What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 12/13/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

-0.4%

|

+165%

|

|

Bloomberg Galaxy Crypto Index

|

-4.0%

|

+197%

|

|

S&P 500

|

-1.0%

|

+8%

|

|

Gold (XAU)

|

+0.1%

|

+21%

|

|

Oil (Brent)

|

=0.7%

|

-24%

|

Source: TradingView, CNBC, Bloomberg

Fed Doublespeak, Fixed Income, Insane IPOs and Digital Assets are all related

This may sound like one giant stream of consciousness, but it is all interconnected. Per Edward Jones, the S&P 500 has hit 30 new all-times highs in 2020, 17 of which were recorded after the February pandemic-induced bear market, and four of which were recorded in the last two weeks alone. Why? Corporate profit optimism is a lame excuse, as is the vaccine, since both of these future events are outcomes that were already priced into inflated markets eventually… they just got delayed. The real reason is that fixed income investors are screwed, possibly forever, and everyone knows that the Fed has eliminated risky consequences. Let’s start with the Fed. Sven Henrich from Northman Trader has been all over the Fed’s double-speak for years, and recently illuminated an interesting passage from Jerome Powell back in 2012. In the FOMC minutes from October 2012, Powell (at the time a Fed Governor) said the following:

“I have concerns about more purchases. As others have pointed out, the dealer community is now assuming close to a $4 trillion balance sheet and purchases through the first quarter of 2014. I admit that is a much stronger reaction than I anticipated, and I am uncomfortable with it for a couple of reasons. First, the question, why stop at $4 trillion? The market in most cases will cheer us for doing more. It will never be enough for the market. Our models will always tell us that we are helping the economy, and I will probably always feel that those benefits are overestimated. And we will be able to tell ourselves that market function is not impaired and that inflation expectations are under control. What is to stop us, other than much faster economic growth, which it is probably not in our power to produce? Second, I think we are actually at a point of encouraging risk-taking, and that should give us pause. Investors really do understand now that we will be there to prevent serious losses. It is not that it is easy for them to make money but that they have every incentive to take more risk,and they are doing so. Meanwhile, we look like we are blowing a fixed-income duration bubble right across the credit spectrum that will result in big losses when rates come up down the road. You can almost say that that is our strategy. My third concern—and others have touched on it as well—is the problems of exiting from a near $4 trillion balance sheet.”

We had no plan back in 2012. The problem is even worse now, and we have even less of a plan today. And Powell is not alone. Incoming Treasury Secretary Janet Yellen is equally wishy washy. As David Rosenberg jests, the Fed is like the heart doctor at an eating contest -- gorge all you want, they’ll keep you alive.

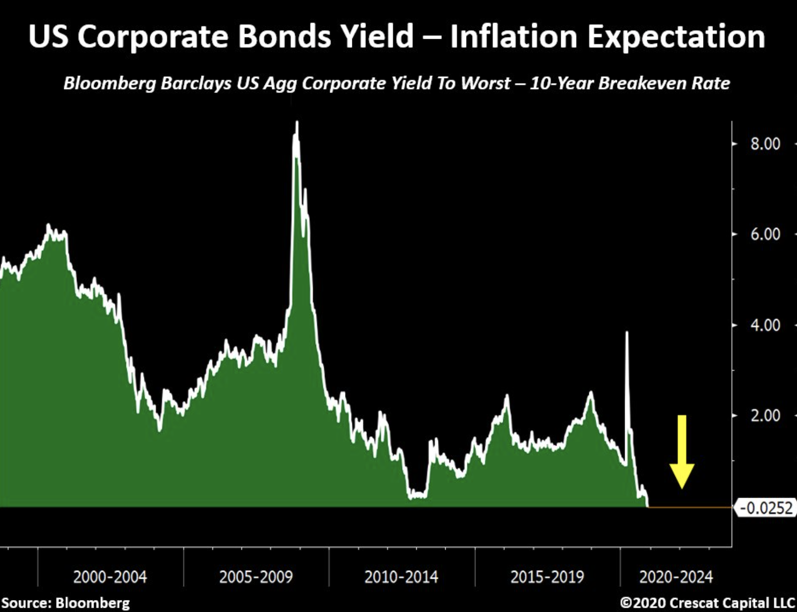

Over the last 10 years, the “everything rally” has created such insane investment gains across all asset classes, that there really weren’t notable fund flows in any one direction. No matter what you owned, it was working, and would likely continue to work. But that is all finally starting to change. Fixed income investors are now screwed, and they all know it. Sure, they are still binging on debt, but go talk off-the-record to any fixed income fund manager or sales person, and they’ll tell you that their job has a short shelf life. Corporate bonds are now yielding less than inflation -- the first time that has ever happened. As John Street Capital points out:

“The annual expected inflation rate over the next decade is 1.89% according to the Federal Reserve Bank of St. Louis. The average IG corporate bond yield is just 1.85% per Bloomberg Barclays data. This has already had & will have a profound effect on risk assets.”

