What happened this week in the Crypto markets?

The End of an Ugly & Peculiar Month

Crypto investing for the month of August began with a 20% rally in Bitcoin led once again by the same macro factors that have supported Bitcoin for most of this year -- endless rate cuts from global Central Banks, declining currencies including the critically important Chinese Yuan, a series of Trump tweets about tariffs and reckless monetary policy, and a nasty decline in equities.

Unfortunately for the crypto markets, the perfect macro storm was erased throughout the rest of the month as these negative correlations quickly broke down. Bitcoin finished the month down 5%, retracing all of the gains and then some, culminating in a 10% decline over the final week of the month. While -5% is a yawn relative to recent volatility given this move can easily be doubled or wiped out in a single day’s session (case in point: BTC rose 7% on September 2 alone, erasing August’s losses), the monthly decline is important nonetheless because Bitcoin failed to live up to the “macro hedge” that many hoped for during the second month of US equity declines this year. Meanwhile, both Gold and US Treasuries posted significant monthly gains.

The argument for crypto has never been “negative correlation” but rather “zero correlation” -- nevertheless, crypto investors (including us) can’t celebrate convenient spurts of negative correlation while ignoring the opposite when it no longer suits the narrative. We acknowledge that Bitcoin is not quite a safe haven yet -- and certainly isn’t here in the U.S where the US Dollar is still king. However, it’s equally important to recognize that Gold, US Treasuries and equities can be bought/sold at the same time using the same brokerage account using the same investing vehicles (ETFs), whereas buying/selling Bitcoin not only requires completely different workflows and systems, but has completely different trading hours. So the notion that Bitcoin isn’t defensive simply because the reactions aren’t real-time is flawed from the start.

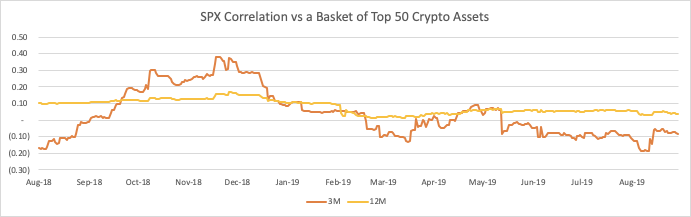

The diversification aspect of Bitcoin and the long-term lack of correlation matters much more than any near-term reactions.

Source: General Risk Advisors - proprietary data for Arca

Diversification, not Negative Correlation

My whole thesis on Bitcoin is many parts of the world need an alternative to their own fiat currencies for all kinds of reasons. Look at the weekend news: currency controls in Argentina; tear gas to subdue protesters in Hong Kong. If you mapped out a continuum and had the US dollar at one extreme (100) and had the Zimbabwean dollar and Venezuelan Bolivar at the other (0), where would you plot Argentina's currency? The clashes grow with intensity. For the 1st time since I've been involved with crypto, we're seeing real demand from ultra-high net worth mainland Chinese business types asking for an on-ramp to bitcoin - and an off-ramp for the yuan. It's one thing to read about it on Twitter or in blogs; it's another thing when you pick up the phone and the client says: "We want to move fast." Bitcoin doesn't have to be the alternative to the weak or troublesome currencies that keep popping up all over. The status quo is always an option, too. It's a risk to get out of bed in the morning; staying in bed indefinitely poses risks as well.

Essentially, Mike is arguing for choice and diversification. The problem of course is citizens of some countries have no choice, or have to jump through hoops in order to express freedom of choice. This creates a lag, and this lag skews real-time data. A far worse problem is some very large institutions have no choice either, or at least can’t act quickly enough and thus choose to act like they have no choice. Pension Funds, for example, are stuck between a rock and a hard place, but are in a unique situation where they get to dictate how much trouble they are actually in by creating the inputs for their own valuation formulas. The entire global debt market is shouting that returns will be nowhere near 6%, yet pension funds are running models based on these flawed expectations.

We are currently in completely unprecedented times, and that usually means traditional models won’t work. Said another way, the status quo won’t work. An advisor at Ritholtz Wealth Management recently pointed out that this year’s significant rally in Gold, US Treasuries and US stocks has only happened one other time since 1930 (in 1986), and conversely, all three asset classes have only lost ground in the same year one time since 1930 (last year).

Given what is happening, diversification should be the only investing attribute that truly matters right now.

