What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

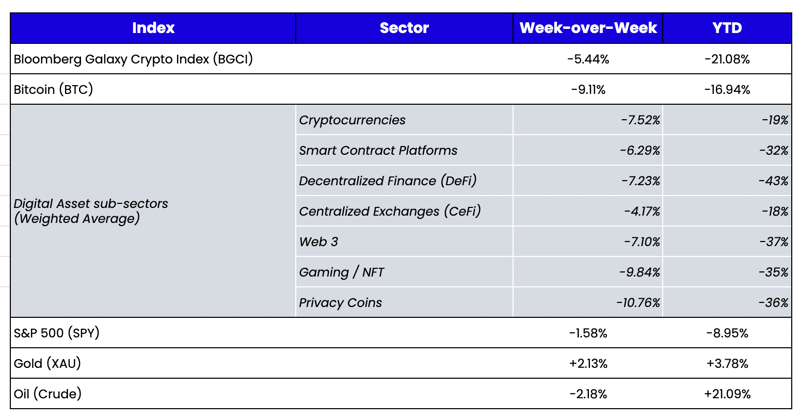

Week-over-Week Price Changes (as of Sunday, 2/20/21)

Source: TradingView, CNBC, Bloomberg, Messari

Oh, Canada!

We’ve written about digital assets every week for over four years, but for the past few months, there’s been little to write about specific to digital assets, their fundamentals, or their price performance. For the time being, the assets packaged inside of digital assets are standing as a risk outlet for expressing macro and geopolitical views.

The increased pace of year-over-year CPI growth and subsequent increased rate hike expectations became a major catalyst for the decline in tech stocks and digital assets over the past 3 months. Rising rates are currently viewed as bad for risk assets, despite little evidence to back that assumption. But how does one reconcile that with the fact that digital assets and equities accelerated their declines last week—even though U.S. Treasuries regained their safe-haven status, rallying in the face of geopolitical tensions as the probability of a 50 bps hike in March decreased to 21% from 49% (and from 95% at its peak)? According to Deutsche Bank, geopolitical “risk-off” events have historically been short-lived for equities, with a median sell-off of -5.7% with an average of 3 weeks to reach a bottom and a further 3 weeks to recover prior levels. On average, the market gains +6.5% and +13% from the bottom 3 and 12 months after. So after we move past rates and move past war, it’s anyone’s guess what the next overarching theme will be.

Meanwhile, events specific to digital assets are being shrugged off for the moment. Even more significant events—like the freezing of Canadian protesters’ bank accounts—were largely swept under the rug. In addition, the Royal Canadian Mounted Police targeted transactions linked to digital asset addresses suspected of funding these protests. These totalitarian actions reinforce the topic of self-custody. They can potentially provide a boost to digital asset adoption, though very little forward-looking positivity has seeped into prices thus far. However, there are several takeaways:

- This is undeniably positive for true decentralized projects like algorithmic stablecoins (UST) and privacy coins. Stablecoins have grown to over $170 billion in AUM in short order. However, the largest (USDT and USDC) are still subject to a few decision-makers being told what to do.

- We’re likely to see increased digital asset inflows from Canada, though it is ironic that most of these flows are into centralized venues (such as Purpose Fund’s BTC ETF), which suffer the same “shut down” potential as the banks they are fleeing.

- These events highlight further discussions around the practices of U.S. banks, which continue to randomly shut down accounts of any business or individual associated with digital assets.

Everywhere you look, there is a story about overreach, hypocrisy and flat-out insanity from the traditional bank/brokerage/government rails. And in the era of social media, these stories are far-reaching and influential, inspiring a quiet revolution against governments and banks. For now, the market is more keyed in on the negative than the positive, but ultimately, digital assets won’t live outside of this system forever. For the time being, though, it is certainly refreshing to be unencumbered by this nonsense.

Are Blockchains Businesses or Are They Nations?

