What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

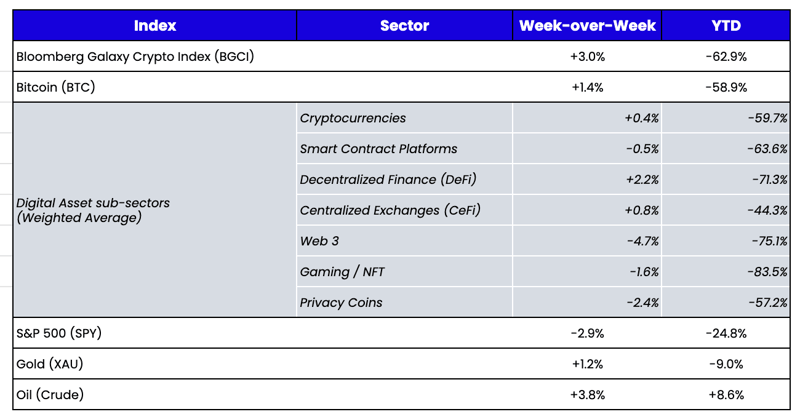

Week-over-Week Price Changes (as of Sunday, 10/02/22)

Source: TradingView, CNBC, Bloomberg, Messari

When Markets Begin to Break

Three straight weeks of ugly price action in equities helped the stock market reach new 2022 lows, with the S&P 500 closing out its worst month since March 2020. Meanwhile, U.S. Treasuries were volatile, with the 10-year exploding 30 bps higher and hitting 4.0% before rallying back to 3.80% later in the week after an unexpected U.K. government bond-buying program. One might have expected this backdrop to have sent digital assets sharply lower, but instead, the “decoupling” that we’ve been pointing out for months intensified.

Even Bitcoin, the only digital asset truly tied to macro, began to separate from the pack.

While it's too early to tell if this is simply seller exhaustion or a new bullish narrative, it does not seem entirely coincidental that digital assets have found their footing—relatively—in recent weeks. A strong dollar is generally bad for risk assets, but a dollar that is too strong indicates real financial stress and reinforces the narrative of why digital assets exist in the first place. At this point, you’d have to be naive to believe that digital assets give you long-term freedom from the current financial system, given regulation is coming from all corners of the world. That said, while not entirely separate, it is different, and different is good when we begin to head down all-too-familiar paths of interconnected failure and bailouts. European banks are starting to show cracks in the armor, and U.K. pension funds needed a bailout after their low-rate levered strategies backfired.

Liability Driven Investment (LDI) almost took U.K. pension funds down; it is a fancy term for “buying levered positions in Gilts” to increase duration to offset the fact that their liabilities increase when rates fall. As gilts sold off, these pension funds got margin calls. When the cost of capital rises sharply, over-leveraged entities get exposed—even those that are supposed to be boring and safe. Pensions added leverage to increase returns, and years later required government intervention—a story as old as time.

And when you hear the words “government intervention,” some small part of the investing world seeks investments outside of this chokehold. Right now, it doesn’t take much incremental buying power to move the needle for digital asset prices.

A Guide to Investing in the Blockspace Cycle

Nick Hotz, CFA - Vice President, Research

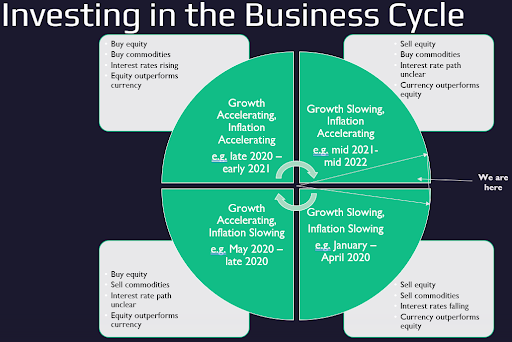

As a former global macro analyst, understanding and following cycles of growth and inflation in the economy were key to understanding what was driving asset markets and forecasting what might be next. The business cycle involves accelerations and decelerations in growth and inflation, typically occurring in a natural progression in capitalist economies due to Federal Reserve policy actions and the credit cycle. While shocks to demand and supply can alter its path, we see this cycle take place across geographies and time periods, with predictable implications for asset performance at each stage.

Source: Arca Internal Research

While numerous researchers have studied the business cycle in real-world economies, none have applied this analysis to the new digital economies enabled by blockchains. While on-chain credit is still in its earliest stages and credible monetary policy was only recently enabled on Ethereum by the merge and EIP-1559 fee burning, blockchains still see a natural cycle driven by the supply of and demand for the resource they provide: blockspace.

Blockspace: Web 3's Gold Rush

Blockspace is space on the blockchain that can be used to run code or store data. Ethereum, for example, provides 1MB per block of blockspace, with a fee marketplace to determine which users get included in the block and a further tip fee to determine location within the block. Blockspace is valuable because it lets you access the immutable, permissionless ledger that is a blockchain at a specific time. The value of blockspace varies across time and for different actors. Accessing Ethereum during a popular NFT mint may have warranted a hefty fee in mid-2021, while using Solana during a popular mint today isn't even noticeable. An arbitrageur may place a high value on being at the front of a block to execute a transaction, while the average DeFi user couldn't care less where they are placed.

