A Small Cap Crypto Rally on Actual Fundamental Strength

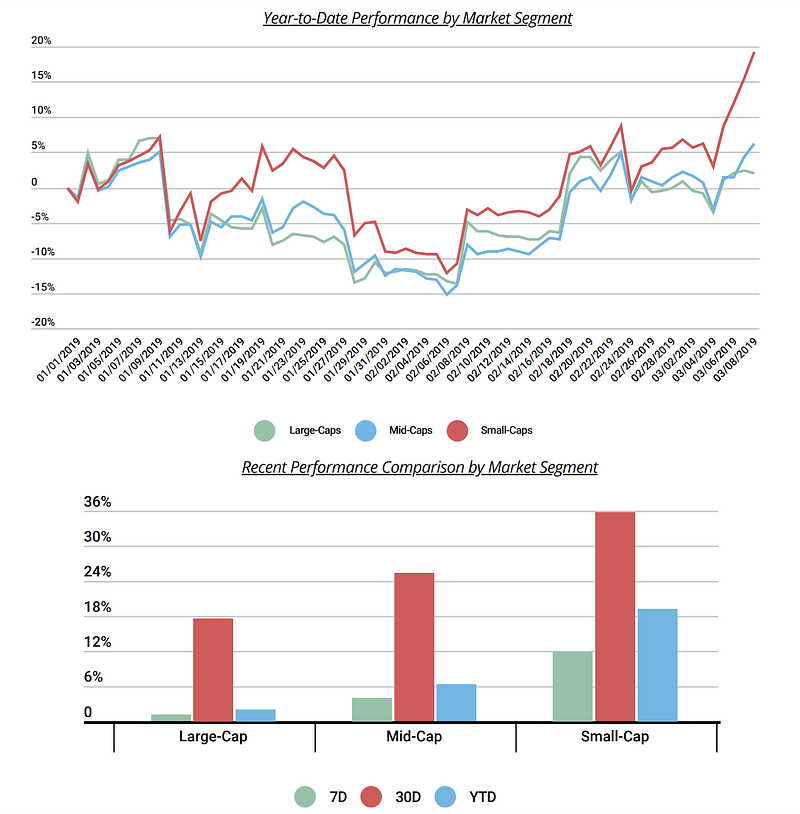

The crypto markets continued to rally last week, posting another 3–6% weekly gain. Notably, the last 6 weeks of gains have occurred without the most well known large cap tokens and coins contributing, with both Bitcoin and Ethereum lagging the broader market. In fact, most of the “legacy” large-cap tokens have been stagnant compared to the new up and comers in crypto, as 12 of the top 100 tokens by market cap rallied 20% or more last week, and only 1 was in the top 10 (Binance Coin — BNB).

Some of these small-cap tokens have already gained more than 100% YTD. And while those numbers seem a bit silly on the surface, for a bit of perspective, most of these tokens fell 90% or more last year and dropped 50% in November 2018 alone. So even after rallying 100%, they are STILL 80% below the all time highs. Said another way, this is why this asset class is so asymmetric to the upside. We’re not even back to November 2018 levels (pre-50% market crash) even after a huge rally.

Relative Value and Thematic Investing

While this isn’t a full blown “alt rally” quite yet, there are some interesting trends occurring that point to continued signs of maturity and overall market health. Using Binance Coin as an example, BNB is up 30% MTD and 140% YTD on real fundamental strength. Binance is stealing market share from other exchanges, they have a token that is easy to value and easy to use, and they have launched new innovative products that require the use of the BNB token. On the heels of BNB’s rapid ascent, the prices of other tokens linked to crypto exchanges (like KCS, HT, and BTMX) have exploded higher as well, as investors believe Binance’s growth can be replicated elsewhere. Similarly, Enjin Coin (ENJ) is up 500% YTD after news broke that Samsung is including the gaming application in its new Galaxy S10 phone. As a result, other Asian-based tokens have rallied significantly, as have other gaming-based applications. Lastly, Basic Attention Token (BAT) has rallied 50% YTD due to growth in popularity of the Brave Browser, which utilizes the BAT token. As a result, other tokens backed by real usable applications that are primed for increased adoption have outperformed the tokens of projects that have yet to produce a working product.

