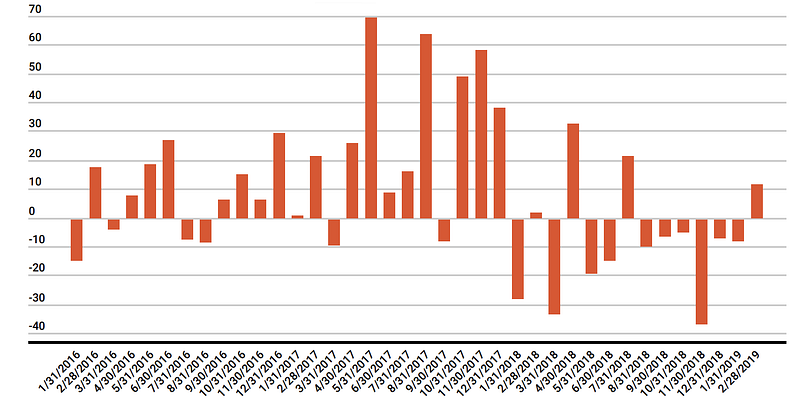

This past week didn’t provide much price action (crypto was mostly flat week-over-week), and that was a welcome calm. The lack of volatility helped Bitcoin and the rest of the crypto market lock in its first positive month since July, snapping a 6-month losing streak of negative returns. February’s gains (Bitcoin +12% / crypto indices +15–18%) provided some much needed relief for the industry.

Coincidentally, there is a noticeable change in investor sentiment right now, both from existing crypto investors and those on the fence peeking in. But it isn’t the price action that has people so excited — it’s the adoption. And by adoption we mean both actual use cases for digital assets on blockchain (the number of unique BTC addresses used increased MoM to an average of 473k vs. 439k in Jan, and is now up 7 out of the last 8 months) as well as adoption from incumbent financial powerhouses who are now entering the industry at a rapid clip (Facebook, Fidelity, Nasdaq, JP Morgan, Samsung, etc).

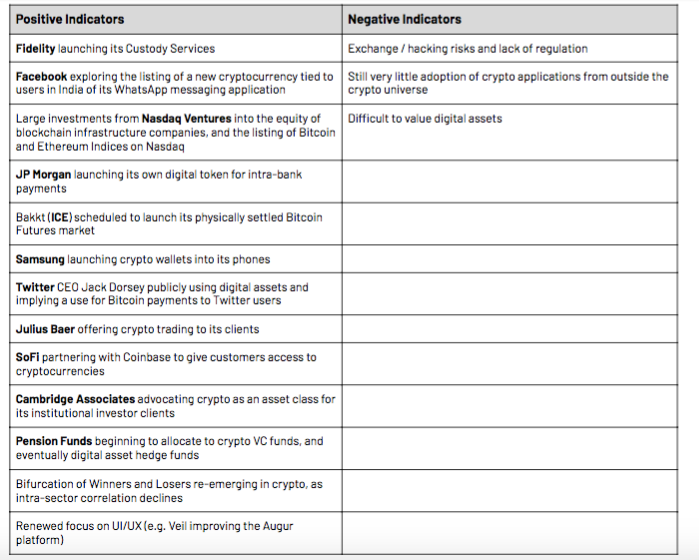

We’ve used the below table a few times in the past, but it’s worth mentioning again that just about everything in and around crypto seems bullish for the future of digital assets. And we’ve also noted that price is often a lagging indicator, so even after February’s gains, we could still be in the early innings of a massive recovery in asset prices.

This leads to a paradox. Just about everything long-term for digital assets is bullish, yet it’s still incredibly difficult to value and therefore have conviction on many crypto-assets that exist today, including to some extent Bitcoin. The bull case is simply that others are bullish enough to keep building / launching until we figure out the best use cases and valuation techniques for these assets.

Despite this paradox, the bull case just got a lot stronger now that the “others” include global financial and technology giants that bring with them enormous, engaged user bases. Crypto adoption, and thus price appreciation of digital assets, is solely based on network effect and growth of users, and while it’s exciting and fun to cheer for the grassroots efforts of new challengers in the space, it’s much more plausible that the industry will piggyback on the incumbents with already massive networks.

The Macro Factors Affecting Crypto Prices and Blockchain Adoption

The Angry Birds Corollary

New technologies without distribution often fail to materialize. There is a good reason why Betterment and Wealthfronthave largely stalled. Their technology is amazing, but also easily replicable by financial advisory powerhouses with larger distribution capabilities, who are now offering similar services to their clients. There are only so many new, young investors willing to start from scratch with unproven platforms like independent robo-advisors. Most everyone else just wants their existing advisor to keep up with new and better wealth management tools. Distribution and brand matter.

So while there are a lot of polarizing opinions on Facebook and JP Morgan’s entrance into the digital asset world, and the long-term importance (or lack thereof) of their token offerings, the fact of the matter is their day 1 will be bigger than our year 10. We need them, and we should embrace them. For example, I for one hate video games and especially hate Angry Birds. That is certainly NOT why I got an iPhone in 2010. But once in the iOS app store ecosystem, Angry Birds somehow made it on my phone and I played it many times. It doesn’t really matter what gets you into the ecosystem; once there, every blockchain app, and every digital token, becomes much more readily accessible.

Basic Attention Token (BAT) moved 28% after news hit that it waspartnering with TAP Network, a blockchain-based ad / data platform. The partnership allows users to use BAT for purchases at TAP’s 250,000 brand partners including Starbucks, Uber, Amazon and Nike.

