What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 12/20/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+22%

|

+225%

|

|

Bloomberg Galaxy Crypto Index

|

+18%

|

+250%

|

|

S&P 500

|

+1.2%

|

+14.5%

|

|

Gold (XAU)

|

+1.5%

|

+23%

|

|

Oil (Brent)

|

+5.5%

|

-20%

|

Source: TradingView, CNBC, Bloomberg

The Everything Rally Marches On

Stocks edged higher last week, with all major U.S. indexes hitting fresh all-time highs ahead of Congress finally agreeing to an unnecessarily delayed $900 billion stimulus bill. Oil logged its seventh straight weekly gain, reaching a new post-March high despite being one of the few asset classes that remains lower year-to-date, perhaps giving a more accurate picture of the true state of the economic recovery. Long-bonds drifted lower, but still remain +7% YTD. Gold inched higher, and is once again in striking distance of its all time high. We even saw a Mike Trout rookie card sell earlier this year for $3.93 million, smashing the all-time record, as demand skyrockets for baseball cards and other novelty items that protect against inflation. So naturally, it should surprise no one that Bitcoin also continued its torrid 4Q march higher, finally breaking above its all-time-high, and accelerating another 20% shortly thereafter.

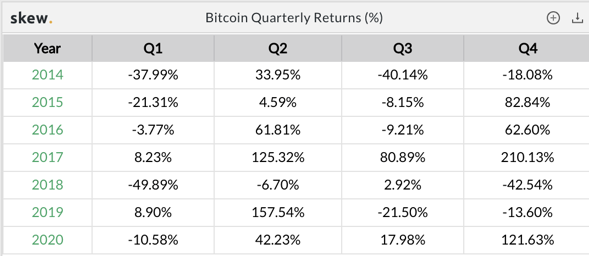

Everywhere you look, there are record highs, and Bitcoin is no exception. It has simply been a phenomenal quarter for what has become a truly global, all-encompassing, macro asset. Bitcoin is having its 4th best quarter since 2014, with two weeks to go. John Street Capital sums up the newfound demand for Bitcoin perfectly.

Source: Skew | Twitter / @johnstcapital

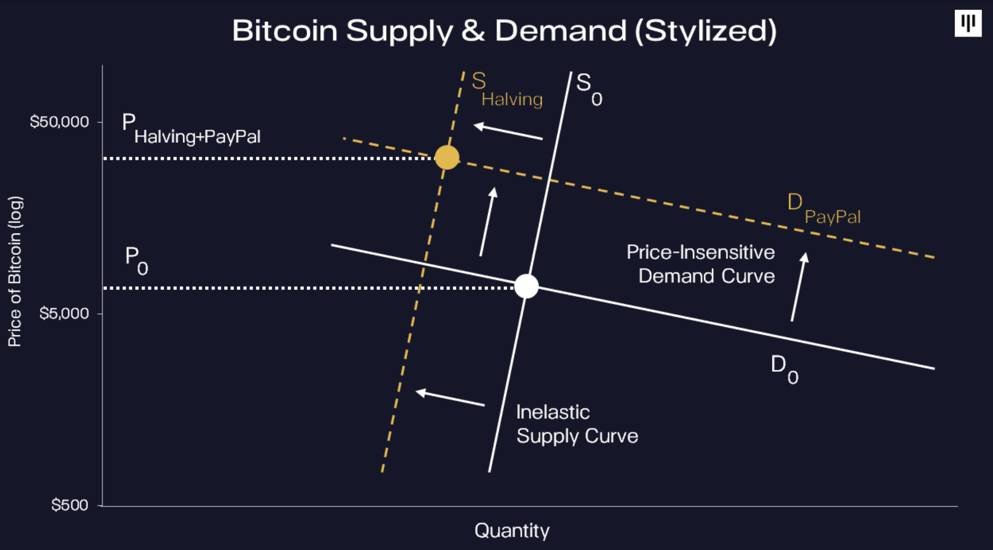

Our friends at Pantera may have put out the single clearest explanation for why Bitcoin demand is outpacing supply

The demand curve seems very price-insensitive. When people want in – like now – price doesn’t seem to have a large impact. On the graph, that yields a fairly flat line. On the flip side, supply seems very inelastic. Many holders of bitcoin hold it more for political/philosophical reasons than for price appreciation. It takes much higher prices to induce them to sell. That makes the supply curve very steep. In the last seven months, we’ve had two huge shifts – one in demand, one in supply – both upwards.

On the demand side, we’ve had public companies like PayPal enter the market. That shifts the demand curve much higher. At the same time, the supply of newly issued bitcoin was cut in half in May – as part of the every-four years Halving of bitcoin issuance. Fewer Bitcoin are available. The price acts like there’s a shortage.