Thematic investing and relative value strategies are quite common in traditional asset classes like equities and fixed income, but are fairly new in crypto, and speak to the maturation of this asset class. While traditional analysts and traders are trained to look for “what’s next” after significant news comes out (i.e. if you miss the MGM rally, you quickly buy other casino stocks/bonds that will benefit from the same trends that are causing MGM’s growth), crypto has historically been dominated by momentum traders and algos/quants who don’t pay much attention to fundamentals. It is undoubtedly positive that real news and real analysis is dominating trade volume and price action.

Bottom line: Equities are starting to lose steam as the bear market rally wears off. The risk-reward to owning U.S. equities remains unfavorable with the S&P 500 trading at lofty forward earnings multiples, while global economic data continues to disappoint. Meanwhile, crypto is gaining steam on real adoption, and investors are beginning to believe that one-off trends in specific tokens are now applicable to the broader industry itself.

So What About Bitcoin?

Glad you asked. While BTC’s 5% gain YTD seems paltry compared to the 9% gain in the S&P and the 20% gain in small-cap cryptos, there are plenty of reasons to be bullish on the #1 cryptocurrency.

Growth potential: Bitcoin’s $70 billion market cap is smaller than Starbucks (SBUX), less than 0.1% of the world’s population own Bitcoin yet, and global governments are practically begging you to diversify your holdings away from their reckless inflation-inducing spending.

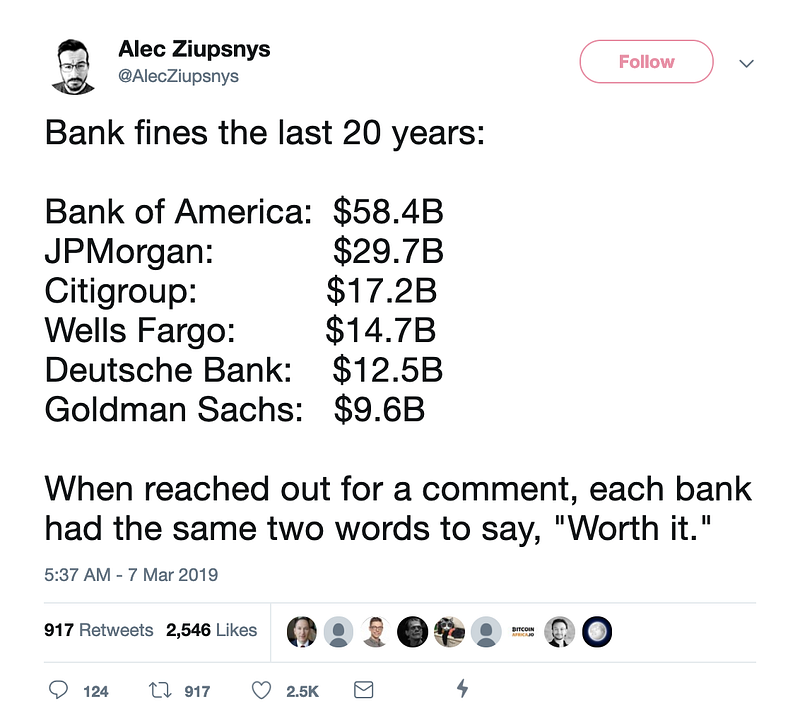

Bad Banks: While the mainstream media likes to link Bitcoin to the nefarious activities of criminals, it’s worth noting that most of the criminal money behavior happens within the walls of our own beloved banks. When entire market cap of crypto < bank fines , it’s probably a good indication that change is on the way.

Real use cases: Bitcoin has surpassed Paypal in annual transaction volume, which probably shocks most of us in the Western World who still have no real need to change the way we spend and transact. Just keep in mind that there are others out there who need this payment technology.

Network effect: The number of unique BTC addresses actively used has increased month-over-month to an average of 473k vs. 439k in January, and is now up 7 out of the last 8 months. According to Diar Research, the number of bitcoin addresses holding between 1 and 10 full BTC rose 6% since last February.

