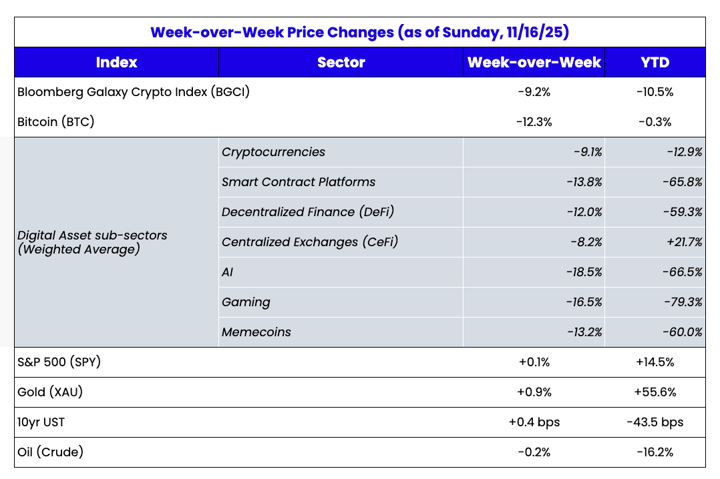

Source: TradingView, CNBC, Bloomberg, Messari

Showcasing the Disconnect Between Fundamentals and Price

There are only 3 areas in crypto that are consistently growing: Stablecoins, DeFi, and RWAs. And these sectors are not just growing, they are exploding.

Look at the charts below:

Stablecoin growth (and you can see even more growth here):

DeFi growth (and you can see even more here and here and here):

RWA growth (and you can see even more here):

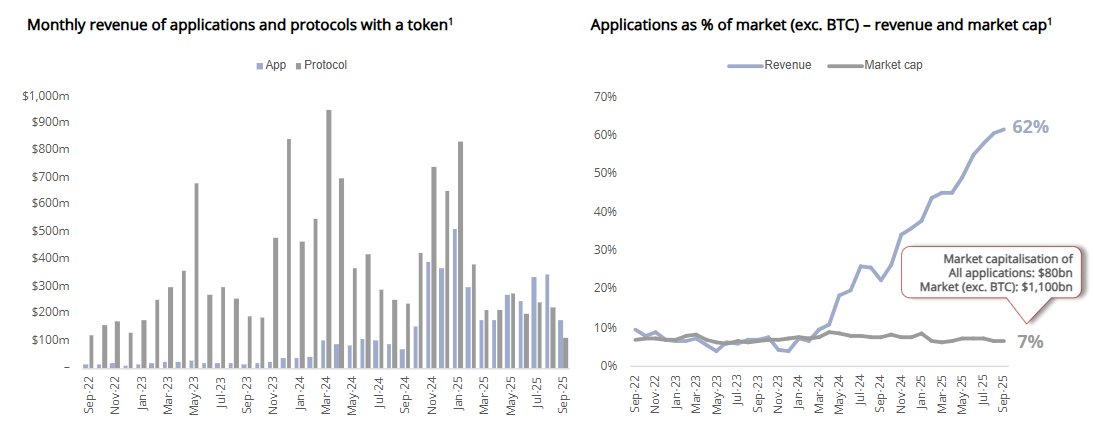

These are the applications crypto should be known for. These are the types of charts that should be on CNBC, in the Wall Street Journal, in Wall Street research reports, and highlighted on every crypto exchange and crypto pricing page. Any objective growth investor would look at the data on stablecoin AUM and transaction growth, RWA growth, and DeFi growth and wonder, "How do I invest in that?" Each of these industries is showing "up and to the right" growth, and with the exception of stablecoins, they are all easily investable via tokens (e.g. HYPE, UNI, AAVE, AERO, SYRUP, PUMP, etc). These decentralized applications (dApps) now make up approximately 60%+ of crypto’s total revenue, yet the underlying tokens of these apps make up only 7% of the total crypto market cap. Read that again. That’s insanity.