Good luck with that 60 / 40 portfolio. As GMO highlights, the point of the 60/40 portfolio is to give you bond investment gains during periods of equity turmoil. They cite:

“Income is only a piece of the puzzle. The inimitable charm of government bonds over the last 30 years or so has been their wonderful tendency to give capital gains when the world starts to fall apart. Five times out of six, the 10-Year note did a wonderful job of cushioning the pain of the bear market, and across all six bear markets it averaged a double-digit capital gain. The fly in the ointment is that those capital gains came from an expectation that the Federal Reserve would reduce interest rates to combat any economic weakness. In each of the above events, such a reduction was possible. Today that is probably no longer true.”

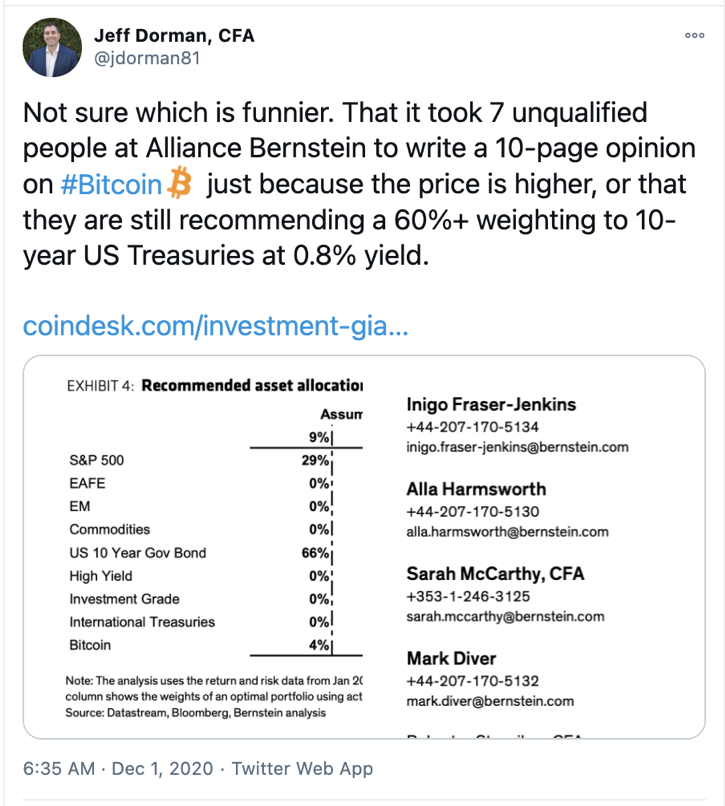

Some wealth managers are beginning to offer solutions to this problem, sort of. Bond bull AllianceBernstein recently made headlines for suggesting that Bitcoin now has a place in a diversified investment portfolio. While the Bitcoin headlines excited a few, the recommended portfolio that AB suggested should have their clients absolutely terrified.

