What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

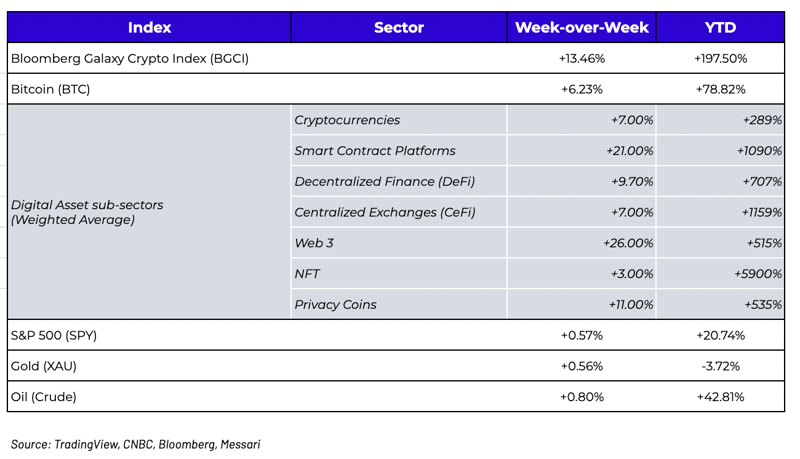

Week-over-Week Price Changes (as of Sunday, 9/05/21)

“Owning Bitcoin is like owning GE stock during the Dot.com boom”

Bitcoin investors rejoiced as Bitcoin finally broke out to a huge modest 6% gain last week, once again underperforming the broader market. The popular cryptocurrency is up a very respectable 78% YTD, but this places Bitcoin near last place amongst digital asset returns YTD, trailing almost all other currencies, smart contract protocols, DeFi apps, Web 3 tokens, NFT and gaming platforms, and just about everything else that is investable in digital form. The recent Bitcoin lull sparked a tweet suggesting that “owning Bitcoin is like owning GE stock during the Dotcom boom”, which is funny for a few reasons. First, it implies that a ~10-year old technological breakthrough that is now competing on the world stage as a legitimate currency contender and touches as many different investor types as US Treasuries is somehow now a boring conglomerate. Second, GE stock actually rose roughly +600% from 1995-2000, which was hardly a disappointing return, even if it did underperform the Nasdaq and many individual tech stocks.

But the point was clear… Bitcoin has never before been this unloved.

In fact, Real Vision released the results of their digital asset survey recently, and their audience now only holds just a 5.92% weighting to Bitcoin, down from 30-40% Bitcoin exposure in prior surveys. Compare this to the leading passive “diversified digital assets index”, the Bitwise 10, which still has an egregious 58% weighting towards Bitcoin. The tide has shifted.

We’ve been as vocal as anyone regarding why this shift makes sense and will likely continue. Bitcoin is a completely different asset than the rest of digital assets, with completely different attributes and properties, and an increasingly separate investor base. Further, there are seemingly endless possibilities for new digital token types and issuers, and as they are launched, evolve and succeed, it will naturally take market share from Bitcoin (meaning Bitcoin dominance, by definition, has to trend towards zero). That doesn’t mean Bitcoin will always underperform; it simply means that there is no reason why it should keep pace or perform in line with other completely different assets that share no semblance to the oldest cryptocurrency. But Bitcoin is far from dead. Last year you could have said similar things about Bitcoin’s relative underperformance, and Bitcoin went on to rise from the dead with a 168% gain in the final 3 months of 2020. It’s very likely that Bitcoin plays catchup again this year, as the macro environment continues to favor owning Bitcoin.

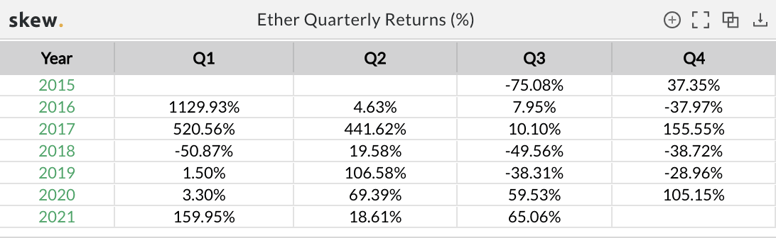

Meanwhile, Ethereum is gaining speed. Ethereum has gained 69%, 59%, 105%, 159%, 18% and 71% in the last 6 quarters. Total value locked has increased from $5 billion two years ago to $130 billion today. The leading non-custodial wallet for Ethereum and Ethereum-based applications, MetaMask, said its monthly active users hit 10 million in July, increasing from 545k monthly users in July 2020, representing growth of over 1,800%.