And yet, the media and exchanges continue to focus only on Bitcoin and memecoins. The majority of investors still associate crypto with BTC, Layer-1 protocols (like ETH, SOL and AVAX), and memecoins. The market has clearly shifted towards revenues and profits, yet most can’t fathom that tokens are really good vehicles for value capture and profit distribution.

Our industry has failed to attract fundamental investors who appreciate growth equity stories with high cash flows and metrics that are up and to the right, even though this buyer base is the largest and most important investor group globally. Instead, for some unknown reason, this industry continues to cater to the tiniest and most irrelevant investor population (tech VCs and fast money macro/CTA funds).

Worse, many continue to think that investing in stocks gives you some sort of legal claim to the company’s cash flows, whereas you don’t have any ownership via tokens. I’ve been pointing out the hypocrisy between equity investors and crypto investors for over 6 years. Have you ever, as a shareholder in a company, dictated how that company spends its cash? Of course not. You have no control over how much they pay their employees, how much they spend on R&D, whether they make an acquisition, or whether they do a buyback or pay a dividend. That is entirely up to management. The only actual legal rights or protections you have as a shareholder are:

- You are entitled to be paid if the company is sold (very important)

- You are entitled to the leftover assets in a bankruptcy net of debt (almost always irrelevant since debt holders typically get all of the post-reorg equity and shareholders get very little, if anything)

- You have the right to join a proxy fight to join the board of directors and overthrow management (but this is also true in crypto – Arca has led 3 token activist campaigns in the last 8 years to force change at certain crypto companies versus Gnosis, Aragon and Anchor).

At the end of the day, you, as a shareholder, are at the mercy of management’s decisions on how they use those cash flows. And that is no different from being a tokenholder at the mercy of management over whether they do buybacks. The fact is, outside of an acquisition, it doesn’t matter if you own a stock or a token – you are at the mercy of management’s decisions on how they utilize the company’s cash flows.

Hyperliquid (HYPE) and Pump.Fun (PUMP) have demonstrated the market appeal of real yield and burn-based value capture, and many established projects, such as Aave, Raydium, and PancakeSwap, have integrated similar mechanisms. Uniswap (UNI) made news this past week for finally turning on the fee switch, giving UNI holders a piece of the protocol's revenue. Again, the market is shifting. In 2025 alone, crypto protocols and companies have conducted more than $1.5 billion in token buybacks, with 10 tokens accounting for 92% of token buybacks (though we think the ZRO data in this article is wrong, and HYPE and PUMP have bought back much more than what is shown in this data).

To put that in context, the entire liquid crypto market cap (excluding Bitcoin and stablecoins) is only $1 trillion. So that’s a buyback percentage of 0.15%. If you just look at the market caps of the largest issuers of buybacks, the buyback percentages for those tokens can be as high as 10% of the market cap. In the U.S. stock market, it is estimated that companies have bought back roughly $1 trillion in stock this year, which is roughly 1.5% of the $67 trillion market.

This disconnect between how people think about crypto investing and value capture, versus what is actually happening, is quite large. You could certainly argue that most tokens are completely uninvestable, but it is also true that the best tokens are completely undervalued, and probably weighed down by the worst assets. As a result, in many cases, growth and revenues are up and to the right, while token prices are down and to the right. Many of the top tokens in the 3 fastest-growing sectors, which have accounted for the most revenue and buybacks, have performed horribly.

Source: Arca internal calculations / Coingecko

So the question remains: why aren’t more industry leaders in crypto focused on promoting the areas of crypto that are actually growing? Shouldn’t this industry be showcasing the tokens in these sectors, with the best tokenomics, and explaining to investors how to invest in them? Investors need to understand that there is actual logic and fundamentals behind investing in crypto in order to bother doing research on these investments. If we want good tokens to start outperforming bad tokens, we have to start teaching people what the good tokens are.