Expanding the Playing Field - the Difference Between BTC & other Digital Assets

The recent crypto decline really has nothing to do with Bitcoin at all. Bitcoin has been performing perfectly well, and rationally, as a risky asset with some defensive characteristics. But the “everything other than Bitcoin” universe is struggling under the weight of lofty and unmatched expectations.

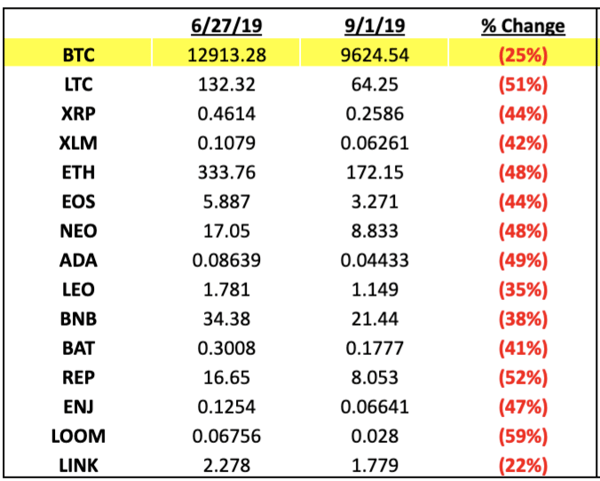

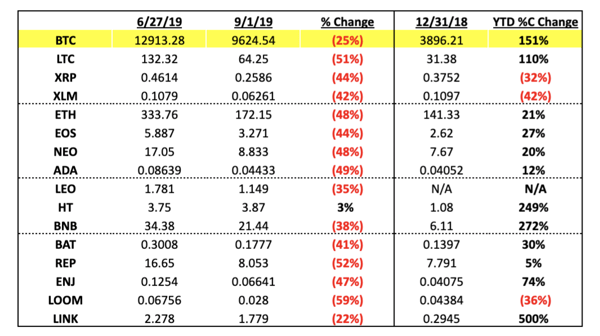

Declines of Select Non-BTC token prices since June 26 highs

Similar to broad-based moves in equities, where each stock/sector produces gains/losses with different orders of magnitude depending on the perceived "quality" of each stock/sector, the cryptocurrency and digital token asset class continues to mature, a lot of the same patterns are emerging. Within the broader digital asset ecosystem, some tokens are proving to be higher quality than others, and are beginning to be classified further into "haves" versus "have nots." Even amidst a broad 30-50% decline over the past 2 months, we're seeing these orders of magnitude in terms of individual token returns.

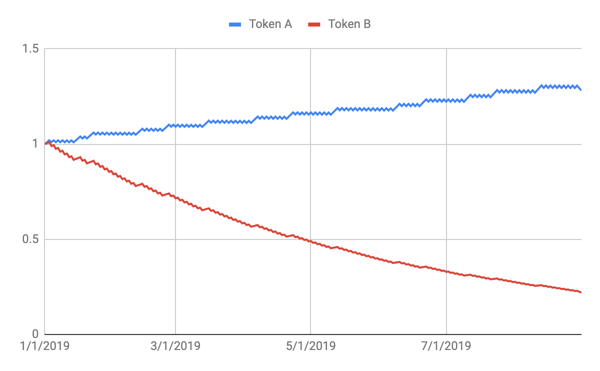

A common throwaway in crypto is that the “universe is too highly correlated”, and thus, there is no differentiation. But correlation does not indicate orders of magnitude. If, for example, two tokens (A & B) always move up together, and always move down together, but Token A moves up 1% on up days and moves down 1% on down days, but Token B moves up only 0.5% on up days but falls 2% on down days, the correlation between these two tokens would equal 1.0, while overtime, Token A would vastly outperform Token B.

Hypothetical Bifurcation of Returns Between Two Perfectly Correlated Tokens with Different Up/Down Capture

While the entire crypto space has struggled, and it may be easy to lump all of them together since -30% in 2 months feels just as terrible as -50%, these orders of magnitude matter greatly over longer time horizons.

Looking at the same table as above but including YTD returns shows how the “everything is the same” narrative truly breaks down. There are many different sub-categories of digital assets, most of which have nothing to do with currencies like Bitcoin. When looking over longer-time horizons, a few trends emerge:

- Bitcoin is outperforming all other forms of “Money” or “Hard Currency” and is acting as a macro hedge against rising global geopolitical risk.

- Protocols and platforms that are years away from having commercial success (ETH, EOS, NEO, ADA) and lack of clear valuation metrics are being treated by the market as risky, high beta investments, and have underperformed as their platforms have over-promised and under-delivered.