Written by Nick Hotz, Research Associate

Debate continues to rage about how to value and define digital assets in the context of the investable universe. While Bitcoin recently passed its 13th birthday, most of the assets we know today are still toddlers in comparison. “DeFi summer,” which spawned the first big wave of real blockchain applications, occurred just over a year and a half ago. Most other successful applications where we see immense value are no more than three years old. At Arca, we have consistently asserted that new emerging sectors in the blockchain application space (like DeFi, NFTs, gaming, and Web3—including its various subsectors in file storage, cloud computing, and telecom) look strikingly similar to traditional startup companies. But despite being around the longest, one sector has defied classification: the blockchain protocols and platforms themselves.

Layer 1 (L1) blockchains like Ethereum, Avalanche, and Terra—or even Layer 2s (L2s) like Polygon, Ronin, and Arbitrum resist an easy definition or valuation attempt. So although we can be sure their tokens have some value, they don’t serve an easily defined need for users. For example, certain DeFi applications, like Sushiswap, are simple businesses that let users trade tokens; they provide a cut of the profits to tokenholders, lending themselves to a simple enough valuation model. But protocols and platforms, like Avalanche, are more like the internet or the Apple app store, whereby one can build applications on top of the protocol. Still, it's not as easy to value since it includes its native token that runs the show.

Despite the complications, two camps seem to have emerged in thinking about the value and structure of blockchains. One camp, blockchains as businesses (BaB) consists of practical, traditional, financially-friendly folks who view blockchains as companies with definable cash flows, product-market-fit, and business models. The other group, blockchains as nations (BaN) are macro-brain dreamers who see blockchains instead as nations that support their own governments, economies, militaries, and taxation systems. The two vastly different frameworks lead to disparate views about these chains' value: the BaB sect is focused on returned value to tokenholders today, while the BaN sect is more concerned with new user and economic growth than tokenholder compensation. The division also leads to people talking past each other as they focus on entirely different metrics to evaluate their favorite chain.

As someone straddling the fence between these warring factions, I have learned from each side that both have merit in describing this subsector of digital assets.

The Case for Blockchains as Businesses (BaB)

When viewed from a traditional finance framework, it is not difficult to make the case that blockchains look a lot like businesses. Ryan Sean Adams of Bankless perhaps says it best, claiming, “Blockchains sell blocks.” Blocks can be sold B2C (to users) or B2B (to other chains), but both ways result in revenue for the selling chain. For a business that sells blocks, increasing the quantity and price of blocks is the pinnacle of success. BaB advocates focus on fees generated—a proxy for revenue earned by the chain to signal product-market-fit. Through fees, they seek the holy grail of returning cash to tokenholders, either through deflationary monetary policy or through other free cash flows (such as staking rewards). In addition to assuring the economic security of the network, these metrics also signal a great investment opportunity.

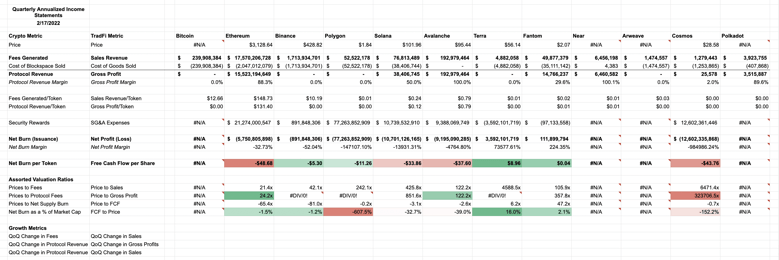

Analysts like Ryan Allis have attempted to value Layer 1s (in this case Ethereum) based on fundamental cash flow metrics that will be incorporated after Ethereum’s Merge event later this year. Allis finds that Ether trades a significant discount to its fundamental valuation of over $10,000 per token based on future cash flows from staking (like an on-chain dividend) and from deflation of the money supply (like a share buy-back). Blasphemy to the BaN camp, a discounted cash flow model is a staple for analytically-minded BaB advocates.

