What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

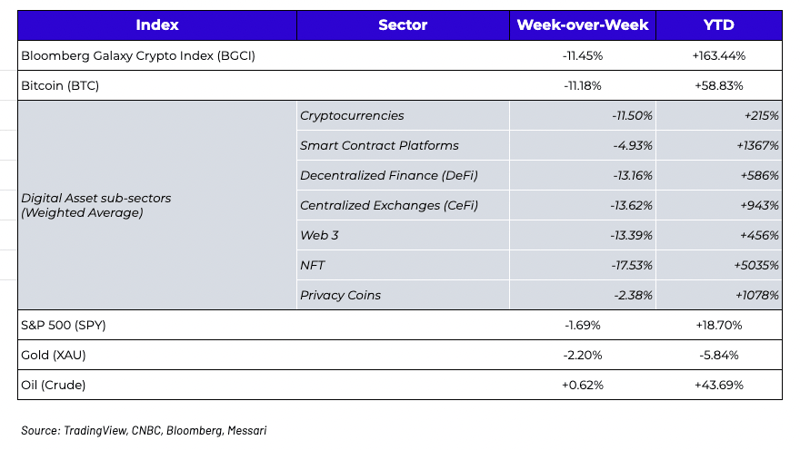

Week-over-Week Price Changes (as of Sunday, 9/12/21)

A wild market flush, but green shoots everywhere

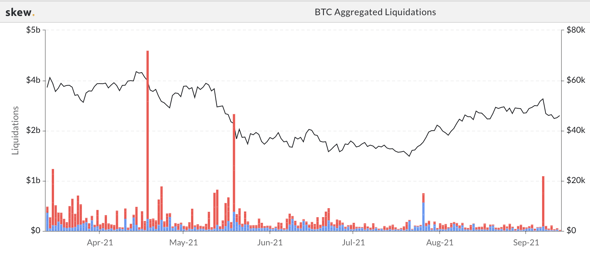

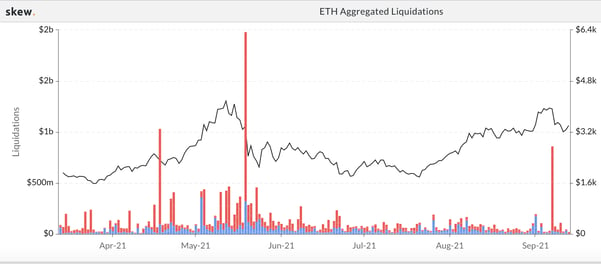

As has been the case in eight out of nine months so far this year, digital assets began the month with a rally, likely driven by institutional inflows. But the September rally quickly faded on Tuesday with an all-too-common occurrence… a leveraged-induced, fast and furious, liquidation-driven selloff. At this point, this isn’t much of a story. Just about every digital asset participant now has the data to see when leverage is building in the system -- the spot/futures basis widens, funding rates turn positive, skew turns negative, sentiment turns increasingly bullish, and lending rates rise. When this happens, a sudden reversal is just a question of “when”, not “if”. The graphs below show Bitcoin and Ethereum liquidations, though you’d see a similar looking chart regardless of which asset you choose. Total liquidations across all digital assets reached over $3.5 billion in just over an hour.

While the liquidations themselves perhaps aren’t all that noteworthy, the market reaction following Tuesday’s selloff most certainly was.

BTC & ETH Futures Liquidations (Red = Longs liquidated / Blue = Shorts Liquidated)

Source: Skew

First, Tuesday’s selloff happened in a completely isolated vacuum. On the same day that many digital assets fell 20-40% peak-to-trough, very little happened elsewhere across global markets.

- Coinbase stock (COIN) fell moderately, while Galaxy (GLXY), Hut 8 (HUT), Canaan (CAN) and other “crypto stocks” were all largely unchanged.

- GME, AMC and other meme stocks were not impacted

- Oil and gold fell just 1-2%

- The US Dollar was marginally higher

- The VIX gained +9% but remained near YTD lows and within a tight 4-month range

- US Equities were unchanged

- Treasury yields were modestly higher

However, a few days later, we began to see cracks in other risk assets, indicating that digital assets may be acting as a “risk on/off leading indicator.”

Second, while we saw high correlations amongst digital assets on Tuesday during the market rout, we saw even greater return dispersion throughout the rest of the week. By week-end, almost half the market had gained +10-30% (Layer 1 protocols, SOL/FTT and its surrounding ecosystem) while the other half of the market declined -10-30% (Bitcoin, ETH and ETH-based DeFi, Gaming/NFT tokens). Not only was the rally impressive for those tokens that bucked the weaker trend, but it was encouraging to see tokens ultimately trade based on information, fund flows, and fundamental improvements rather than just student-body left structural declines. Last week was a good reminder that digital assets are now a complex, alpha-driven asset class.

