What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

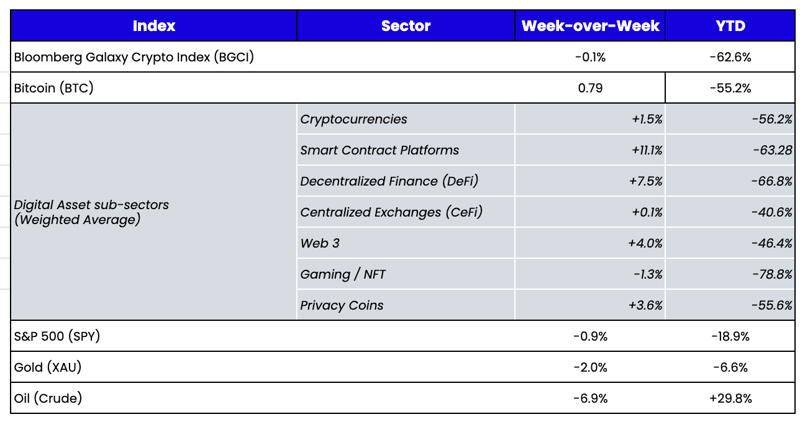

Week-over-Week Price Changes (as of Sunday, 07/17/22)

Source: TradingView, CNBC, Bloomberg, Messari

The Forced Selling Has Stopped, But the Bad Narratives Continue

Don’t look now, but there has been quite a resurgence in token prices since the “Three Arrows bottom.” Some tokens are now up over +100%, while most have gained north of +30%. We're not out of the woods, though—on average, digital assets are still down -42% over the past 90 days, even with this recent bounce. Still, it's encouraging to see that most of the leading price gainers are rising because they've had real idiosyncratic positive news or they are market leaders in their respective sub-sectors.

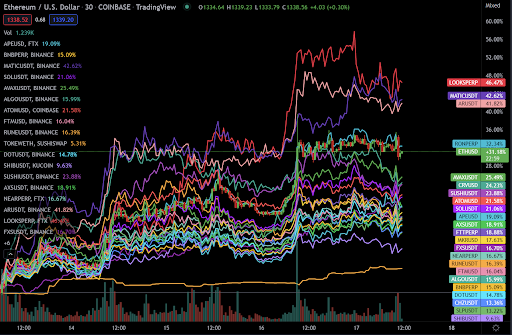

| Select performance since last week's CPI print dump |

Select performance since 3AC bottom |

|

|

Source: TradingView

One of the tokens missing from this recent rally is Bitcoin, which is now up only +12% over the past 30 days and still -48% over the past 90 days. Much of this underperformance can be attributed to forced selling since Bitcoin was, and still is, the most heavily used form of collateral for loans. But while Bitcoin is still a market leader in its respective sub-sector (currency), the Bitcoin narrative has taken some lumps recently.

- BTC is no longer acting defensively, as Bitcoin has lost market share relative to the field since the start of the digital asset selloff.

- BTC is not acting as an inflation hedge, as BTC has lost ground versus gold and the U.S. dollar.

- BTC is no longer the dominant blockchain regarding fees or transactions.

Now, before Bitcoin maxis start throwing disparaging crypto epithets my way, let me state in no uncertain terms that I love Bitcoin the asset. I believe Bitcoin is an asset everyone should own. I think it's a cheap call option on a very uncertain macro future. And I believe Bitcoin is an entirely different asset than every other digital asset and, therefore, should not even be traded by the same investors, let alone used as a comparison or benchmark. I love “Bitcoin the asset,” but I can’t stand “Bitcoin the industry.”

For example, recently, NYDIG—a company built entirely on the success of Bitcoin and no other digital asset—wrote the following in their (usually) wonderful weekly market recap:

“...investors may re-underwrite the asset class, likely with a renewed focus on bitcoin, partly because investors may have realized that many of the new projects and assets that sprung to life in the previous cycles did not live up to expectations and partly because they may have realized that, amongst the nascent asset class that is digital assets, bitcoin is the one with the best product-market fit. That is to say, the attributes most important to the asset class, its trustless, permissionless, and censorship-resistant nature, are best suited to a non-sovereign form of money rather than, say, a video game. Previous cycles have taught us that many of the recent cycle’s hot projects may end up falling by the wayside and never regain their former luster in the next cycle.”