Source: Arca Internal Research, Token Terminal, Coin Gecko, various blockscanners

Looking at the numbers objectively, some blockchains are currently much better businesses than others. L1s like Ethereum—and to a lesser extent, Binance Smart Chain—rake in fees due to relatively high gas fees and full blocks. These are the cash cows of the blockchain space and, for BaB, have the fundamentals today to justify a solid investment. Terra could also be slotted in this category due to its historically deflationary monetary policy returning value to tokenholders (stablecoins are a great business too!) On the other hand, chains like Solana, Polygon, Cosmos, and Avalanche generate only nominal fees and have much more heavy inflationary token supplies—kryptonite to a BaB’er.

All-star digital assets metrics and research provider, Token Terminal, takes the same approach, assigning blockchain’s fundamental metrics like revenue, a price to sales ratio, and a price to earnings ratio the same way it does with application layer businesses like Sushi and Axie Infinity. However, given the different fee policies and heavy token issuance rates of many blockchains, this approach can run into problems when making comparisons. For example, although Terra has returned value to holders of its native LUNA via deflation, Token Terminal doesn’t assign any “earnings” or P/E ratio since it doesn’t burn fees.

Another critical issue with viewing blockchains as businesses is the currency in which they generate fees. Unlike every business in the world, blockchains exclusively earn revenue and profit in their native token, not external money like the U.S. dollar. To a critic, it’s like saying that Amazon “earned a profit” when it repurchased its own shares, rather than when it received new cash. To bridge this belief, the BaB camp views their native tokens as fundamentally new assets that encompass the properties of capital assets, consumable assets, and store of value assets. When framed as a novel asset class, it’s easier to overlook how exactly L1 native tokens earn their revenue.

BaB advocates fundamentally start from a framework that views fiat currency, particularly the U.S. dollar, as the global Unit of Account. As a result, fees generated in the native token of a blockchain are valuable since a consumer decided to purchase blockspace rather than using their dollars to spend on something else. I’m not passing judgement on this view, and believe that it's likely the more practical of the two. However, there is another way to look at the problem: viewing blockchains in an entirely different way—as nations rather than businesses.

The Case for Blockchains as Nations (BaN)

One of the oddest things to a financially-savvy newcomer in the Web3 space is the tribalism between the various L1 communities. Bitcoin people and Ethereum people seem to despise each other, while tensions often flare between Ethereum advocates and those of other “newcomer” L1s. For someone familiar with investing, it's not something seen in any other asset class. There’s no one willing to go to (social) war over the merits of Coca-Cola vs. Pepsi. People don’t identify with owning shares of Goldman Sachs over JP Morgan Chase. But for some reason, this is how things play out in the various digital asset communities.

While much more difficult to notice for their native assets (probably due to their stability), such patriotism around particular communities is prevalent among the residents of nations. An Ethereum maximalist and a Solana maximalist might fight within the confines of the blockchain world, but will band together against traditional finance to promote the efficacy of blockchains. The dynamic is not dissimilar to how neighboring nations might fight along their borders, but would band together against other cultures if they met in New York City. When people are deeply involved in their communities, they are passionate about them. And when their social, financial, and physical health are on the line, they are willing to lay down anything to defend their values.

Indeed, with a slight squint, the social structures of blockchains also resemble those of nations. When a country first forms, it is a blank canvas with unlimited potential but no real economic value other than “future option value.” But over time, as a society builds roads, schools, and other businesses, a country begins to grow its GDP and tax revenues. The same is true of a blockchain as it moves from early formation and speculative value to a thriving metropolis with apps and transaction revenues. Validating nodes “elect” the government and the rules by which society functions. Miners and stakers serve as the military, providing security to defend the nation from potential attackers. However, with enough of the military defecting, blockchains can suffer brutal civil wars. Chains support diverse economies with goods (NFTs) and services, plus deep decentralized financialization and trade routes (bridges) to connect it all. Much of the activity takes place in the nation’s native token, which is the primary medium of exchange of value. This token is also used to pay gas “taxes” that support public goods that serve everyone who uses the chain.