Source: Skew

And yet even Ethereum’s jaw-dropping 435% YTD return is taking a back-seat to other layer 1 smart contract protocols (like Solana +7545% YTD, Terra luna +5180% and Cardano +1538%), leading NFTs and NFT/gaming platforms (like Axie Infinity +13,853% YTD) and certain Web3 tokens (like Arweave +1982% YTD and Helium +1690% YTD), most of which are showing incredible fundamental growth supporting the increased market caps.

Needless to say, there is a lot going on in digital assets. And it all starts with the passionate (and sometimes myopic) communities.

WAGMI Ser

Don’t worry if you don’t know what “WAGMI” or “Ser” mean. Investing in digital assets these days requires learning a whole new vernacular. It also requires understanding passionate communities, the likes of which we’ve just flat out never seen before.

This past week, a new NFT was launched called “Loot”. In layman terms, it’s a series of index cards with random but unique words on them. The canvas is blank -- anyone can now build games using these NFTs, similar to how Ethereum was a blank smart contract canvas and any developer could build an app upon it. Loot is the equivalent of giving everyone playing cards before any card games were invented, but empowering and incentivizing everyone who owns a card to start creating games…. blackjack, euchre, poker, gin rummy, go fish, etc would all be built by random community members over time, but no one could play if they didn’t have access to the cards, and the profits from these games would be shared among token holders. Whether this works or not remains to be seen, but the sense of community and imagination is already overwhelming, as are the jokes about how fast this went from non-existent to self-perceived worth. But these grassroot projects are no joke -- it sparks something much deeper from a social investing and psychological standpoint.

Earlier this year, Gamestop (GME) and AMC Entertainment (AMC) made headlines after their stocks went parabolic, causing short-squeezes and government investigations into the Reddit community forums that led to the unnatural price appreciation. While everyone (other than Melvin Capital) had a good laugh, no one at the time thought that this would still be a story in late 2021 (Matt Levine at Bloomberg continues to write about these two stocks almost weekly). The assumption was that these were two dying companies, with manipulated stocks, that would fall back to earth after the day-traders were done screwing around. But despite mild pullbacks from the highs, GME is still +976% YTD and AMC is still +1976% YTD. The businesses themselves didn’t improve enough to warrant holding on to these market cap gains -- it was the communities that improved, giving the companies time and resources to maybe, just maybe, grow into something real and valuable again. The investors who own, or trade, these stocks just don’t care about what you or I think about valuation -- these stocks have united a group of like-minded investors and traders into something much bigger than green and red arrows. This is a support group, with open membership, where members want to be seen and heard, and take pride in being a member of the most expensive country clubs on the planet.

The only people who may have seen this longevity and sense of pride coming were digital asset investors.

By now, most have heard of the term “maximalism” as it pertains to Bitcoin maximalists, or Ethereum maximalists. The term describes a tribe- or cult-like persona that is so myopic in its view of a particular asset that it refuses to acknowledge the success or even existence of other competitors or complementary pieces. Often this can become toxic, but what’s lost in the output of this toxicity is how these maximalists got to this point in the first place. They rallied around “no one believed in us”, and “us against the world” mentalities, and naturally bonded over collectively winning at the expense of short-sellers and naysayers. These maximalist views are powerful with strong roots. Cardano (ADA) now has a $92 billion market cap. The protocol finally launched smart contracts this past week after six years of promises and peer-review. The launch was, to say the least, uninspiring. A rational investment thesis might be to short ADA, as it trades at 20% of the value of Ethereum, with about 1-over-infinity less traction and economic output. A rational investment thesis doesn’t take into account how absurdly passionate and confident this community is. Without the risk of default, Cardano can go on forever making promises, and the community will be there to support the project every success and failure along the way. Cardano will of course eventually have to create real economic value, or the support spigot will dry up, but “eventually” is a long-time from now. Like AMC and GME -- when the pressure of cash flows and default goes away, the option value increases.