That statement is the kind of propaganda we would have expected four years ago when there was very little data to back it up, but there are numerous public data sources that immediately refute such a claim. In the past two years alone, there have been plenty of success stories with massive product-market-fit:

- U.S. Dollar Stablecoins went from non-existent with $0 of AUM to over $150 billion in AUM

- DeFi grew from non-existent with $0 in TVL to over $100 billion in TVL

- NFTs grew from non-existent to trading $100 million per week

There are numerous public resources available to check this information. For example:

- Cryptofees shows that applications like Uniswap and Layer 1 blockchains like Ethereum generate more fee income than Bitcoin. Additionally, many other apps and blockchains clearly show product-market fit.

- Token Terminal shows the revenue generation of numerous applications and blockchains, allowing you to compare and contrast which are a flash in the pan and which are generating consistent business.

- DefiLlama shows how each DeFi application across different Layer 1 blockchains is growing or contracting with regard to TVL.

- The Block is a treasure chest of data—from Bitcoin activity to the growth of stablecoins to the rise in NFTs.

- Other sites like Dune Analytics allow you to find dashboards on just about anything you’d ever want to search in the blockchain world. Curious about the Three Arrows’ NFT collection currently under Chapter 15 court supervision? There’s a dashboard for that. Wondering how Staked ETH is trading relative to ETH? There’s a dashboard for that. Curious how LooksRare is fairing versus OpenSea? There’s a dashboard for that.

The digital assets sector is under constant fire from traditional finance, the media, regulators, and everyday naysayers. So we don’t need those within the industry also perpetuating false information. We can love Bitcoin without falsifying its dominance. In the spirit of educating a new generation of digital asset investors, we should point investors to the tools and resources that can help them understand the ecosystem and make informed decisions—not feed them unsubstantiated narratives in the hopes of preying on the uninformed.

At Arca, we speak to investors every day. Many are now more knowledgeable about blockchain and digital assets because they took the time to learn. Unfortunately, others are still entering the space with skepticism due to misinformation and misconceptions driven by those who get the most air time. Fortunately, the data now speaks for itself. So let’s use it.

Breaking Down Layer 1 Valuations From First Principles

Written by Nick Hotz, CFA - Research Associate

In February, I wrote "Are Blockchains Businesses or Nations?". The piece analyzed some popular frameworks for evaluating Layer 1 blockchains from thought leaders in the space, categorizing them as regarding blockchains as businesses with equity-like tokens or nations with currency-like tokens. I formed a middle ground, seeing merit in both frameworks while not taking a stance on how to value the chains’ native tokens. Analysts have relied on various metrics to understand how to value these assets, including discounted cash flows, price-to-earnings, number of developers, number of transactions, active addresses, and many more. But while all have nudged us in the right direction toward understanding token value, none have articulated what is actually fundamentally driving flows to and from these assets.

Today, I'm no longer on the fence. Layer 1 protocol tokens are clearly currencies.

And just like every other currency, the forces that drive currencies are supply and demand. Every metric used thus far has attempted to quantify some aspect of one of these, but none has taken it back to first principles. In this piece, I'll illustrate what drives these assets by viewing them as what they really are: cryptocurrencies.

First Principles: The Supply Side

Supply is the far less important and easier to quantify part of the supply-demand equation for most L1s. Similar to fiat currencies, supply can be broken down into two simple components: how much new supply is added to circulation and how much existing supply is removed.

Adding New Supply: Bad

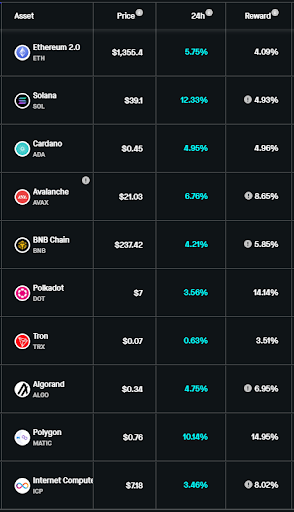

In the case of fiat currencies, there are two main drivers of new supply: the commercial banking system and the federal government—both of which "print" new money out of thin air. Since the crypto economy isn't based on credit like the fiat economy, only one entity can issue new supply: the blockchain itself. For Bitcoin, new currency "printed" by the blockchain is paid out to validators as a block reward (see annualized rates below). However, newer blockchains have also issued to founders, the team, and others for ecosystem development—essentially running a budget deficit to stimulate the burgeoning economy. All else equal, adding new circulating supply reduces the cryptocurrency's value because it makes it less scarce.