Blockchain-based economies have cycles of supply and demand, just like traditional economies. Real-world economies consist of many persons and organizations transacting to obtain various goods and services, just like digital blockchain economies. Different forces can shock blockspace value, both on the supply-side (e.g., introductions of rollups, creating new L1s) or on the demand-side (e.g., DeFi summer, NFT mania). Last year when blockspace was really valuable, new producers (Layer 1s and Layer 2s) rushed in to provide more, but I suspect they may not be so eager as blockspace becomes less and less valuable.

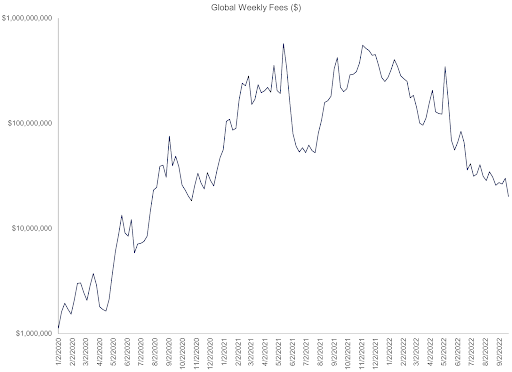

After close to a year since the global market cap highs, with prices of most digital assets sharply lower, demand for blockspace has collapsed. For example, 90-day average gas fees on Ethereum are down to 22 Gwei (~$0.70 for sending ETH) from a high of 128 Gwei in January 2022 ($10-20 to send ETH). This, in turn, has led to a 96% decline in total fees paid to Layer 1 blockchains since the November 2021 highs. While fees aren't the only thing that makes a Layer 1 token valuable, the scale of the drop is a sure sign that users are no longer very interested in paying to access blockspace.

Source: Arca Internal Research, Token Terminal

But while users certainly don't want to pay to use blockchains, actual usage doesn't look nearly as dire. Total active addresses using public blockchains have risen each of the last four weeks, from a peak drawdown of just -31% from the highs.

Source: Arca Internal Research, Artemis, Glassnode, Messari

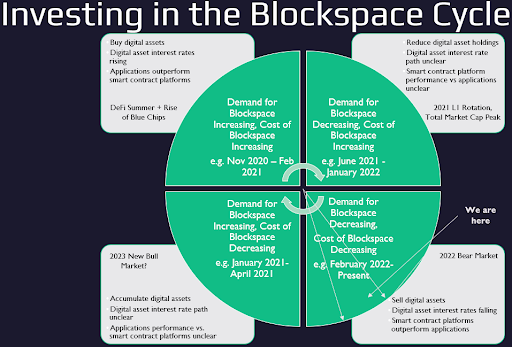

Initial signs of a bottoming in users without a corresponding pickup in fees are quite consistent with the business cycle, where growth rises first, only later followed by prices. But in this case, we can call this predictable pattern the Blockspace Cycle.

Investing in the Blockspace Cycle

Source: Arca Internal Research

For those looking at the parallels, the blockspace cycle is a lot like the business cycle. Both tend to (but don't always!) occur in a logical sequence of inflation following growth. User growth leads to higher interest rates and more speculative activity, increasing users' wealth and willingness to spend money. Eventually, a scarcity of new users and money due to high prices and a lack of innovative new products turns demand downwards, reduces borrower interest, and ultimately drags prices down. The cycle repeats as new products are built, or new liquidity is injected into the ecosystem from investors to draw in new users.

The business and blockspace cycles have major implications for asset allocation among the various asset classes available within the economy. During good times when fundamental growth and gas price inflation are rising, higher beta assets tend to outperform while Layer 1 currency tokens underperform. During these times, interest rates rise to reflect increased willingness to borrow, and asset prices in aggregate tend to rise. In the opposite environment, Layer 1 currencies tend to outperform along with low beta assets. Interest rates fall as borrowing demand dries up and asset prices generally fall.

A 2 Minute Walk Through the Last Blockspace Cycle

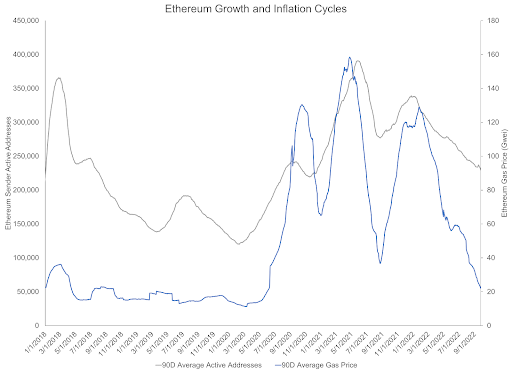

The end of the 2017 bull run brought an immediate drop in both usage and prices on Ethereum, which lasted through early 2020. While ETH itself fell 94% from peak to trough during this time, most ICO sale applications essentially went to zero or lost all liquidity between 2018 and 2019. The blockspace cycle began to shift in 2020 as DeFi summer caused active addresses to turn higher while gas fees lagged. As new gas-intensive applications (e.g., auto-compounding DeFi interest) gained adoption, gas fees soon followed usage higher.

