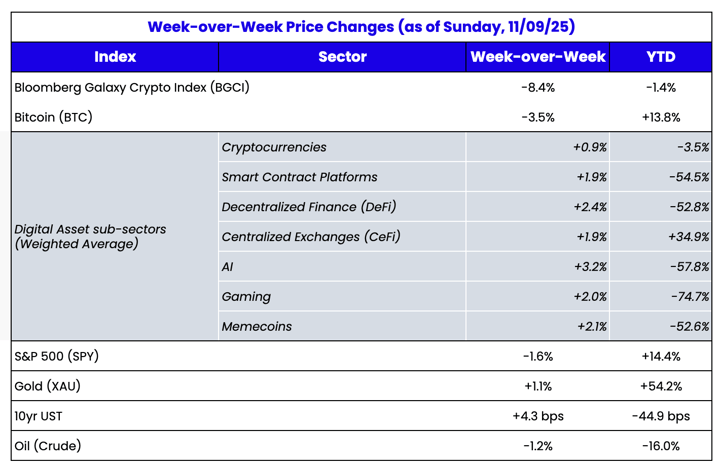

Source: TradingView, CNBC, Bloomberg, Messari

This week’s edition was written by David Nage, Portfolio Manager at Arca

Act I: The TGA Buildup (October 1 - October 31)

When the government shut down on October 1st, something unexpected happened in the financial system's operations. While federal spending came to a halt, tax collections continued. Every dollar collected during this period flowed into the Treasury General Account (TGA), the government's checking account at the Federal Reserve.

The mechanism is mechanical and unforgiving:

- Tax payment comes in, which increases TGA by $1

- Bank reserves decrease by $1 (inverse relationship)

- Banks have less liquidity to lend to each other

- Overnight funding markets tighten

By late October, the TGA had surpassed $1 trillion, marking a significant increase in just 4 to 5 weeks. Meanwhile, bank reserves, which were approximately $3.2 trillion at the beginning of October, fell to around $2.8 trillion. Although this may seem like a substantial amount, the Federal Reserve has historically intervened when reserves get close to $2.85 trillion.

(TGA data: U.S. Department of the Treasury (2025), Daily Treasury Statement, November 7 release; Reserve balances data: Federal Reserve Board (2025), H.4.1 Factors Affecting Reserve Balances, November 6 release)

Act II: The Late October Repo Crisis (October 27 - November 3)

The stress in the repo market became evident, particularly in the overnight lending market where banks and financial institutions borrow against Treasury collateral. On November 3rd, the usage of the Fed's Standing Repo Facility (SRF) surged from typical levels of $2-5 billion to nearly $50 billion.

Additionally, the Secured Overnight Financing Rate (SOFR), which serves as a benchmark for trillions in loans and derivatives, rose to 4.36%, exceeding the Fed's target ceiling of 4.25%. Spreads also widened to 36 basis points above the Federal Funds rate, indicating funding stress in the market.

In response, Fed Chair Jerome Powell announced on October 30th the end of Quantitative Tightening (QT), effective December 1st. During his press conference, he explicitly acknowledged the stress in the repo market, conveying a clear message: the Fed was monitoring the situation and would take action if necessary.

Act III: The Resolution (November 4 - Present)

As quickly as it appeared, the stress evaporated. By November 7th, usage of the SRF had dropped back to nearly zero. SOFR fell to approximately 3.90%, dipping below the Federal Funds target range and signaling abundant liquidity. The crisis in the repo market was over.

What led to this turnaround?

The communication from Fed Chair Jerome Powell proved more influential than the mechanical policy changes. By explicitly acknowledging market stress and outlining a framework for responding to it, Powell helped markets adjust. Banks began to realize that the Federal Reserve was supportive, leading to a decrease in emergency borrowing and a return to normal market functioning.

Meanwhile, the TGA continues to grow, currently hovering around $1 trillion. However, market participants now understand that the Fed is closely monitoring the situation and is willing to navigate through the stress until the shutdown concludes.