In traditional debt and equity markets, this would be most analogous to project finance deals. Often, the hype around a new project is too much, but the hype will quickly be replaced by substance, for good or for worse. Almost every launch leads to prices going down, as the anticipation of the casino, hotel, shopping mall, etc is often greater than the actual product itself. I remember going to the soft-opening of the Revel Casino in Atlantic City in 2012 after $2.4 billion in debt and equity was poured into the buildout of the massive casino. The property looked amazing; functionality however it was a disaster (wrong layout, no customer loyalty, bad management, etc). Morgan Stanley literally walked away from their $932 million in equity. Creditors kept pouring money in to save the project, which filed for bankruptcy twice in the next 2 years. Ultimately, the $2.4 billion investment was sold for $110 million. It was an unmitigated disaster for investors, with a quick and painful death. And yet, had Revel been financed by a digital asset, the casino may have never needed to open, and would likely still have a multi-billion dollar valuation. There would be people all over the world who “reveled” in the idea of the casino project. The cash-flows would be irrelevant for decades, and the hope of future success would buoy the project.

Just this past week, I was asked if Illuvium (which is not yet a live, working, playable game) had the potential to compete with Axie Infinity (the most successful game in blockchain’s young history, with over 1 million DAUs, and $4 billion of run-rate revenue). I gave what I thought was a logical response, that the two gaming companies weren’t comparable yet. Over the next 48 hours, I got TORCHED by the community and even the founder of Illuvium himself, for not seeing this amazing and certain future success. The ridicule of my opinion became so much that Arca’s head of investor relations felt compelled to voluntarily offer himself up as a defense witness at my virtual stoning. The ILV token came to market late last year at $3/token. It currently trades at $563/token. There is a passionate, and now very wealthy community that will fight to the death in favor of this project, even if the game ends up being a flop (or never even launches). Ironically, in some of Arca’s funds, we own a position in ILV, and we are huge advocates and investors of both NFTs and gaming projects -- we’re very aligned with the community and the founder, but I made the fatal flaw of challenging “what currently is'' instead of optimistically looking at “what could be”, and I paid the social price. Another large, well-known, well-respected fund manager recently made an off-the-cuff comment about Axie Infinity -- similar result, torched by the community. Now, we’re still big believers in fundamentals, as frequent readers and Arca investors know very well. Eventually fundamentals matter, and projects that show real tangible success will outperform those that don’t. But “eventually” is a very long, undefined time from now, and those that underperform direct comps may still outperform every other asset class. Even those of us who have dedicated our lives and careers to investing in digital assets are still sometimes the bad guys for underestimating this community fervor, becoming lightning rods for “nobody believes in us” rebellion. There’s a reason that we often say “Digital assets are the greatest capital formation AND customer bootstrapping mechanism we have ever seen.”

Digital assets have spawned the most passionate believers in projects, who are growing their wealth and clout alongside the projects that they finance. AMC and GME may both become real companies again, as their investors have given them time and money to pull off the impossible resurrection. The same is true for nearly every digital asset project that empowered their users and communities from day 1. Conversely, Coinbase and Robinhood sold stock to financial mercenaries AFTER massive gains were already realized by insiders instead of given away the upside to customers early on… it’s no surprise that COIN and HOOD aren’t trading nearly as well as tokens of digital asset projects that were largely given away to customers and future users. They failed to achieve the same alignment and community passion.

No one has financial models yet that can effectively value what these communities are worth… but it is clear that they are worth more than the market once thought possible.

What’s Driving Token Prices?

- FTX (FTT) jumped +33% after FTX.US acquired LedgerX. Based on a previous interview with Business Insider last month, FTX.US is looking to provide derivatives by the end of the year, and this acquisition is aimed towards acquiring licenses to accomplish this goal.

- Helium (HNT) rose 14% after Helium's 5G partner FreedomFi announced that 5G network hotspots would start shipping at the end of September, a positive catalyst for more revenue going to the network and could announce partnerships with mobile carriers before the 5G network starts to be deployed.

- Terra Luna (LUNA) only gained 6%, underperforming the rest of Layer 1 blockchains, as the Terra ecosystem TVL growth slowed down this week and was ~flat WoW at $7.5 billion, after showing rapid growth over the month prior. The LUNA token’s chain upgrade was pushed back a few weeks to October.

- Sushiswap (SUSHI) gained 22% following strong WoW volumes growth of +19.42%. Sushiswap launched on Arbitrum, the L2 scaling solution, and released the Shoyu website indicating the NFT marketplace should be live soon.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - PM, Special Situations

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

Kyle Doane- Trader Operations Associate

Nick Hotz- Analyst

Andrew Stein- VP of Research

To learn more or talk to us about investing in digital assets and cryptocurrency