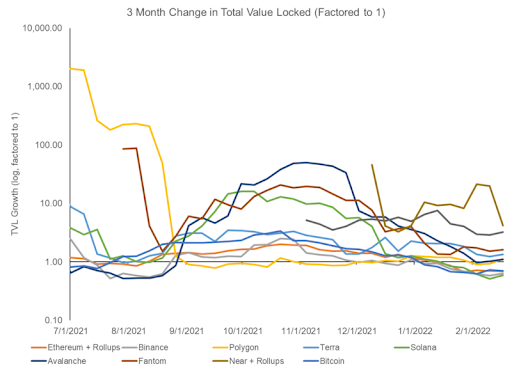

To camp BaN, it seems silly for BaB to value tokens by the amount of taxes paid by residents of the nation. Native tokens are currencies, and the most important thing for a currency is to be used in a large and dynamic economy. With reserve currency status eventually on the line but chains so early in their development, it’s currently anyone’s game. Growth, not current value, matters; what will really move prices in the long-term is inflows into their native economies, not tokenholder-friendly tokenomics. When growth is what matters, a chart like the one below is more useful for analysis than understanding fees and profitability.

Source: Arca Internal Research, DeFi Llama

We see the winners of the past eight months (Polygon, Solana, Avalanche) stand out as fast growers, while Ethereum, Binance, and Bitcoin are slow and steady. In an emerging world of digital nations as seen by camp BaN, network effects are weak, and there's no room for complacency among the current dominant players. The persistent high fees of Ethereum—and to a lesser extent Binance Smart Chain—are an opportunity for other chains to compete with lower tax rates to attract users and capital to their “countries.”

Natasha Che of Tascha Labs sits firmly in this camp, proposing that L1 blockchains are instead closer to governments than to businesses, with tokens as their native currencies that grow in value as the “GDP” of their economies expand. She also authored a bear case on Ethereum, arguing that comparably slower growth and the shift to Layer 2s, which remove a direct connection to users, will make Ethereum a laggard compared to other L1s.

Haseeb Qureshi of Dragonfly takes a similar vantage, analogizing blockchains to cities that scale up and out but eventually get too full/expensive and force new cities to spring up. For example, expensive but culturally iconic Ethereum is New York City, but adventurous souls head West to settle in Los Angeles (Solana), Chicago (Avalanche), and San Francisco (Near). Haseeb’s city analogy is a forceful defense of a multichain future (it would be completely crazy for there to be only one city in the whole world) and also suggests that these U.S. cities will be able to coexist and even collaborate, rather than kill each other.

While he has sometimes raised an olive branch to the BaB camp, a16z’s Chris Dixon is another example of someone who waxes poetic about the BaN gospel. Chris speaks of Web3 as a messy but dynamic and lively city, while Web2 is Disneyland—clean and beautiful but highly curated and unnatural. To Chris, blockchains facilitate composable digital economies; new economies spring up, where anyone can create new goods and services to trade with others. They certainly aren’t simply Disneyland-like businesses for tokenholders to extract a profit.

While this framework probably better describes how blockchains are structured, the BaB sect would argue (correctly) that its practicality is limited. Since currencies can’t be fundamentally valued, the only way to invest for the BaN sect is to follow the momentum as financial value and citizens rotate between and adopt different chains. While a community native could have strong beliefs in the technology or social structures underpinning a specific chain, investors may have a tougher time getting comfortable with a token based on these more qualitative judgements alone.

To onboard the world to these systems, we need to help people understand blockchains in ways that resonate with them. For some, it's easy to see the analogies to traditional businesses; for others, the more revolutionary framing of blockchains as nations may make more sense. Both have merit in explaining the emerging world of Web3 and in valuing its largest assets. Which one resonates more with you? The answer could reveal blind spots that you may have missed and help you understand why many people are passionate about this space.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Director of Research

Hassan Bassiri, CFA - Portfolio Manager

Sasha Fleyshman - Portfolio Manager

Alex Woodard - Research Analyst

Andrew Stein, CFA - Research Analyst

Nick Hotz, CFA - Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Defi Trader

David Nage - Principal, Venture Investing

Michael Dershewitz - Principal, Venture Investing

Michal Benedykcinski - Research Analyst

Andrew Masotti - Trading Operations

Topher Macpherson - Trading Operations

To learn more or talk to us about investing in digital assets and cryptocurrency