The Coming Liquidity Injection: Why Shutdown Resolution Could Be Bullish

This is where things become interesting for risk assets, including digital assets. When the government shutdown concludes (whether that happens next week, next month, or in December), the TGA will be drained. Federal spending will resume, and the approximately $1 trillion currently held in the Treasury's account will re-enter the economy.

The mechanism reverses:

- Government pays contractor → TGA decreases

- Contractor's bank receives deposit → Bank reserves increase

- More liquidity in the banking system

- Easier funding conditions → risk-on behavior

Treasury Secretary Scott Bessent and his team are expected to quickly spend down the TGA once operations resume. There is no reason to hold onto excess cash at that point. A reasonable estimate suggests that $150 to $200 billion could flow back into bank reserves within the first few weeks after reopening.

Historical Pattern: Reserve Injections Drive Risk Assets

We've seen this movie before, and it tends to end well for risk assets:

March 2020: After the Federal Reserve injected massive reserves through QE, the S&P 500 reached its bottom and began a historic rally. Concurrently, Bitcoin surged from $5,000 to over $60,000 within the next year.

September 2019:The Fed resumed repo operations and expanded its balance sheet, leading to a rally in both equities and crypto as the year ended.

January 2023: The TGA drawdown from debt ceiling negotiations injected approximately $400 billion into reserves, and simultaneously, Bitcoin rallied from $17,000 to over $30,000 in the first quarter.

The pattern is clear: when bank reserves increase, especially after a period of stress or decline, financial conditions improve, and risk assets tend to perform well. More liquidity chasing a similar amount of assets usually drives prices higher.

In particular, digital assets have historically been sensitive to liquidity conditions. The bull market from 2020-2021 occurred alongside unprecedented reserve expansion, while the bear market in 2022 took place during quantitative tightening (QT) and reserve contraction. The rally in 2023 began when the TGA drawdown reversed some of the QT effects.

However, an estimated $150 billion to $200 billion in reserve injections alone is unlikely to spark a Bitcoin rally, as many factors are at play. However, it could alleviate some existing pressures and potentially create favorable conditions, especially if it aligns with other positive developments.

The Legislative Casualty: CLARITY Act Momentum Stalling

While markets focused on repo rates and TGA levels, a more significant issue was quietly developing in Washington: the push for comprehensive digital asset legislation was losing momentum.

Where We Were: Digital Assets Regulation Pre-Shutdown

The CLARITY Act, which aims to create a clear regulatory framework that distinguishes digital commodities from securities and establishes CFTC jurisdiction over most crypto assets, passed the House in July 2025 with strong bipartisan support, receiving a vote of 279-136. This is not a narrow partisan vote; it reflects a clear mandate.

Senator Tim Scott, the ranking member of the Senate Banking Committee, has been working on complementary market structure legislation. While the Senate's approach varies in some specifics from the House bill, the frameworks are compatible. Industry observers and policy analysts anticipate conference committee negotiations in November, with a realistic path to passage before the end of the year.

The political climate is favorable for several reasons:

- Both parties are eager to demonstrate their ability to govern and pass significant legislation.

- Digital assets have become a genuine bipartisan issue, with advocates from both parties.

- The industry has united around reasonable frameworks, reducing lobbying conflicts.

- Regulatory clarity would benefit both traditional finance entering the crypto space and crypto-native firms.

- Most importantly, the legislative calendar is clear, as there are no major elections until November 2026, allowing legislators the political space to address complex policy issues.

Where We Are Now: Day 39 of Shutdown

Momentum has hit a wall.

The Senate Banking Committee hearings that were scheduled for early November have been postponed indefinitely. Staff members who were working on legislative text and conference committee preparations have been furloughed. As a result, timelines for floor votes and final passage have become meaningless.

On November 7th, Democrats proposed what they called a compromise: they would agree to pass a one-year extension of enhanced Affordable Care Act subsidies in exchange for reopening the government. However, Republicans immediately rejected the proposal, labeling it a "nonstarter." Senator Lindsey Graham described it as "political terrorism," and Senator John Thune stated that it doesn't "get anywhere close" to what is needed.

In other words, the government shutdown is likely to continue for the foreseeable future. With each passing day, the window for year-end legislative action becomes smaller.