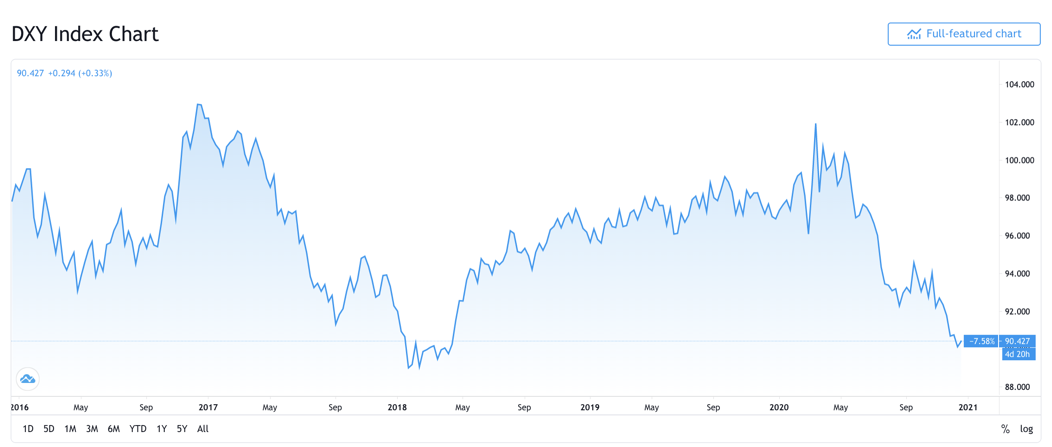

It was only six months ago that strategists were hailing “King Dollar” and voicing their concern over how a strong dollar would hurt the economy. Instead, six months later, the US dollar is near 5-year lows. It’s just hard to envision any assets going lower amidst negative rates, continued government stimulus, and a declining dollar.

That said, if any of these conditions change, it’s also hard to imagine who the incremental buyer is now that most investors are already all in. Fear is gone, which should make one fearful.

Source: TradingView

10 Random Thoughts Heading into 2021

We’ve written a lot about digital assets in 2020. But there is also a lot that we simply didn’t get to this year given how fast this asset class changes and evolves. There is simply too much information to absorb and process on a weekly basis, since digital assets are affected by so many different facets of the economy. This will be our last market recap of 2020, so we're going to mix things up and put down some thoughts that we didn't have time to develop further this year. We’ll be out with our annual 2021 digital assets predictions over the holidays, but until then, happy holidays!

- While the V- or K-shaped recovery marches on, investors are likely underappreciating how many people and industries will be permanently scarred by having to live through this pandemic. As Sam Zell said, “Just as the Depression left behind a generation that couldn’t shake the experience of mass unemployment, hunger and desperation, the burdens this crisis has forced on society may be similarly hard to forget. It won’t be easy for people to live as they did before the “extraordinary shock” of the pandemic. Some amount of social distancing and working from home will persist long after the acute phase of the outbreak is over, possibly for years. Retail, hospitality, travel, live entertainment and professional sports are some of the industries that will continue to struggle.” The digital revolution is just getting started.

- Japan is the only country that has ever avoided default once government debt exceeds GDP by 130%. US debt-to-GDP went above 130% in the 2Q, and is still dangerously high heading into a period of almost certain continued government spending and further GDP declines (at least through this winter). This will not end well.

- I don't know if Bitcoin is going higher or lower (I assume higher), but I do know that a ton of unqualified Wall Street professionals are going to continue to give amazingly inaccurate price predictions with no justification. Wall Street is very consistent -- enter the party late but claim expertise in order to extract low-hanging fruit fees.

- The upcoming Coinbase IPO is exciting, but will further accentuate a problem that already plagues equity market participants who are looking for digital assets exposure. The small handful of publicly traded equities of companies loosely affiliated with Bitcoin are being treated by investors as “Bitcoin tracking stocks”, with insanely high correlations, even if many have very little to do with the success or price of Bitcoin. The Coinbase IPO will be no different, luring investors into the largest “crypto IPO” as a Bitcoin or digital asset surrogate. The most underreported digital assets story of 2020 has been the price gains in small-cap stocks loosely related to Bitcoin, from VYGR to GLXY to HUT, down to even looser relationships like SI and MSTR. “Crypto stocks" have gone wild this year as mom and pop investors are desperate for exposure to this asset class.

- The Bitwise 10 Index, which now trades OTC under the ticker BITW, is yet another disappointing product that preys on retail investors. The “index” is 88% Bitcoin and Ethereum, the two easiest digital assets to purchase directly, yet the index trades at a 230% premium to NAV (down from almost 500% earlier this week). The goal should be to teach investors how to buy digital assets directly, or introduce safe products that are appropriate for them. This is not progress.