Source: stakingrewards.com

Removing Old Supply: Good

Just like the case for adding new supply, there are two main ways of removing money supply from the fiat system. First, people can pay back their debts. This is what happened with Covid stimulus checks: rather than spend the money, many people took the opportunity to pay down debts, erasing this newly created money from the system. The other way is for people to pay their taxes. The government creates money out of thin air by spending; similarly, it removes money from the system via taxation. Again, since the crypto-economy isn't credit-based, the only way to remove supply is via taxation—or burning fees (see below). Burning tokens is simply a way of stabilizing the money supply to ensure newly printed currency doesn't inflate away the token’s value. All else equal, burning old circulating supply increases the cryptocurrency's value because it makes the token more scarce.

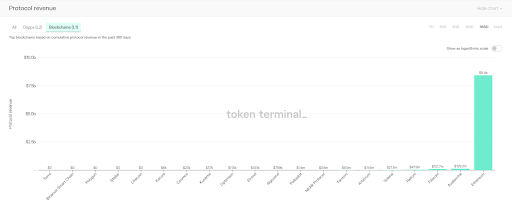

Currently, only one cryptocurrency has a net deflationary supply side adding value to the token—BNB, which issues zero new supply and burns a portion of fees. The rest of the bunch make it up on the demand side.

Source: Token Terminal

First Principles: The Demand Side

Cryptocurrency prices are so volatile due to the much more complex and variable demand side of the equation. No one is sure how important, stable, or useful blockchains will be in the future, so estimates of the future of the demand side vary wildly. The relationship of demand to supply for currencies is also dynamic and overlapping. Even so, there are only a handful of demand drivers for cryptocurrencies that link back to fundamental flows.

Increasing Real Interest Rates: Good

One of the most important drivers of relative currency values worldwide is their interest rates. All else equal, capital flows to currencies with high interest rates and out of currencies with low interest rates after adjusting for inflation. During the L1 rotation trade of 2021, relative interest rates were the main story, with yield farmers sending capital flying between various blockchains in pursuit of whichever economy was providing the highest interest rate. These rates were almost completely offset by inflation (adding new supply: bad), which made it a hot-potato rotation game rather than a fundamental bet on the future of blockchain. Taking advantage of these high interest rates required getting in early, snapping up as much of the yield as possible, and converting into a harder asset (stablecoins, BTC, or ETH) before the free money spigot turned off completely.

Relative interest rates also explain much of our current predicament. In the name of getting tough on inflation, global central banks have been aggressively tightening monetary policy throughout the year, with interest rates rising globally. By far, the most important actor has also been the harshest: the U.S. Federal Reserve. U.S. rates have already come up by 1.5% from near zero with further hikes planned for the future, funneling financial capital worldwide into the U.S. dollar. With newly sober investors no longer willing to finance blockchains printing free money (see above), interest rates in crypto-land collapsed, creating a double whammy of capital outflows back into fiat—especially U.S. dollars (see below).

Source: TradingView

Increasing Expected Usage: Only Feeds Into Other Fundamentals

Expecting more usage of the blockchain is not a first principles reason for wanting to own a currency. However, since so many investors focus on it, I thought it was important to mention it. The key point is that increasing expected usage is only valuable if it can reduce supply or increase demand in some other way for the blockchain.

Many blockchains tie their fee burn to economic activity on the chain. Ethereum, BNB Smart Chain, Avalanche, and Solana all do this—they burn more tokens when the economy is running hotter and gas fees are plentiful; they burn less when the opposite is true. In all of these cases, an increase in expected usage directly leads to expectations of more tokens burned and a lower future token supply (see: Removing Old Supply: Good), meaning all else equal, the price should rise.

Fees can come in different forms. In Ethereum post-EIP-1559, the burned base fees are the general fees paid simply for access to space in a block. Users can also pay priority fees to move ahead within a block. These fees go to miners instead of being burned. Solana is implementing a similar mechanism in localized fee markets, where users can pay to access transactions with highly demanded accounts. In a proof of stake system, these fees are paid out to stakers. See where I'm going with this? An increase in expected usage of the chain can also mean more priority fees, which increases the real interest rate of the cryptocurrency relative to other assets. And an increasing real interest rate is positive for the currency’s price because capital will flow into the currency to take advantage of higher yields.

More activity on the blockchain also leads to more inefficiencies. Mispricings between decentralized exchanges, underwater borrowers in need of liquidation, or even frontrunning opportunities abound as financial activity blossoms. In the fiat world, we turn to Wall Street to iron out these inefficiencies and ensure everything is priced correctly—at a societal cost. In the blockchain world, so-called maximum extractable value (MEV) searchers seek out this extractable value and arbitrage it away for themselves. However, as the MEV game has grown, so has the competition. Arbitrage opportunities still come up, but many MEV searchers often find them simultaneously. Searchers are forced to submit bribe payments directly to block producers to have their arbitrage be the one that makes it into the block. The advent of Flashbots on Ethereum has distributed these bribes to validators, which will go to stakers after the merge. As financial activity increases, the size of MEV increases, increasing the bribe payments to stakers, once again increasing the real interest rate and the price of the cryptocurrency.