Bitcoin really is “fast money”: There is an interesting experiment taking place in real-time, where one Twitter user sends a few pennies worth of BTC to another user through the developing Lightning Network (an off-chain solution used to speed up the transaction speed of Bitcoin). This has now spread toJack Dorsey(CEO of Twitter),Fidelity, and even to Iran and back. This really is a new form of money transfer that is only akin to handing cash over in person to someone. So if Bitcoin is money, then it’s moving like nothing we’ve ever seen before.

So Why is Bitcoin Volatility so Low?

An excellent Twitter threaddigs into one of the largest and most controversial crypto exchanges, Bitmex, which offers up to 100x leverage via the use of perpetual swaps, and has been one of the main culprits for historically high levels of volatility in crypto. But during Q1 2019, the Bitmex Insurance Fund increased its BTC reserves resulting from liquidations at the lowest rate in over a year and this also corresponds to a decrease in theBitmex Funding Rate.

Bitmex does not charge interest on funding. Instead, the Funding Rate is exchanged directly P2P and is based on the notional value of the trader’s position (e.g., put up 1 BTC at $4K, the notional value is $400K). In general, the greater the notional value of a position, the higher the Funding Rate. When the funding rate decreases, it means trader’s have less notional value at risk implying less leverage.

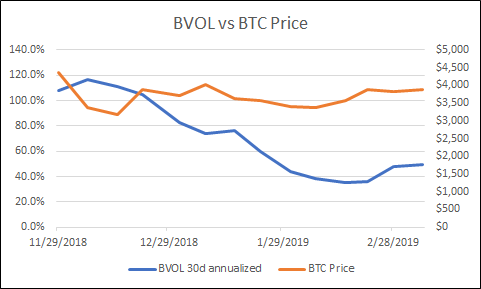

The takeaway is that this reduction in Bitmex leverage over Q1 nicely corresponds to a reduction in BVOL(a measure of Bitcoin volatility) which is currently at 50%, down from 83% at 1/1/2019 and well over 100% late last year. Using our example from above, when a trader with 100x leverage takes a long position and the market moves down, Bitmex forcefully liquidates the long position by selling 100 BTC at the market price. Clearly, these forced liquidations have had a substantial effect on price volatility.

It is difficult to tell whether reduced leverage is causing, or just correlated to, decreased volatility but it’s certainly an excellent observation. Regardless, the reduced volatility changes investor sentiment. Large, frequent drops in price are becoming less frequent and less likely, which in turn makes people more bullish. As volatility drops, confidence is restored, positions get larger, and time horizons expand.

As the author of the original tweet puts it, “[Bitmex] has robbed all his casino go’ers blind [and now] there’s no one left to sit down at the table…which is definitely healthy for those that want to see a market move higher”.

There is an increasing chance that the lows in Bitcoin may be behind us.

Notable Movers and Shakers

Enjin (ENJ) continues its tear, up 140% from last week. The Samsung partnership rumors, which started the token’s rally two weeks ago, were recently confirmed, further driving the price up.

Metadium (META), an identity protocol focused on Self-Sovereign Identity, rose 55% hot off the heels of its mainnet launch at the end of February, and is now up over 200% YTD.

Binance Coin (BNB), now up 140% since the beginning of the year, ran up 30% last week. We’ve talked at length about why the token is up (see: Testnet launch), but now according to CoinDesk, BNB is no longer tracking Bitcoin price.

Basic Attention Token (BAT) saw an 18% rise after new stats were released on the Brave browser. Brave currentlyhas over 20 million users, a massive number for any crypto-related consumer application.

According to a new study from Cisco, college dorms are the second most popular place to mine cryptocurrency, as electricity costs are included in the costs of housing. Cutting the cost of electricity from mining crypto significantly increases profits, and savvy students are taking advantage. Technology investors have always done well following early adoption signals from students — and this is no different.

According to the Worldwide Semiannual Blockchain Spending report from the International Data Corporation, worldwide spending on blockchain is expected to increase from $1.1b in 2018 to $2.9b in 2019. This 88% increase will be predominantly led by the financial sector, comprised of banking, insurance, securities and investment, which is expected to pour more than $1.1b into the space.