The 2026 Problem: Why Midterm Elections Kill Legislation

Here's the uncomfortable reality that participants in the digital asset industry need to understand: If comprehensive crypto legislation slips into 2026, it’s likely to be lost.

Why is that? Because of the midterm election dynamics.

In a midterm year, especially one where control of Congress is genuinely contested, legislators become extremely risk-averse. Every vote can become the target of a 30-second attack ad, and every complex bill poses a potential liability.

Digital asset legislation, no matter how well-crafted or bipartisan, involves a level of technical complexity that can be easily mischaracterized. For example, critics might claim:

- “Senator X voted to help crypto scammers avoid regulation.”

- “Representative Y sided with Wall Street over Main Street.”

- “They want to legalize money laundering for drug cartels.”

None of these statements would accurately characterize the CLARITY Act or Senator Scott’s framework, but accuracy doesn’t matter in attack ads.

Furthermore, 2026 presents additional structural challenges:

- Committee composition changes: Members will focus on reelection rather than legislating. Leadership bandwidth: Floor time will be dominated by messaging bills aimed at energizing base voters.

- Lame-duck risk: If control of Congress flips, the post-election session may become chaotic.

- Presidential politics: Candidates positioning for 2028 might oppose bills to differentiate themselves.

The window for substantive, complex, bipartisan legislation is 2025, specifically within the next 6-8 weeks before the holiday recess. Unfortunately, the government shutdown is consuming that valuable time.

What Senator Scott's Team Has Been Working On

Based on discussions with Senator Scott's office and public statements from the Banking Committee, the Senate's approach to regulating digital assets prioritizes clarity in market structure while addressing legitimate regulatory concerns.

Key elements of the Senate framework include:

- Functional Definitions: Establishing clear criteria to differentiate between digital assets that are considered commodities and those classified as securities, focusing on actual usage and network characteristics rather than their origin.

- Transition Mechanisms: Creating pathways for digital assets to shift from being treated as securities to commodities as their networks become more decentralized.

- Jurisdictional Clarity: Assigning the Commodity Futures Trading Commission (CFTC) as the primary regulator for commodity digital assets, while the Securities and Exchange Commission (SEC) retains authority over securities.

- Custody Standards: Developing a framework that allows banks and broker-dealers to hold digital assets for their clients safely.

- Stablecoin Provisions: Coordinating with the House-passed GENIUS Act on regulations concerning payment stablecoins.

While the Senate's approach differs from the House's CLARITY Act in some technical aspects, especially regarding timeline requirements and disclosure obligations, the two frameworks are fundamentally compatible. A conference committee could reconcile these differences relatively easily.

Why This Matters More Than Most Realize

Regulatory clarity isn’t merely about satisfying lawyers; it’s essential for unlocking capital and fostering innovation that is currently stagnant.

Consider the potential outcomes if the bill passes:

- Institutional Custody: Banks that are currently hesitant to offer crypto custody due to regulatory uncertainty could start providing these services.

- DeFi Protocols: Projects would gain a clear understanding of applicable regulations and could structure their compliance accordingly.

- Venture Capital: Venture capitalists could invest in token structures without facing significant regulatory risks.

- Public Companies: A clearer accounting framework would facilitate corporate treasury adoption of digital assets.

- Retirement Accounts: 401(k) providers could offer cryptocurrency exposure with regulatory assurance.

Each of these developments has the potential to unlock tens or even hundreds of billions of dollars in capital that is presently sidelined—not speculative retail capital, but institutional capital managed by fiduciaries who require regulatory clarity before making investments.

Conversely, if the bill fails, the status quo will remain. This would lead to ongoing jurisdictional disputes between the SEC and CFTC, enforcement through press releases, and entrepreneurs relocating to countries like Dubai, Singapore, and London. As a result, capital would flow offshore, putting U.S. companies at a competitive disadvantage.

The shutdown is not merely delaying a bill; it could jeopardize the global competitiveness of the U.S. digital asset industry.

The Irony: Crisis Creates Opportunity, But Also Risks.

Let's connect the dots.

