Issac Newton is often credited with coining the phrase, "If I have seen further, it is by standing on the shoulders of giants." Though it is true he said this, he was not alone in sharing this sentiment, which has been stated in one form or another, since the Middle Ages. Our present state of advancement and technology is an aggregation of our previously gathered knowledge. This holds true in asset management as well. It is especially true at the dawn of asset management in the crypto space.

All of the structures, tools and methodologies that have been agreed upon and are extant in traditional finance need to be reimagined, recreated and reimplemented in the world of decentralized financial products. This includes how we think about the role of active vs passive investment strategies, especially in regard to crypto as an asset class.

Newton, Standing on the Shoulders of Giants

And this brings us to crypto and blockchain. Every day there are new headlines about the number of companies racing to create the first ETF that allows investors of all levels of sophistication to invest passively in crypto. These strategies range from the simplest, holding only Bitcoin, to the most sophisticated, following an index that tracks a basket of cryptos and blockchain products. So far, the SEC has resisted these efforts as they do not see the underlying asset—Bitcoin specifically, and crypto in general—as mature enough to be offered in an Investment Company Act of 1940 product. This industry does not need easier access for unsophisticated investors to speculate on crypto. This industry needs products that rise to the exacting standards of institutional investors.

It is these investors, making active decisions about underlying value, who allow passive strategies to work. Patrick Tan does a great job outlining the value of active management in The End of an Era & The Rise of Active Management for Cryptocurrencies:

Add to the inherent inefficiencies in the cryptocurrency markets, the complexity, and informational asymmetry and it’s not difficult to see why cryptocurrencies have what one manager refers to as a “knowledge premium.”

Call it “smart alpha” if you will, but even pedestrian strategies drawn from the capital markets and applied to the cryptocurrency markets — stuff that you’d be learning in a basic finance or trading course at any Ivy League school — can yield outsized returns.

And because there is informational asymmetry, passive investment strategies — cryptocurrency ETFs (where available) and cryptocurrency indexes are nowhere as effective as actively managed strategies.

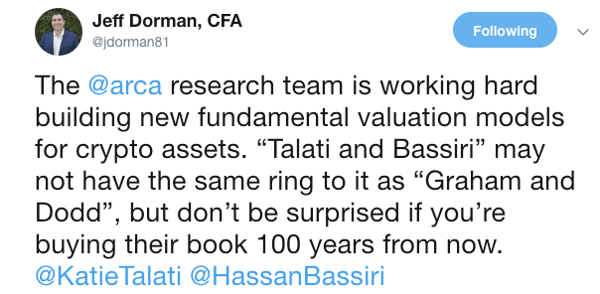

This is why I am picking up my active management sword. The giants on whose shoulders future passive crypto strategies will stand are still growing. We don’t yet know from which quarter they will emerge. Jeff Dorman of Arca said it succinctly:

Following financialization, firms that use index commodities make worse production decisions, earn 40% lower profits, and have 6% higher costs. Consistent with a feedback channel in which market participants learn from prices, our results suggest that index investing distorts the price signal thereby generating a negative externality that impedes firms' ability to make production decisions.

Additionally, our current low-to-no interest-rate environment has created a potent combination of factors that have accelerated the adoption of passive strategies. John Stepek details it in How central banks created the bubble in passive investing. Even central banks, such as the Bank of Japan, have used ETFs to buy the equities of Japanese companies, directly influencing asset prices. This type of naked asset-price manipulation makes the song-and-dance routines of Jay Powell and the Fed seem almost quaint by comparison. As Ben Hunt at Epsilon Theory warns,

“Capital Markets are being transformed into a Political Utility.”

.png)