A few years ago, virtually no product generated meaningful revenue. Today, many do, and many use a very high percentage of that revenue for buybacks (sometimes as much as 99% of revenue), and many trade at incredibly cheap prices compared to other stocks. In fact, these tokens are essentially stocks, but without the educated, persistent buyer base.

So where would these assets trade if they actually were stocks? Where would they trade if investors understood how these revenue-producing buyback tokens differ from “cryptocurrencies” and “smart contract protocols?”

Let’s use the two best examples in the market to illustrate.

Hyperliquid (HYPE) and Pumpfun (PUMP)

Hyperliquid is the leading decentralized perpetual futures exchange. Just about every metric shows how fast and how consistently this company is growing.

Volumes:

Source: Artemis

Fees:

Source: Artemis

As a result of the growth in volumes and fees, Hyperliquid is one of the cheapest tokens using traditional valuation models. HYPE is annualizing $1.28B in revenue (based on the last 90 days), and it trades at a P/E of 16.40x with 110% YoY growth. It is also using 99% of revenues to buy back the token, and at this rate, it has already bought back over 10% of the circulating float (HYPE has bought back $1.36 billion of HYPE tokens). That is one of the most successful stories in history, not just crypto history.

Source: Arca Internal Calculations

For comparison, the S&P 500 trades at roughly 24x and the Nasdaq trades at 27x. Coinbase trades at around 25x P/E. Robinhood (HOOD) trades at about 50x P/E, and only does about 2x the earnings as HYPE (~$2B vs HYPE at $1B).

- HYPE has grown faster YTD (110% vs 65%)

- Hyperliquid is also a Layer-1 protocol, which isn’t yet priced in. The market still treats HYPE as nothing more than an exchange.

- Every dollar earned is distributed to holders through buybacks, whereas HOOD has no buybacks or dividends.

Source: Arca Internal Calculations

So that either means the market expects Hyperliquid’s growth to slow significantly and for it to lose market share, or it means the market is missing something. There are valid reasons why HYPE trades at lower multiples than HOOD: the token is only a year old and faces strong competition, with digital assets typically having little to no moats. But HOOD trading at a 5x higher P/E ratio while growing more slowly and showing lower profit margins seems exaggerated and is more likely due to the buyer base than the assets. Stock investors are just more educated than crypto investors.

In any other industry, if you saw a chart like the one below, where price is going down while earnings are going up, you’d be putting every dollar you had into this investment.

Now let’s look at Pumpfun (PUMP). Like Hyperliquid, this is a simple business. Pumpfun helps token issuers launch tokens, and earns a fee on both the launch and the trading of these tokens post-launch.

Once again, it’s one of the most successful stories in crypto history, with trailing revenue already north of $1 billion.

Source: Blockworks

The PUMP token was ICO’d earlier this year at $0.004, and while the max supply is 1 trillion tokens, only 590 billion are currently circulating. In under 4 months, Pumpfun has already repurchased 3.97 billion PUMP tokens, and it also allocates 99% of its revenues for buyback tokens. Using adjusted market cap, PUMP trades at 6.18x earnings (and all earnings are used for buybacks).

Source: Blockworks

Quite frankly, we’ve never seen any companies grow as fast as Pump.Fun and Hyperliquid, and certainly none that have dedicated so much of their free cash flow to repaying their investors. These are the most successful stories in investing history, and the best tokens in crypto history.

If these were stocks, they’d be trading 10x higher, if not more. But alas, the investor base isn’t here yet. So those who recognize this value will wait. The assets aren’t the problem. The mechanisms for value transfer aren’t the problem.

Education is a major problem.

If you would to coordinate an educational session, please reach out to

ir@ar.ca.

.png?width=738&height=264&name=unnamed%20(7).png)

.png?width=610&height=224&name=unnamed%20(8).png)

.png?width=632&height=368&name=unnamed%20(9).png)