If you haven’t seen this headline from Bloomberg over the the last week let me quickly bring you up to speed before digging into why this is so important in crypto:

Why is this SO important? First let’s go into the history of Cambridge Associates who are the Adviser mentioned, who they service, what they do and then connect the dots.

For those unaware of CA here’s a brief history:

Cambridge Associates began working with a number of world-class educational endowments in 1973, pioneering the strategy of high-equity orientation and broad diversification. Building on our legacy of innovation, we have continuously evolved over the last four decades, working to stay at the forefront of the investment landscape and to deliver investment results for our clients.

So that’s the marketing line — here’s the real deal: if you’re on the investment team of a Family Office, Endowment or Pension there are a few things you do when looking to diversify risk and find some new exposures (this is not an exhaustive list but a few general things that are done):

The proof is in the numbers: Cambridge Associates has, as of mid-2018, $389 billion in assets under advisement, of which roughly $30 billion is managed for client on a discretionary basis — a 50% increase from 2017.

What Cambridge Associates Does

With more than 40 years of experience in alternative assets and public investments, we believe manager selection is crucial to successful investing, and we have experienced resources focused on a rigorous selection process to help us find nimble, innovative, and differentiated managers. With a global network of top-tier manager relationships, we use our scale to access best-in-class investments and negotiate favorable fees and terms on behalf of our clients.

Essentially Cambridge Associates, with regards to fund managers, is like the equivalent of a Brita water filter; it’s main job is to get to know every manager, their team, their internal processes, operations and much more — all at the end of the day to get the best drink of water possible (or in this case fund manager investment as possible). For many investors searching for new funds having diligence by CA is akin to having a Good Housekeeping seal of approval.

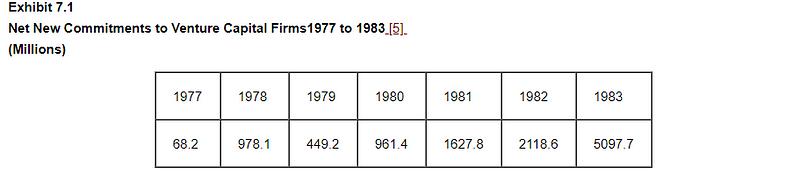

The 1970’s were a boom and bust time for Venture Capital; in the first half of the decade the industry was, in many ways, on life support. It was in 1978 that the attractiveness of venture capital received a shot in the arm in the form of regulatory assistance.

The 1978 Revenue Act reduced the capital gains rate from 49 1/2% to 28%. The flow of monies into venture capital funds jumped from $68 million to nearly $1 billon. Then in 1979, Congress passed the ERISA “Prudent Man” Rule that allowed pension funds to invest in venture capital. In the chart below we can see the massive growth of capital entering VC after the ERISA passage.

Cambridge Associates was right there in the mix in the 70's, providing Institutional Investors insights, diligence and research into an alternative asset class that was still emerging and new, just receiving a regulatory shot in the arm, ready to fire on all cylinders.

Although the crypto industry remains in its infancy, we think institutional investors should begin exploring it. A host of different investment options exist, ranging from an illiquid venture capital–like approach to a liquid hedge fund trading–like approach. Though these investments entail a high degree of risk, some may very well upend the digital world.

Upon reading that line a few things came to mind but mostly I asked “why now?” CA advises some of the most conservative Institutional Investors out there; the market cap has capitulated from $850B to $120B during “crypto winter”; what’s the catalyst for them to write this now?

I wasn’t surprised to read “the” why:

Beyond investment activity, the Intercontinental Exchange (ICE) formed a subsidiary called Bakkt to start trading physically settled bitcoin futures in early 2019. This follows the December 2017 launch of Bitcoin futures on the Chicago Mercantile Exchange. Fidelity announced plans to launch Fidelity Assets Services, LLC, which will be providing custody and trading solutions for enterprise clients. Furthermore, a number of projects have launched aimed at addressing key problems in the space, such as scalability, privacy, custody, cryptoasset volatility, interoperability, and governance.

As I wrote a few months back in The 10 Minute Guide to Investing in Crypto For Family Offices:

New market entrants: as discussed above the recent news from Fidelity, Goldman, Nomura, NYSE/ICE, TD Ameritrade and others in the traditional finance system is quite promising.

In essence Cambridge Associates is observing what many deep in the ecosystem have been discussing for the last 2–3 quarters; the infrastructure is hardening, is becoming more “institutional”. While the notion of self custody/self sovereignty is one I believe in personally and is meritorious, i.e “not your keys, not your crypto”, qualified custodians and back office systems to manage the potential billions of dollars of inflows from Institutional Investors who are used to those systems is necessary right now; Cambridge Associates is seeing that happening and thus a significant catalyst for investors to start peeking in.

I could write a conclusion to this article but the folks at Cambridge Associates who wrote this paper, Marcos Veremis and Alex Devnew, did it for me:

Although investors could rely on venture capital funds in their portfolio to determine their allocations to cryptoassets, there are strong reasons to consider a dedicated crypto fund investment. First, the SEC cap on non-qualifying investment could restrict their desired exposure. Second, the space is highly technical, meaning late entrants and non-specialists will be operating at a disadvantage to investors immersed in the space. Lastly, we expect partners specializing in crypto at traditional venture firms to spin out and launch their own dedicated crypto funds, as has already been the case. Taken together, these reasons mean investors could miss out on investments with the most knowledgeable managers in an industry with large potential payoffs.