- The steep divide between wages and productivity, and the worsening income inequality gap, is going to be the biggest driver of “non-cryptocurrency” digital asset adoption. Digital assets issued by companies matter because they turn product customers into quasi-equity owners. Watching Airbnb and Doordash print hundreds of billions of dollars of gains for a small amount of wealthy investors on the backs of everyday working class people may have been the tipping point.

- COVID-19 did not cause an economic collapse; it merely exposed the fragility of the economy. The last 10 years produced the slowest recovery in history while requiring the highest debt expansion and lowest rates in history. Historically after recessions, debt is greatly reduced which provides a proper financial foundation for positive growth going forward, but instead unproductive debt continues to soar. There is no way out of this mess.

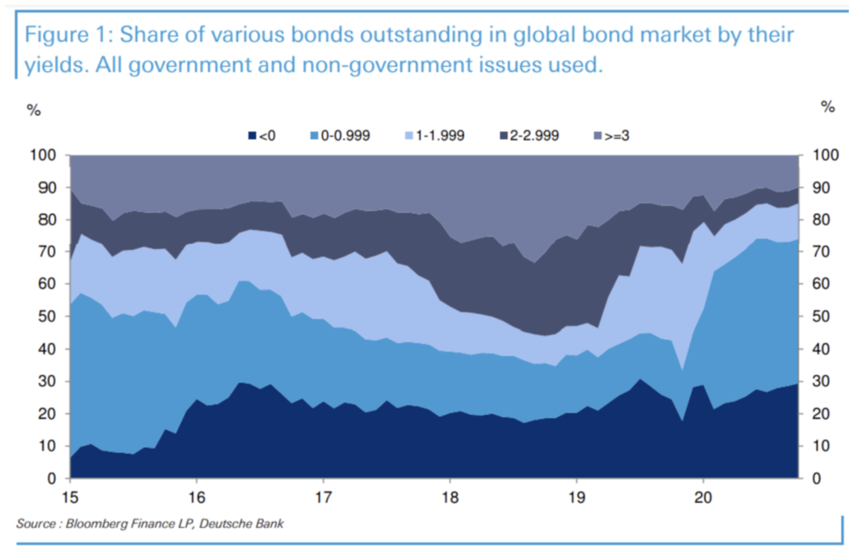

- That said, according to Deutsche Bank, the share of global government and non-government bonds yielding 0-1% has increased from 15.7% of the total to 44.7% now. Fixed Income is a completely dead asset class, and is the primary reason equities and digital assets are going to continue to laugh at economic data and reason for decades to come.

- A standard framework for assessing and valuing pass-thru tokens and asset-backed tokens is coming, and investors will begin to ask themselves questions like: Is the token used for anything? Is it quasi-equity? Is it backed by a real income stream? Is there a yield? Does the company have optionality with regard to enhancing the features? If none of these are true, and you’re left simply talking about “demand being greater than supply”... it’s probably a soon to fail “cryptocurrency” and you should run as far away from it as possible.

- When asked to do a 2020 recap, my mind simply flutters with buzzwords that actually came through this year: institutional adoption, prime broker-like services, the rise of stablecoins, massive derivatives growth, much needed regulatory action, M&A, DeFi, value-accruing tokenomics, successful activism, and NFTs. It is hard to be more bullish on this asset class even after such an amazing year.

What’s Driving Token Prices?

The relationship between Bitcoin and the rest of the market can be broken down into the following sections: the rest of the space lags when Bitcoin goes up rapidly, the rest of the space has high downside beta when Bitcoin goes down rapidly, and the rest of the space generally does well when Bitcoin is stagnant. With Bitcoin breaking through its all time highs this week (and then some, as it finished the week up 22%), most of the space simply did not keep pace. There were still notable assets that warrant attention this week, both from nascent sectors:

- Chiliz (CHZ) has had a remarkable week as the leading sports fan engagement platform in the digital ecosystem. On Monday, they announced that Binance would be launching staking pools for the Juventus (JUV) and Paris Saint-Germain (PSG) tokens, as well as listing them on their Innovation Zone portion of the platform and making a strategic investment in Chiliz. The surge in interest has led to over 20% of CHZ to be locked (via LaunchPool and Locker Room), which has led to a significant price bump in CHZ (+28%), JUV (+103%), and PSG (+71%).

- Axie Infinity (AXS) finished up a successful Land Demo this week (dubbed Project K), where owners of digital land were able to interact with their plots in the beta for 7 days (with an associated Land Design competition). The project is looking to deploy their own sidechain, Ronin, to alleviate some congestion throughout the network, as well as roll out v2 of their turn based battle system. The play-to-earn game model is starting to take hold, with 9M AXS (~$13M) to be distributed in Year 1. Metrics have been increasing at a rapid pace (December Update), and the token has been appreciating just as rapidly: AXS finished the week up 13% after peaking +48%.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency