Guest Edition — Written by Christopher MacPherson, Research Analyst at Arca

In the early days, they ignored crypto—few understood it, and no one even cared about Bitcoin. Then they laughed at it, with comments like Jamie Dimon’s “Bitcoin is a pet rock.” Then they fought it—through the Gensler regime, Elizabeth Warren’s “Anti-Crypto Army,” and Operation Chokepoint 2.0. The last part of that saying is “then you win.” But right now, it doesn’t feel like crypto is winning.

The once-irrationally ambitious, ‘believe in something’ crypto-native crowd is now capitulating to pessimism and short-termism—just as the outside world is finally beginning to embrace crypto. Even some of the most dedicated analysts and traders I speak with are starting to question the long-term vision that crypto will continue to grow and be a force for good in the world. Among that group, the prevailing view increasingly sounds like:

“Other than Bitcoin and stablecoins, crypto is not working and never will work.”

The first part of that statement is correct. But never work? That is the epitome of the “what can go wrong, will go wrong” doomer ideology infecting so many young people around the world today. I’m not going to spin the latest drawdown as an amazing chapter in crypto’s history, but I do sincerely believe this is a constructive and necessary period of time for crypto before its next expansion.

Misinformation and misunderstandings of crypto’s basic core function are still the norm in the world rather than the exception. I’ve spent every day over several years digging deeper into this market and individual projects (more than any human should). I do it partially because markets fascinate me, but primarily so I can understand what the truth really is, and what it is not, in our markets. The truth is that crypto has a token problem. The problem can only be fixed by experts who subscribe to the “What could go right?” point of view and are willing to lead from the front.

When you study the history of markets, one of the most important concepts is that markets are self-correcting in nature. Crypto’s current bear market is not a signal of the end. It is self-correction happening in real-time. Although most tokens are dying an ugly (but deserved) death, there is more to it than what meets the eye.

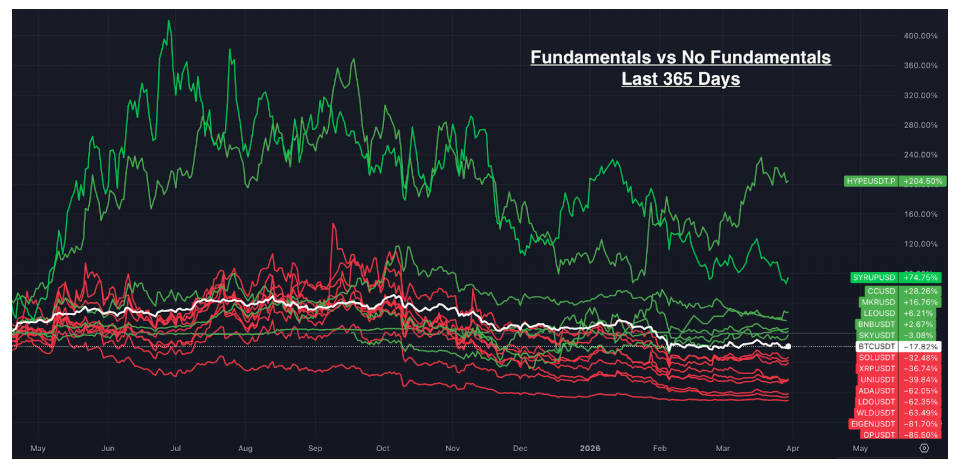

The above chart should make things very clear. Crypto used to reward hype, contrived definitions of value, and the belief that the value of the tech is the value of the asset.

