Another Week of the Same Macro Concerns and Crypto Apathy

I was on vacation for the latter half of last week. Historically, that’s not noteworthy since my vacations just mean that I work from a different location. When you invest in a 24/7 liquid market, there really is no difference between weekdays and weekends, vacation days and work days. In fact, I typically consume even more market knowledge when I’m traveling than when I’m in meetings all day.

Last week I took a real vacation. There was almost nothing notable worth digesting. Private credit has a liquidity issue (not a credit issue), and simply reading more about redemptions and gates doesn’t change that. The Iran situation is not over, and no information from President Trump or the media is credible at this point. My price alerts didn’t go off. My internal Arca communications were quiet. While equities jumped at least partially due to quarter-end rebalancing, and oil prices and gold marched higher amid continued war headlines, the majority of digital asset prices barely budged.

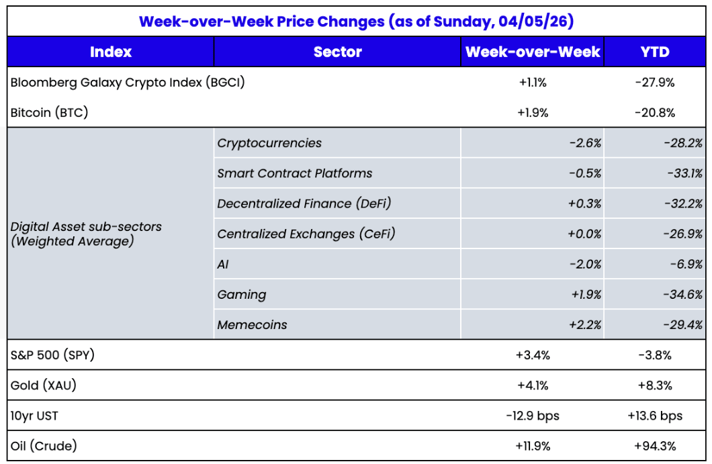

Bitcoin (BTC), an asset that almost never has material idiosyncratic news (unless you consider Saylor’s buys “material news”), completely shrugged off further quantum fears. Researchers from Google Quantum AI, Stanford, UC Berkeley, and the Ethereum Foundation published a paper called “Securing Elliptic Curve Cryptocurrencies against Quantum Vulnerabilities: Resource Estimates and Mitigations” on Monday, demonstrating that it is easier for quantum computers to crack cryptography than previously thought, should they eventually be successfully built. Ho hum… BTC was unchanged on the day and +2% week-over-week (for those who want the bull case for Bitcoin, Galaxy Digital wrote a nice piece noting Bitcoin core developer progress on this matter).

Since the war began on February 28th, oil has obviously outperformed everything, but BTC has marginally outperformed both gold and the Nasdaq.

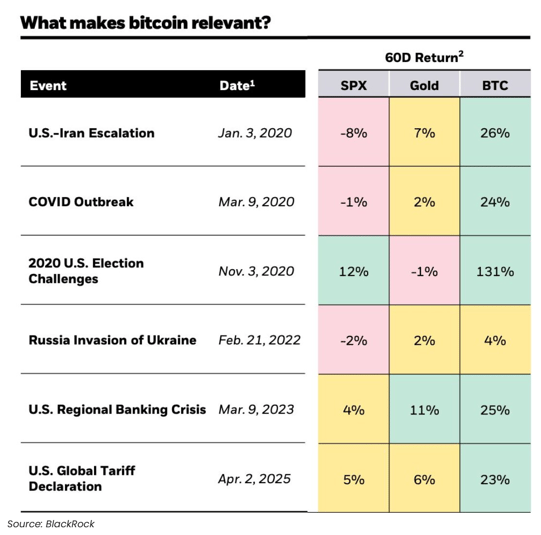

BlackRock recently noted that during the most destabilizing events of the last 5 years, including past U.S.-Iran escalations, COVID, the American regional banking crisis, and global tariffs, Bitcoin has largely shown behavior that neither the S&P 500 nor gold has replicated.

The pattern used to be clear: in moments of systemic stress, Bitcoin may initially face pressure, but then it recovers, and often goes beyond. That has not been the case this time around, at least thus far.

Meanwhile, the rest of the digital assets market (sans Bitcoin) remains just as lifeless. As we’ve been pointing out for years (and again last week at Arca’s FO256 conference), there is a major disconnect between the extremely positive news flow on blockchain adoption and the prices of blockchain-based assets. A big reason for this is that this industry (exchanges, ETF providers, market makers) is built around the trading of Bitcoin, and continues to force-feed this narrative, even though Bitcoin itself has literally nothing to do with the 3 areas where blockchain is growing the fastest:

If you want to express a “long blockchain growth” theme, and all you own is BTC, that’s the equivalent of trying to be “long gambling” by investing in the 3-card monte guy in Times Square.

That said, there really isn’t an easy answer to being “long blockchain growth.” Mike Ippolito at Blockworks summarized this in a recent tweet thread, highlighting how big a problem token investing is right now. In conclusion:

The whole thread is good, but this last part is most important.

Arca, for example, has one of the longest-running liquid token funds, and we think less than 20 tokens are even part of the investable universe, if that. Very few of the token issuers, exchanges, or VCs ever ask what it is a liquid fund wants to see to make a token investable. They don’t seem to care. The goal seems to be only to issue the token, not to make it valuable. And unfortunately, there are no investment banks or independent market makers in this industry to keep them honest, so the same pattern keeps repeating.

The exchanges are the worst culprits. An “everything exchange” doesn’t work when you kill all your customers with terrible investment products and try to sell the whole industry as one giant “macro trade.”

What do we mean by “investable”?

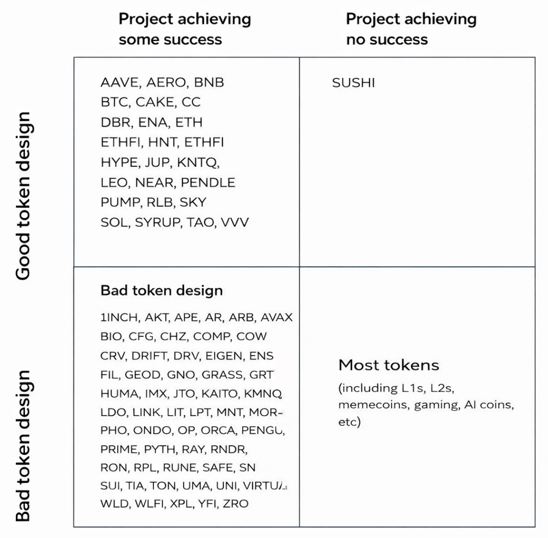

Let’s think of the token landscape like a quadrant.

The best way to move forward is to focus on the 10-20 tokens that are investable, ignore the rest, and require tokens to be built properly before giving them liquidity and visibility.

Until exchanges, market makers, and other powerful gatekeepers agree on some level of token standards, expect more of the same apathetic (or down-only) price action.