The SEC, the Fed and the Looming Fight

The Tweet heard around the world came from Brian Armstrong, CEO of Coinbase, calling out the SEC for not engaging in a constructive dialogue with the company and falling short on their obligations to provide regulatory clarity. This came after the SEC issued a Wells notice to Coinbase, which means there was already a violation and that the SEC is now giving Coinbase one last chance to defend itself before enforcement action is brought. Coinbase appears to be going on the offensive rather than backing down. To our knowledge, all Coinbase has done so far is announce a future product offering, and create a waitlist for it -- which means the SEC may be operating here without due process. But independent of any future wrongdoing, or interpretation of the SEC’s actions, there is an interesting and developing subplot that doesn’t seem likely to end any time soon. Investors and builders in digital assets are openly and aggressively calling out hypocrisy and potential wrongdoing by politicians and regulators.

At traditional financial firms, compliance and legal officers take every measure possible to avoid ending up in the Wall Street Journal. They are taught to say no first to avoid bad press, rather than try to create solutions that may be controversial or lead to operating in legal grey areas. Every employee at traditional banks, brokerage firms and asset management firms go through extensive compliance and legal training to ensure that they don’t misstep, or poke the bear. The fear of the SEC and other regulators is instilled from the onset of a traditional finance career.

But most digital asset firms were built by FinTech executives, which have a reputation for “work fast and break things”... an approach that to date hasn’t been very effective in regulated finance. And most digital asset participants are retail investors, which often includes high net worth celebrities with loud and public voices on social media. While there have always been disagreements between regulators and those being regulated, the digital assets industry is the first in recent memory to openly, publicly and frequently call out regulators for hypocrisy and wrongdoings. And this attitude is not limited to digital assets and the SEC - we are seeing more and more aggressive and public stances against banks, brokerages, money transfer companies, the Federal Reserve, Congress, and every large, legacy institution supposedly “safe-guarding” our financial system. In just the last few weeks alone:

The examples go on and on. In fact, I categorize topics that may impact our investing decisions at Arca, or may create good discussions in future weekly blogs, and one category in my notes is titled “Fed and the SEC.” For me to even have a category for this shows how often it comes up these days, and how relevant it probably is to the future of this asset class.

As we’ve stated in the past, most people we know are not anti-government or anti-regulators. Most of us want to see improvements, and are willing to work with regulators to achieve this. Similarly, most regulators we speak to are doing their jobs exactly as you’d want them to do -- they are educating themselves, speaking to industry participants, and are trying to figure out what parts of this ecosystem are already adequately covered by existing frameworks versus which parts need entirely new frameworks altogether. They seem to be taking their time to ensure that they don’t get it wrong or hastily rush out policies that will be too restrictive, or obsolete.

But this methodical slow-playing has consequences too, as it leads to unrest. The digital assets industry keeps growing, leading to more political lobbying efforts and rising legal coffers with which to fight. These efforts to fight/determine regulation are going to be made out in the open, where companies are hoping the court of public appeal will likely prove more influential than judicial courts.

What’s Driving Token Prices?

- Terra Luna (LUNA) gained +22% as the Terra ecosystem continued preparations for the Columbus 5 upgrade which was delayed last week to September 29th. Additionally, SUNNY, a DeFi aggregator on Solana, added liquidity pools for wrapped LUNA and UST, both positive for LUNA demand given the significant TVL growth and adoption of the Solana ecosystem over the last month.

- Helium (HNT) fell 13% despite Helium's fee revenue from underlying network usage continuing to steadily build while the frontend Console for deploying devices on the network, phone app for network providers mining HNT, and Validators securing the blockchain all received compatibility updates in preparation for Helium's second 5G network launching at the end of the month.

- FTX (FTT) gained 7% after Steph Curry of the Golden State Warriors partnered with them lastweek. Additionally, FTX kicked off a $20mm advertising campaign starring Tom Brady and Gisele Bundchen which played during the opening NFL game on Thursday. FTX's ADV was down -19.20% WoW due to the decrease in derivatives volumes after the leverage unwind lastTuesday.

- Sushiswap (SUSHI) fell 16% despite a strong week in terms of volumes (+34.37%) and had its highest volume day of the quarter on Tuesday. Shoyu's release is the next large catalyst for SUSHI and is expected to be released in the next two weeks.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - PM, Special Situations

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

Kyle Doane- Trader Operations Associate

Nick Hotz- Analyst

Andrew Stein- VP of Research

To learn more or talk to us about investing in digital assets and cryptocurrency