The decrease in expected near-term usage of blockchains likely played a role in the current downturn by feeding into other supply and demand factors that determine flows into and out of their currencies.

Where Other Metrics Fit In:

Other metrics and models can still be helpful and are relevant for token-based applications that are not Layer 1 blockchains. Still, we need to be cognizant of their limitations regarding blockchains and understand where they demonstrate value accrual to the currency.

- Discounted Cash Flow - An absolute way of valuing removed old supply; fails to take into account new supply and interest rates; doesn't apply to currencies

- P/E Ratio - A relative way of valuing removed old supply; fails to take into account new supply and interest rates; doesn't apply to currencies

- Number of developers - A leading indicator of usage, which is not a fundamental driver of capital flows

- Transactions - A coincident indicator of usage, which is not a fundamental driver of capital flows

- Active Addresses - A coincident indicator of usage, which is not a fundamental driver of capital flows

- Total Value Locked - A coincident indicator of usage, which is not a fundamental driver of capital flows

- Fees Generated - A proxy for real interest rates but doesn't factor in the supply side

A Note on Bitcoin: Need for Fees

As an asset with no visible interest rate and a fixed supply schedule, Bitcoin would seem to be a poor candidate for this framework. But BTC fits too. Bitcoin's entire value proposition is being the hardest money possible. In economics terms, the ideal end game for Bitcoin is an infinitely sustainable zero real interest rate: zero interest paid out by the asset and zero inflation. For Bitcoin to be sustainable as its inflation subsidy ticks towards zero, it needs fee revenue to continue paying miners to secure the chain. As a result, increased economic activity directly leads to a more credible interest rate policy and higher real interest rates. Given that Bitcoin's roadmap has made its sole purpose holding and never transacting bitcoin, color me skeptical that it will achieve sufficient activity to make it sustainable.

A Note on the Ethereum Merge: Mispricing, But Not Where You Think

As I've highlighted, the switch to proof-of-stake is certainly a bullish event for the ETH currency. While staking yields are currently paid only from inflationary rewards, the merge will put valuable priority fees and MEV bribes in the hands of stakers, dramatically increasing real interest rates. Additionally, the switch will slash security costs, reducing the amount of issuance needed to secure the chain. A drop in new supply of the asset plus a rise in demand for the asset equals “number go up.” Simple, everyone gets it.

But that's not the whole story. Eager traders were quick to bid up DeFi assets as merge speculation heated up this week, assuming that the merge must be good for all things Ethereum. This couldn't be more wrong.

Source: TradingView

The merge is bullish for ETH and staking products only. But it's bearish for activity on Ethereum. There's a good reason why, until very recently, global central banks kept the easy money flowing over the past decade-plus. Holding down real interest rates stimulates the economy by encouraging credit creation and borrowing. When real interest rates rise significantly, lenders don't have to take credit risk to get the same returns, so they stop lending. After the merge, why would anyone take smart contract risk lending ETH at 0.76% on Aave when they could earn a risk-free 5-7% in the staking contract?

Source: Aave

Raising real interest rates, by definition, raises the cost of capital and slows the economy. That's good for the currency but bad for all the equity on top of it. Don't expect DeFi's merge anticipation rally to continue for long.

It's All About Perspective

For good reason, it has become unpopular to call all digital assets "cryptocurrencies." However, in the specific instance of Layer 1s, it's the correct framework to think about them. Currencies aren't possible to value on an absolute basis, but any FX trader worth their salt is very familiar with the fundamental factors that drive changes in their exchange rates. Net supply changes, real interest rates, and the structural demand forces that drive those factors are how fundamentals feed into currency markets. Momentum plays a huge role in both currency and cryptocurrency markets. And those same forces determining interest rates in other currencies like the dollar impact exchange flows worldwide.

Tokenomics are hard. We're pretty sure crypto assets have some value, but knowing exactly how much is also hard. Let's at least start from the same first principles. Layer 1 tokens are currencies, not equities. They should be valued with basic economic forces of supply and demand, not tangential factors like developer counts, Nakamoto coefficients, or P/E ratios. At least that's a start.