Source: Arca Internal Research, Etherscan

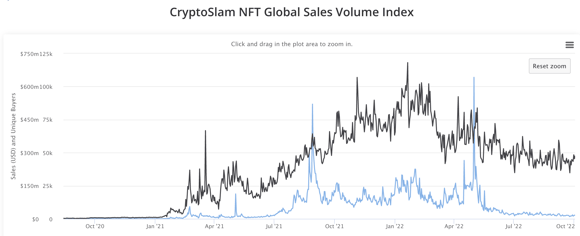

Shocks to either growth or inflation can impact the typical sequence of inflation following growth. For example, the initiation of the NFT mania on Ethereum represented a major shock to demand in early 2021, as existing users transitioned from using blockchains for DeFi transactions to even more gas-intensive NFT minting and trading.

Source: CryptoSlam

This resulted in gas prices shooting up relative to active addresses and peaking in May well before addresses peaked 2 months later. From there, gas fees collapsed 75% as demand dropped while new blockspace from Polygon PoS, Binance Smart Chain, and Solana increasingly came online to offset some of the new blockchain users. Finally, as 2022 began, both fundamentals started dropping in earnest, with falling prices and yields reducing mainstream interest.

While applications outperformed for significant periods in early 2021 and the second half of 2021, particularly during large upswings in fundamentals, the story of the 2022 bear market has been one of ETH dominance over application tokens. So the question remains: what happens once these fundamental trends and the blockspace cycle begin to turn?

It's Time to Bet on Thin Protocols and Fat Applications

Placeholder's Fat Protocol Thesis that commodities and smart contract platforms like Bitcoin and Ether would accrue the majority of the value within digital assets has long been a point of discussion at Arca, with both sides having reasonable arguments for and against. However, almost as important as knowing the future of value accrual in the space is understanding that the path we take there is not likely to be straight. Instead, we'll probably go through many waves of infrastructure building, followed by waves of applications enabled by that new technology.

The pendulum has swung from an environment in 2021 where blockspace was so scarce that users would regularly pay $50 or more to access quality blockspace on Ethereum quickly to one where demand is low enough that users can easily obtain cheap, secure blockspace. And increasingly, they will be able to use systems like Cosmos's Inter-Blockchain Communication (IBC) or Synapse's optimistic rollup chain to seamlessly and safely move liquidity and data cross-chain.

Such an environment has very different implications for asset allocation than the one from which we've come. As demand has come down in 2022, smart contract platform tokens like ETH, BNB, and ATOM have generally outperformed, with all but the most blue chip application tokens down 80%+ year-to-date. In addition, interest rates have fallen sharply; last year, many were propped up by token issuance, investor capital, and DeFi hand-waving.

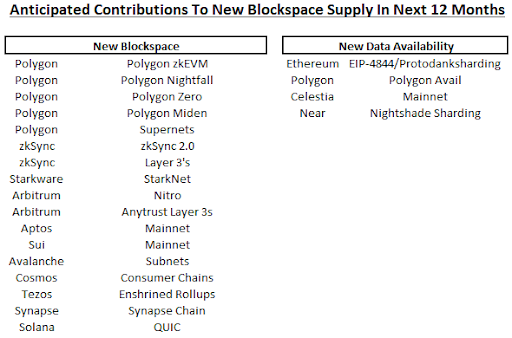

While demand for blockspace generally continues to languish, builders remain hard at work, particularly on infrastructure. 2021 showcased how valuable blockspace can be when buyers are interested, and teams across the space are trying to ensure they can capture as big of a piece of the pie as possible. Unlike a couple of years ago when rollups were still a pipe dream and a multichain future was uncertain, now there is an absolute ton of new, high-quality supply coming online in the next twelve months. Here is an incomplete list:

Source: Arca Internal Research

Even go-forward value accrual for Ethereum—the platform most likely to accrue significant usage fees—is a question mark. Over the past few years, the roadmap focused on improving ETH the asset; this has given way to one focused on scalability by improving the business model for Layer 2s at the expense of its own margins. Additionally, an onslaught of Layer 2s is coming online to compress transactions and reduce fees even further. Between the two, this should put a lower floor on how much users expect to pay on the most expensive chain.

The cementing of ETH as a medium of exchange for Layer 2s has also recently been called into question by Starkware, which plans to use its own token for gas fees on the upcoming StarkNet Layer 2. Outside of Ethereum, scaling solutions for many other ecosystems are coming into their own with an increased focus on decentralization and security. Finally, if gas fees on Ethereum and other premier blockchain ecosystems like Solana and Cosmos remain low, value accrual to many lower-tier tokens (many which pitch low fees as one of their main selling points), is even more questionable.

The impending environment will likely favor active investors focused on understanding the new wave of blockchain applications that will drive usage and economic profit. Meanwhile, persistently low fees will push investors to question the value propositions of many Layer 1 currency tokens. Further, with new infrastructure allowing for broader app experimentation, a greater focus on sustainability in the decentralized finance space, and potential for app-chains to dramatically improve application margins, the backdrop for the application space is brighter than it has been in a while.