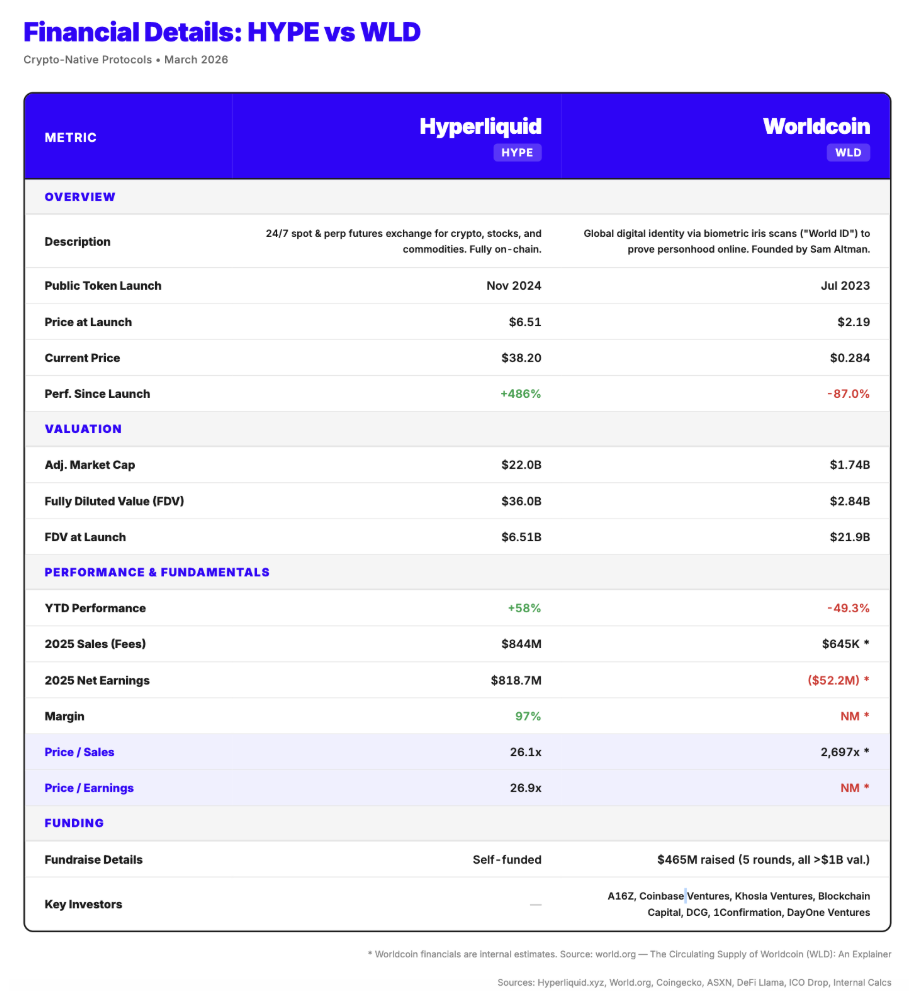

Okay, so one project represents a grassroots crypto exchange that is crushing it (+58% YTD and +486% since launch), and the other project is Sam Altman’s dystopian, eyeball-scanning orb project that is seemingly failing (-49.3% YTD and -87% since launch). Sure, it’s odd that a Sam Altman endeavor with $465M in private funding could be failing this badly, but so what? Some ideas win, and some lose.

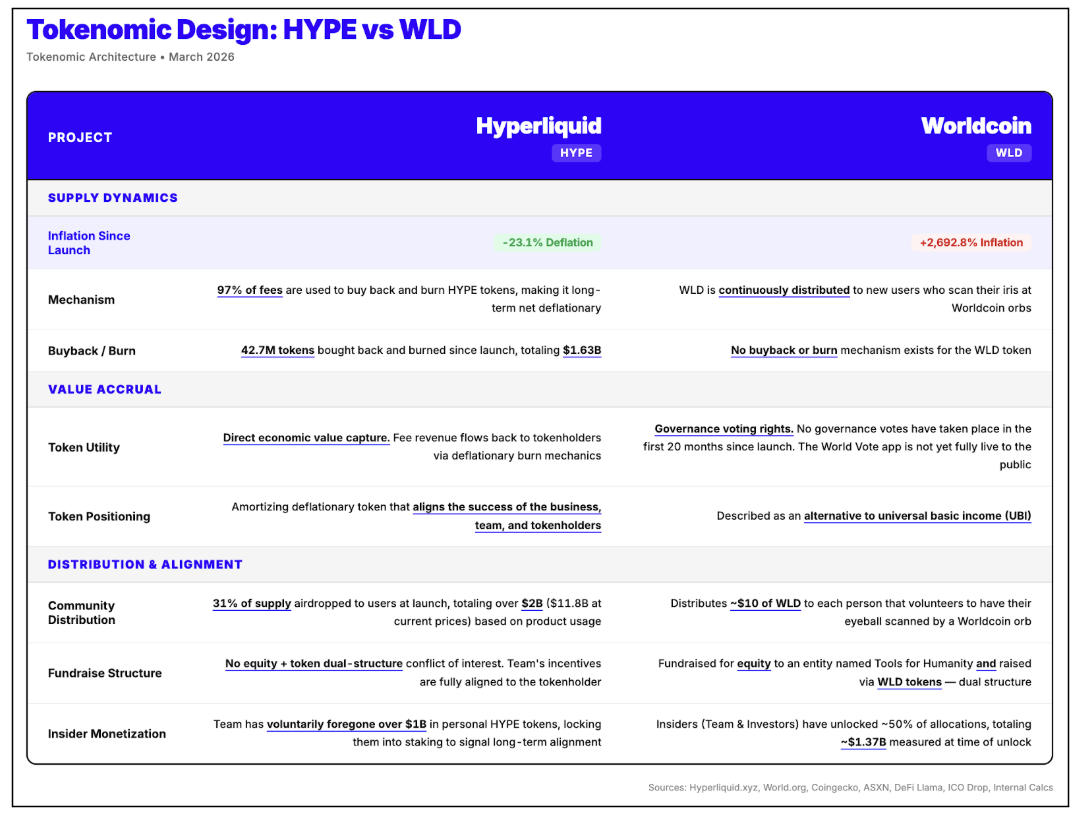

The truth of the matter is, Worldcoin was never going to work. Not because there is a lack of naive humans on earth that are willing to give up their unique iris pattern to Sam Altman for a quick ten bucks (there are plenty). Worldcoin was never going to work because its economic design around the token made it so. Every project/token that is horribly failing has the exact same issue: avalanches of supply (diluting token holders), with no mechanisms to fight back against that dilution. Crypto denied the existence of supply and demand, thought it could redefine Econ 101 principles of markets, and is now taking its medicine.

It always comes back to tokenomics.

If it’s not clear yet, consider the incentives from a Worldcoin (WLD) participant’s perspective:

Hyperliquid is the opposite because it operates like a business, and that business aligns all value to the token. You grow the business by growing the value the product provides to the world. If you believe that the value of the product will grow over time, the token is designed such that its value is correlated to that growth. That is a straightforward fundamental model that institutional investors can get behind. It sounds simple because it is—when you see things through the lens of “what could go right?”

Ignore the doomers. Lead from the front.