy, etc.

In my opinion, there are a LOT of good token and equity investments right now that accrue value via the adoption of crypto and blockchain. Aligning your investments with the actual growth areas may work over time. As mentioned many times previously, almost all of the growth and adoption of crypto and blockchain is happening in 3 financial areas:

But little to none of that growth accrues value to the 4 tokens mentioned above. If this industry pivots away from BTC, ETH, SOL, XRP, and memecoins and into the stocks and equity-like tokens that fuel the growth of DeFi, payments, and RWAs, then price will likely start matching adoption more closely.

The Strategy (MSTR) End Game

Strategy (MSTR) continues to find ways to buy more Bitcoin. I’m on record recently saying that I think the Strategy story is just boring now, as they may not be able to acquire meaningful amounts of Bitcoin going forward since DATs are dying, but they also won’t be forced sellers of Bitcoin anytime soon. But it appears that I, like many others, have underestimated Saylor and the capital markets chicanery he is capable of.

Most recently, with mNAV compressing, Saylor has turned to its preferred instrument (called STRC) to continuously sell into the open market via the ATM issuance. There was a good write-up this week from Crypto Narratives titled “Understanding STRC: How Strategy Turns…” that walks through the mechanics of Strategy’s (MSTR) capital stack and the recently issued STRC preferred securities. The article does a nice job laying out how Strategy has effectively built a multi-layered financing structure around its Bitcoin treasury using common equity, convertibles, preferred securities, and other instruments to continuously fund BTC purchases.

The key argument in the piece is that Strategy’s balance sheet appears relatively safe when viewed through traditional leverage metrics, because the company’s Bitcoin holdings significantly exceed its debt obligations. In other words, if you simply compare assets to liabilities, the company appears well capitalized. Add in the fact that the debt has no covenants, eliminating any risk of BTC liquidation, and the conclusion is that creditors and preferred holders should feel comfortable.

But that framing misses the most important credit metric: interest coverage.

Leverage ratios matter if the assumption is that assets will eventually be sold to repay debt. But the entire Strategy thesis rests on never selling Bitcoin. If BTC is never sold, then the relevant question isn’t leverage — it’s cash flow.

Interest coverage is simply EBIT / Interest Expense. Strategy generates essentially $0 in EBIT, indicating it has no interest coverage. Meanwhile, the company now faces more than $1 billion per year in interest and preferred dividend obligations, and that number continues to grow as the capital stack expands, especially if MSTR now relies more on selling preferred stock to fund its growth.

Which means that over the long run, Strategy only has a handful of possible end states:

The problem is that there are four stakeholder groups directly tied to Saylor and Strategy, and all four stakeholders believe they are safe, but it is impossible for all four to do well without sacrificing one or more of the others.

Individually, each of these groups can be right for a long time. But collectively, they cannot all be right forever. If Saylor never sells Bitcoin, then the debt and preferreds will eventually default. If Saylor continues to sell more shares to fund the interest and dividends, then MSTR shares will be diluted. If Saylor sells the Bitcoin to fund its capital structure, then BTC will suffer.

You can’t pay the bills (interest/dividend payments) without cash flow, and that cash flow has to come from somewhere.

At some point, the system has to choose which stakeholder group it prioritizes. And that’s the real risk to this new instrument.