Ravencoin (RVN) saw gains of 154% last week after listing on digital asset exchangeBittrexandadding a USD trading pair on Vertbase. Potentially unrelated but important to note, Ravencoin also started a#RavenTorchcampaign, similar to the Lightning Torch, which is currently being passed around Twitter.

The big news of last week was SoFi’s partnership with Coinbase to allow its customers to buy and sell cryptocurrencies through their SoFi Invest platform which went live earlier this month. Their new offerings also include robo-advising and index ETFs with waived fees, but their digital assets offering will continue to broaden adoption of crypto among consumers.

For digital assets to succeed, they need a strong network effect, and Bitcoin is the best example to date of a grassroots effort. Another way to create a network effect is to already have the network, and introduce a token to your massive audience. Last week we saw the JP Morgan Coin, and now Facebook moves closer to introducing it’s digital payment concept via WhatsApp.

Julius Baer, a major Swiss bank, has begun offering crypto trading for their clients last week through SEBA Crypto AG, a Swiss cryptocurrency bank. “We are convinced that digital assets will become a legitimate sustainable asset class of an investor’s portfolio”, according to official statements from representatives at the firm. Julius Baer joins the likes of Fidelity, Nasdaq and ICE as they begin entering and exploring the digital asset space.

Speaking of Fidelity,following their investment in Coin Metric’s seed round last week, Fidelity’s Digital Assets group published this piece discussing their outlook for crypto and the importance of having data-driven insights in the nascent and growing industry.

The area known as “middleware” in the digital assets space is comprised of businesses that are building solutions to help connect all the disparate networks currently in crypto. 2019 promises the launch of four middleware solutions, which could either be a boon to the crypto sphere or a complete flop, pointing to slower adoption long term.

Last week a bill was introduced in the California state legislature to allow Cannabis businesses to pay their taxes using stablecoins. If passed, the bill would allow businesses, which are often not granted access to traditional banking services, to pay their taxes in a cashless manner.

Although the title of this article misses the point, it’s important to discuss how other companies are attempting to use cryptocurrency and blockchain technology for payments. Facebook is planning to create a stabletoken that can be sent instantly through its messenger app, WhatsApp. Telegram, which has an avid user base on its secure messaging platform, is also planning on releasing a token, which presumably can be used to send within its messaging app.

Last week, Voyager, a publicly-listed crypto brokerage firm, agreed to purchase Ethos.io, a blockchain wallet provider. The purchase includes all of Ethos’s current products, “certain blockchain technology and IP”, and tokens sold during a 2017 initial coin offering. To date, the crypto space has seen a handful of acquisitions mostly performed with cash for equity. However, this may mark the start of M&A stepping outside of those boundaries.

According to a report from job site Hired, 2018 saw a staggering 517% increase in demand for blockchain engineer positions. The report, which also details median incomes, signifies that the blockchain space is still growing at a rapid pace despite the current bear market.

In this op-ed, a Venezuelan economist explains how Venezuelans protect their assets while still accessing the local economy. LocalBitcoins is an exchange that allows users to purchase BTC but also allows them to sell their crypto for local currency when they need to purchase everyday goods and services, protecting their assets from the ongoing inflation.

Arca in the Press & on the Streets

In last week’s“Reading the Merkle Leaves”, Arca Chief Legal Officer, Phil Liu, provides his thoughts on why exchanges need regulatory oversight, and that regulation is coming to the space very soon.

Arca CEO, Rayne Steinberg,penned his thoughts last weekon the (non) potential for Bitcoin to become a reserve currency in the traditional sense.

This Is A Big Headline For Crypto: Head of Strategic Relations, David Nage, discusses the importance of Cambridge Associates greenlighting crypto for pensions and endowments. He traces the history of Cambridge Associates’ involvement in evaluating various asset classes and highlights their thoughts on how allocators should invest in the space.

Don’t forget about[Block]Chain of Events, where the Arca Research team spearheaded by Katie Talati and Hassan Bassiri discuss recent events in crypto that dictate price action, focusing on how important transparency is to both price and adoption.

FO256, the crypto advocacy conference for family offices hosted by our own David Nage, is set for April 10th in New York. A host of Arca executives will be speaking. Let us know if you’re interested in joining

And That’s Our Two Satoshis! Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team Jeff Dorman, CFA — Portfolio Manager Katie Talati — Head of Research Hassan Bassiri, CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

Subscribe For the Latest Blockchain News & Analysis

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation. Any decision to invest or take any other action with respect to any investments discussed in this commentary may involve risks not discussed, and therefore, such decisions should not be based solely on the information contained in this document. Please consult your own financial/legal/tax professional.

Statements in this communication may include forward-looking information and/or may be based on various assumptions. The forward-looking statements and other views or opinions expressed are those of the author, and are made as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated and there is no guarantee that any particular outcome will come to pass. The statements made herein are subject to change at any time. Arca disclaims any obligation to update or revise any statements or views expressed herein. Past performance is not a guarantee of future results and there can be no assurance that any future results will be realized. Some or all of the information provided herein may be or be based on statements of opinion. In addition, certain information provided herein may be based on third-party sources, which is believed to be accurate, but has not been independently verified. Arca and/or certain of its affiliates and/or clients may now, or in the future, hold a financial interest in investments that are the same as or substantially similar to the investments discussed in this commentary. No claims are made as to the profitability of such financial interests, now, in the past or in the future and Arca and/or its clients may sell such financial interests at any time. The information provided herein is not intended to be, nor should it be construed as an offer to sell or a solicitation of any offer to buy any securities, or a solicitation to provide investment advisory services.

.jpg)