The government shutdown has created two parallel effects:

- A Coming Liquidity Catalyst: When the shutdown ends, $150-200 billion will flow from the Treasury General Account (TGA) back to bank reserves. This will ease financial conditions and has historically supported risk assets, including cryptocurrencies.

- A Legislative Roadblock: The CLARITY Act and the Senate market structure bill are losing valuable time, which could delay them into the 2026 midterm elections. At that point, passage of these bills would become extremely unlikely.

We have a potential short-term positive (liquidity injection) being undermined by a medium-term negative (legislative failure).

The ideal outcome—still achievable—would be a resolution to the shutdown in November. This would enable:

- TGA Drawdown → Reserve Injection → Easier Financial Conditions

- Congress is returning and scrambling to demonstrate its ability to govern, leading to much-needed bipartisan wins.

- Digital asset legislation is becoming the perfect vehicle, as it already has bipartisan support from the industry.

- A conference committee resolving the differences between the House and Senate in December.

- The bill is passing before the holiday recess, achieving regulatory clarity.

This optimistic scenario combines a liquidity injection with legislative clarity, both arriving in Q4 2025 or Q1 2026.

In contrast, the pessimistic scenario involves the shutdown dragging into December. This would close the year-end legislative window, delaying the bill to 2026. Midterm election dynamics could kill it, delaying regulatory clarity by another 2-4 years while other countries move ahead.

The outcome we experience largely depends on the next 3-4 weeks.

What to Watch Out For

Near-Term (Next 2 Weeks):

- Shutdown negotiation dynamics: Is there any movement beyond the current ACA stalemate?

- TGA balance: Is it continuing to grow, or is it plateauing?

- November 21st deadline: The House's original stopgap Continuing Resolution (CR) expires; this is largely symbolic but creates a sense of urgency.

Medium-Term (Through Year-End):

- When the shutdown ends, what will be the pace and magnitude of the TGA drawdown?

- Reserve levels: Will we see the injection translate into easier conditions?

- Congressional calendar: How many legislative days remain before the holiday recess?

- Senator Scott's Banking Committee: Are there any indications regarding the timeline for hearings or markups?

Longer-Term (Into 2026):

- If the bill doesn’t pass by year-end, will the momentum carry into 2026?

- Midterm election positioning: Will cryptocurrency become a partisan issue?

- Regulatory developments: Will the ambiguity between the SEC and CFTC persist?

Conclusion

The government shutdown is teaching us a vital lesson about digital assets: while short-term market dynamics are important, long-term regulatory clarity is even more crucial.

The repo crisis that occurred in late October garnered significant headlines and caught the attention of traders. Concepts like SOFR spreads, SRF usage, and TGA balances are all critical, but the crisis resolved itself within days once the Federal Reserve communicated its backstop.

In contrast, the ongoing legislative delay is quieter, less dramatic, and more difficult to track on a Bloomberg terminal. However, its effects could last for years rather than just days. If comprehensive digital asset legislation is delayed until 2026 and then dies in midterm politics, the industry will miss out on the regulatory clarity needed to attract institutional capital and achieve sustainable growth.

The next few weeks will be telling:

- If the shutdown ends in November, we may benefit from both a liquidity injection and a legislative opportunity. This is the best-case scenario, providing easier financial conditions alongside regulatory clarity, both arriving in Q4 or Q1.

- If the shutdown extends into December, we’ll still see a liquidity injection, but we will likely lose the chance for legislative progress. This is the mediocre scenario: short-term benefits tempered by medium-term challenges.

- If the shutdown continues indefinitely, we risk losing both opportunities, and 2026 might turn into a lost year for cryptocurrency policy. This is the scenario we must avoid.

While markets are focused on Bitcoin price movements and macro liquidity trends — and understandably so — the larger story for digital asset adoption over the next 3-5 years is being shaped behind the scenes in Senator Scott's office and the Banking Committee staff rooms, which are currently dark due to the shutdown.

It's essential to keep an eye on Washington, not just on the Federal Reserve, but also on Congress. The decisions made in the coming month could determine whether 2026 becomes the year for clarifying U.S. digital asset regulation or simply a year postponed due to election cycles.