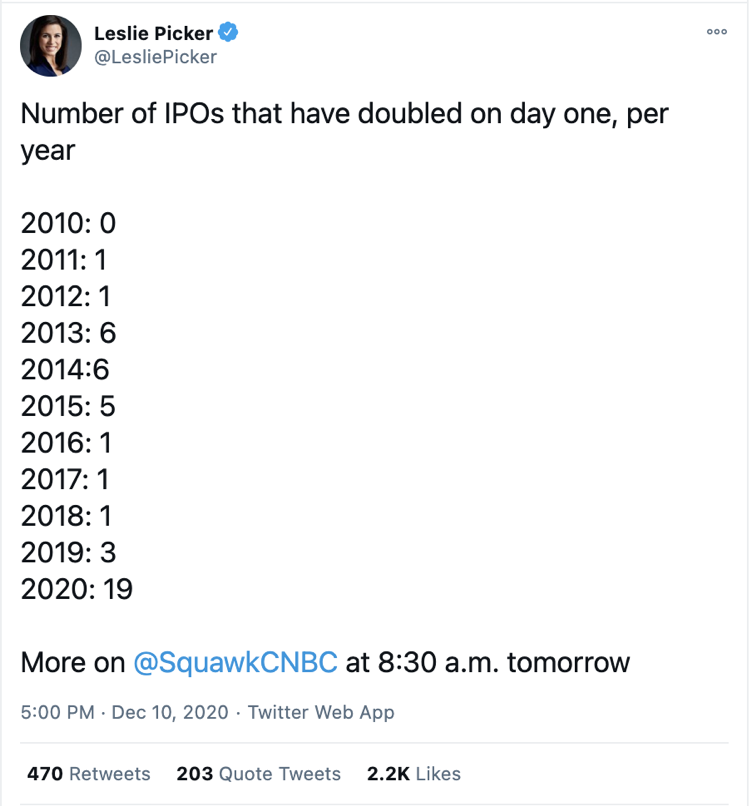

Which brings us to the IPO market. Nothing even has to be said about this. It’s pure insanity. And why shouldn’t it be? The Fed and the fixed income market are daring investors to hold cash and bonds. You might as well buy every new equity issue regardless of fundamentals or growth.

Which leads us to last week’s Airbnb and DoorDash IPOs. On the one hand, 100% gains in the first week of trading show that investment banks are clueless and that companies are leaving money on the table. On the other hand, this is great news for investors right?

Except it isn’t.

Prior to the IPO, Airbnb had a handful of investors, all of whom were already hilariously rich. Airbnb also has 188 employees, who are now hilariously rich. But marketplaces don’t succeed because of investors or employees… marketplaces succeed because of suppliers of product, and consumers of product. In the case of Airbnb, there are almost 3 million hosts, and 500 million customers, yet over $100 billion in investment gains were created before the majority of these people will make any money off of the success they created (Doordash similarly has 20 million users and 340,000 participating restaurants). Oh, forgive me, Airbnb’s PR team half-heartedly gave $238 million of the $100 billion to its community. Gee, thanks.

If you’ve come this far, hopefully you are as angry as I am, and are starting to see why this has everything to do with digital assets. While blockchain began with “cryptocurrency” and Bitcoin, it is now much deeper than that. It has become a tool for companies and projects to raise capital, bootstrap their growth, and give both the financial gains and product utility to their communities. In the case of Airbnb and Doordash, their investors (financial gain) differ from their users (utility). In the case of every company that has issued a digital asset, the community of users ARE the investors. While a blockchain is not necessary for this to occur, it has proven to be the most fair and easy way to pull this dynamic off. Companies who issue digital assets are not faceless technologies -- they are companies with developers, employees, customers, hosts and everything in between, and this new technologically-enabled asset class has given both tech and non-tech companies the ability to empower their entire stakeholder group, not just its shareholders. You will see a digital asset in every company’s capital structure in the near future. Until then, there are a handful of companies and projects where every day customers, developers, employees and investors are working together to both get rich and build successful products.

The IPO market has become a farce. Fortunately, there is now an alternative.

What’s Driving Token Prices?

Bitcoin traded in a wide range last week, but ultimately went nowhere despite multiple large financial institutions announcing support. As Coinbase pointed out, there was support for custodying digital assets (Standard Chartered & Northern Trust), trading digital assets, (DBS, the largest bank in Southeast Asia by assets), and both (in the case of BBVA, the second largest bank in Spain).

- The DeFi sector as a whole was beaten up, generically falling 10% week-over week, as futures markets seem to be driving the price action. Uniswap (UNI), YearnFinance (YFI), Synthetix (SNX), Thorchain (RUNE) and NexusMutual (NXM) all moved down in tandem. Sushiswap (SUSHI) bucked the trend, rising +7% as Sushi continues to eat into the parity level of UNI, with product innovation (BentoBox) and increased resources (YFI merger) giving it a bit of a thruster boost.

- Axie Infinity (AXS) rose +25% as the Land demo proved successful, and metrics for game usage (marketplace revenue and breeding fee revenues) continue to hockey stick. These revenues will soon go to Axie's DAO and to an extent token holders, giving AXS holders a tangible asset backing the token.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

Source: Bloomberg / Twitter @TaviCosta

Source: Bloomberg / Twitter @TaviCosta