- Real cash-flow producing companies, like those running crypto Exchanges (BNB, HT, LEO) are outperforming as these companies grow quickly, and are finding innovative ways to use tokens in their cap structure and on their platforms.

- “Applications” are a mixed bag -- some are showing little to no traction (like LOOM & REP) while others are growing in both size and strategic importance (like LINK and BAT).

The crypto ecosystem is evolving. Gone are the days of unilateral symmetric movements, replaced by a market where the winners begin to consistently outperform the losers, which incidentally is the reason why Active Management is outperforming Passive Management (see “What We’re Reading” section) -- research and security selection matter. Those that have a choice beyond the status quo can be a part of this evolution, and have a chance to take part in what looks to be a sizable paradigm shift in the tokenized ecosystem.

Notable Movers and Shakers

Bitcoin fell (-4%) for the third consecutive week as summer winds down. The holiday weekend likely contributed to a muted newscycle, but there were a handful of events that deserve notice:

- Loom (LOOM) announced in a Medium blog post early last week that they plan to integrate with Libra, adding interoperability support for Libra (and therefore their code language, Move). The integration allows for Solidity smart contracts to work on the Libra blockchain and therefore for Loom’s gaming applications to work across both Ethereum and Libra.

- In the private world: Hedera Hashgraph (HBAR) announced it will launch its mainnet (beta version) on September 16. Telegram (TON) also released code to run a node on its testnet over the weekend, with an expected mainnet launch of October 31 (according to the purchase agreement). Both launches are notable as these projects raised massive funding rounds of $200m (HBAR) and $1.7b (GRAM) in 2018, leaving many with high expectations for these projects’ performance.

- Binance (BNB) rolled out its lending product to exchange users for three assets - BNB, USDT, and ETC. While the lending offering is only over a 14-day period, this appears to be a litmus test for further expansion into the lending space. In the same week, Binance announced a platform, Binance X, which aims to help developers learn and collaborate within the blockchain ecosystem. They have also hinted at enabling futures trading on the platform “very very soon”, as well as alluding to the launch of “Venus” which aims to rival Facebook’s Libra token. The flurry of news comes as no surprise, as Binance is looking to further entrench themselves as the leading cryptocurrency exchange.

What We’re Reading this Week

Investment management firm, ARK Invest, lays out the five "transformative innovation platforms" to watch: artificial intelligence, DNA sequencing, robotics, energy storage, and blockchain technology. They estimate these sectors combined will generate $50+ trillion in value over the next 10-15 years. One key takeaway is that new technologies can take many years to become adopted and disruptive innovation can take 40 years to fully affect the economic development cycle.

According to a recent report from Forbes, Alibaba, Tencent and five other companies will be the first to receive the Chinese government's cryptocurrency. Sources say that the currency could launch as early as November 11, an important shopping day in China. By handing the currency out to 7-8 institutions to start, they hope it will trickle down to consumers who regularly use these businesses. The launch of such a currency has many implications, including potentially curbing use of outside crypto assets, solidifying China's sovereignty over its national currency, and the Chinese central bank maintaining control over monetary policy.

Unlike traditional hedge funds that rarely outperform passive index products, crypto hedge funds have generally outperformed passive indexes and Bitcoin. The study found that most funds actually underperformed in the 2017 bull market, with ~10x returns versus Bitcoin's 12x for 2017, but vastly outperformed in 2018. In addition, it found that the average age of the funds (an indicator of manager experience) was also much lower (16 months) than the median of traditional hedge hedge funds (52 months).

Amid the Hong Kong protests, which are now in their twelfth week, a number of local businesses have begun accepting cryptocurrencies as payments. Pricerite, a popular department store in Hong Kong, announced it will begin accepting BTC, LTC and ETH as payment, converting the crypto instantly to Hong Kong Dollars. The move to crypto payments comes as protesters have shifted their tactics to economic damage: protesters have been withdrawing cash in mass from banks and ATMs. With the threat of further declines of the HKD vs the USD peg, many are turning to crypto as a way to protect their assets.

A new report from Coinbase finds that 56% of the world's top 50 universities now offer blockchain courses spanning the disciplines of engineering, humanities, finance and more. This 25% increase from 2018 is also coupled with an increased interest from students, 34% of those surveyed indicated interest in taking blockchain-related courses. Blockchain education is essential for adoption and the proliferation of interest among university students is promising.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)