Facebook was in the news again last week, after the release of CEO Mark Zuckerberg’s blog post which focused on the future of Facebook: privacy. Privacy is the opposite ethos of what Facebook has historically encouraged, and this article posited that Facebook may offer customers a data dividendvia their payments platform in exchange for using their data. It seems the world is growing tired of Facebook’s abuse of power when it comes to data, and FB itself is seeing its platform decline — perhaps this move is more of a necessary response than a wanted response, and is a great example of the power of cryptonetworks, where control is given back to network users and not just network shareholders.

A16z explores how cryptonetworks function similarly to cooperatives and commit to further cooperation with their users over time, whereas traditional networks start competing with their users over time. In cryptonetworks, owners are not third-party shareholders, but are the users and builders, which provides different and continuous incentives for the enterprise to succeed.

Without diving into the political or moral debate, we point this out for one reason. Coinbase’s quick 360 degree “about face” shows the difference between a speed boat and an aircraft carrier — while Coinbase is the 800-pound gorilla in crypto, it’s still a tiny rather meaningless startup in the grand scheme of finance, and it can make decisions quickly and swiftly. This exemplifies the speed at which crypto is moving.

The idea of Precision Finance comes from Precision Medicine, where treatments and medical interventions are customized for each individual. With the advent of digital securities, financial structures, compliance and governance can be written into code. This allows for digital securities to represent specific assets within a company, or specific cash flow streams, rather than the company itself.

According to data from Citigroup, stock buybacks among S&P 500 companies reached over $800b in 2018, making it the first year since 2008 that buybacks topped capital expenditures.Mark Yusko of Morgan Creek Capital Managementweighed in on the debate noting that buybacks were actually illegal prior to 1982, raising the questions of whether or not companies should even be allowed to buy back their own stock. Regardless, when companies are goosing EPS instead of looking for growth mechanisms, it’s a dangerous sign for the economy.

The city of Denver, Colorado announced last week that it would pilot a blockchain-based voting app for voters who are overseas or on active military duty. Voting, one of the most promising applications of blockchain technology, will be conducted on the Voatzapp, which has already completed 30 successful pilots.

The world’s largest social investing platform, eToro, launched cryptocurrency trading services in the United States last week. The exchange, which already services 10 million users, is offering US customers in 32 states the ability to trade 13 digital assets and access to their multisignature wallet. eToro also offers users the ability to copy the portfolios that are curated by their analysts. Take a minute to let this sink in — investing, once a private endeavor, is now a social activity, and a natural extension from there is not just sharing in the gains, but actively contributing to them via crypto networks. Technology moves fast.

Arca in the Press & on the Streets

Join us forFO256- our one-day summit focused on digital assets for family offices and sophisticated investors. As of now, leading institutions such as Goldman Sachs, Fidelity, NYSE/ICE & Circle are joining the Arca team in addition to some of the best investors, lawyers and founders we know in the space to provide you real-time information on what’s happening in the digital assets & blockchain industry and how best to proceed into looking at investments.

And That’s Our Two Satoshis! Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team Jeff Dorman, CFA — Portfolio Manager Katie Talati — Head of Research Hassan Bassiri, CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

Subscribe For the Latest Blockchain News & Analysis

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation. Any decision to invest or take any other action with respect to any investments discussed in this commentary may involve risks not discussed, and therefore, such decisions should not be based solely on the information contained in this document. Please consult your own financial/legal/tax professional.

Statements in this communication may include forward-looking information and/or may be based on various assumptions. The forward-looking statements and other views or opinions expressed are those of the author, and are made as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated and there is no guarantee that any particular outcome will come to pass. The statements made herein are subject to change at any time. Arca disclaims any obligation to update or revise any statements or views expressed herein. Past performance is not a guarantee of future results and there can be no assurance that any future results will be realized. Some or all of the information provided herein may be or be based on statements of opinion. In addition, certain information provided herein may be based on third-party sources, which is believed to be accurate, but has not been independently verified. Arca and/or certain of its affiliates and/or clients may now, or in the future, hold a financial interest in investments that are the same as or substantially similar to the investments discussed in this commentary. No claims are made as to the profitability of such financial interests, now, in the past or in the future and Arca and/or its clients may sell such financial interests at any time. The information provided herein is not intended to be, nor should it be construed as an offer to sell or a solicitation of any offer to buy any securities, or a solicitation to provide investment advisory services.

.jpg)