What happened this week in the Crypto markets?

Macro Recap - Bitcoin Currency Back in The Black

The summer doldrum was very apparent in the digital asset space as liquidity had been sucked out of the market for the past few months. With summer over, liquidity is now slowly coming back, and Bitcoin posted its first positive week since the beginning of August. We are currently in the mid-point of a long-lasting trading range between $9,000-$12,000, and market participants are becoming a bit impatient. Most alternative assets are not holding to their BTC pairing, causing underperformance by and large across the ecosystem (BTC’s share of the overall digital assets space is up to 71.8%, a 110% increase YTD).

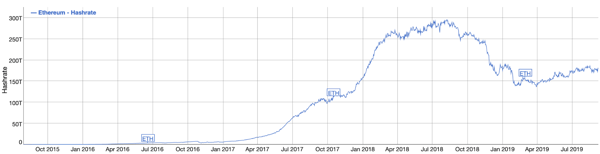

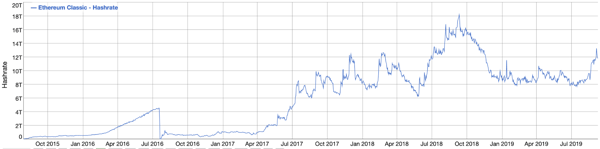

Ethereum is beginning to lose favor among miners, with the ETH/ETC hashrate ratio dropping (signaling an increase in hash rate in Ethereum Classic comparative to Ethereum - miners may be switching to the more profitable network for the time being).

While the first 6 months of 2019 was driven by catalysts, many market participants now remain on the sidelines awaiting the next significant catalyst with enough legs to propel this market out of the current range. Bakkt (a regulated crypto derivatives exchange owned by NYSE ICE) opened deposits this month, and coincidentally ~$1B worth of Bitcoin moved to a new address on the same day. Bakkt plans to open their first futures contract September 23rd, which will be worth watching. While we wait, it’s important to keep things in longer-term perspectives.Bitcoin went from $3,200 to $14,000 in just over 7 months. While it is easy to be distracted by the short term volatility , investors must take a patient approach to this decade’s most profitable asset class.

We Have a Choice -- A Reminder of Whence We Came

A non-productive market is a good time to reflect. The digital assets space is now a diversified ecosystem, with numerous digital use cases for asset growth and transfer that stretch far and beyond “currency”. In fact, the generic term “cryptocurrency” has actually become damaging, as it conjures up images of purchasing and bartering, when in fact, a majority of digital assets are not at all meant to be currencies. Confusion over the types of digital assets is compounded further by confusion over the terms we use to describe basic services, such as custody and storage. These differentiations and standardizations will develop over time, and when they do, Bitcoin will no longer be the only topic of discussion.

But for now, Bitcoin’s simple narrative and limited functionality is the easiest to understand, both because of its exponential growth and its rationale for existence. It’s the best starting point for understanding why digital assets need to exist, starting with alternatives to fiat currencies, and the natural extension from there is understanding why other types of digital assets can be utilized as well.

Let’s start globally. The world simply can’t afford higher rates. Without rising tax receipts and massive GDP growth, there is simply no way to refinance absurdly low coupon debt with even modestly higher coupon debt across hundreds of trillions of dollars of debt. Every indebted nation and company immediately becomes insolvent when cash outflows rise and inflows don’t keep pace.

As a result, there are only 2 ways out of this mess:

- Continued lower rates (which is what is happening despite every economist calling for higher rates)

- Massive inflation to reduce the impact of the debt burden (enter Modern Monetary Theory)

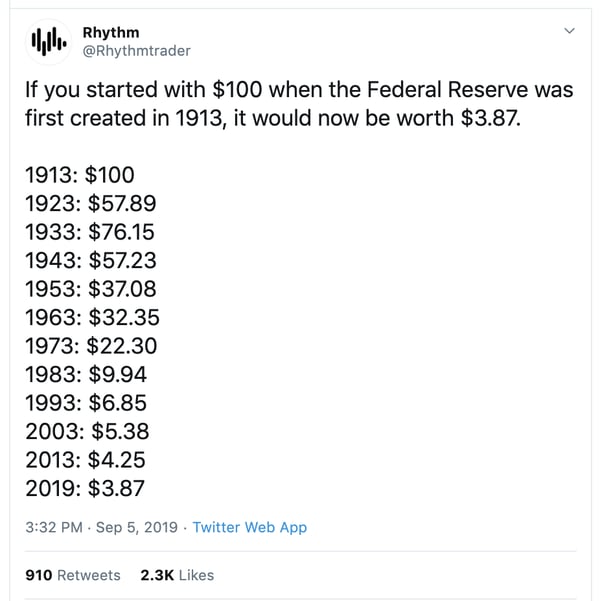

These two factors are of course the ultimate bull case for Bitcoin. Low rates reduce the opportunity cost of holding non-yielding assets, and both inflation and deflation make Bitcoin attractive as a form of alternative purchasing power. The rise of Bitcoin, a currency in digital form, is simply providing people with a choice. Choice is a funny word, because we all have it, even though we often choose not to utilize it because of historical norms and convenience. For instance, we may not think we have a choice other than using US Dollars, since we pay taxes with US Dollars and most of our assets and liabilities are in US Dollars. But that simply means US Dollars are necessary and mandatory in some instances; it doesn’t mean there are no additional alternatives. If you give up your choice, you start to accept things the way they are without challenging them, which leads to situations like this:

Any 8-year old would look at the above and think this is crazy, and would immediately try to figure out how to protect their piggy banks from this massive wealth destruction. But the rest of us with any semblance of economics knowledge simply chalks it up to “normal inflation”. It’s easy to say “my car costs $30,000 now even though the same car cost $10,000 twenty years ago” if all of your other assets (stocks, bonds, real estate) have appreciated at the same absurd rate. While you do have a choice, it’s just as easy not to bother exercising this choice… as long as you own other assets.

But what if you don’t own other assets? While the majority of wealth in this country is owned by those who have benefited from decades of lower taxes, lower yields, non-stop financial engineering and debt-fueled bubbles, the younger generations don’t have any assets, and have little to no loyalty to the status quo. Will they be the ones who exercise choice?

What about outside the US? What happens when this same inflation not only crushes your purchasing power domestically, but also abroad? Most of these citizens had no choice prior to Bitcoin… but now they do. Will they be the ones who exercise this choice?

For some, this choice is starting to become a no-brainer, and we’re witnessing the results of this choice via demand (and thus price increases) of Bitcoin every month and every year. While many people focus on the volatility of Bitcoin and immediately dismiss it as a currency, perhaps a better way to think about it is to focus on the monthly and annual lows of Bitcoin, and watch the increasing growth distribution.

It’s not often we get to see the results of choice in real-time -- but Bitcoin provides a daily scoreboard.

Another Unique Token Use Case - Huobi Token (HT)

We mentioned above that digital assets have a wide range, much beyond currencies like Bitcoin. We recently learned about a new digital token that exhibits this wide range of functionality.

The token was issued by an Asian digital asset exchange, Huobi, which matches buyers and sellers of digital assets, and takes a cut from each trade. This is a real company with real equity, earns real revenues/profits, and still found a unique use case for a token within its capital structure that serves themselves and their customers with a different purpose.

Within 10 minutes of learning about this token, we went from “this is a total sham” to “wow, that’s actually really innovative and smart”, which shows that even those of us who are already believers still need education.

In a nutshell, this is how the Huobi token is used:

Similar to tokens issued by other Exchange companies, buyers of the Huobi token receive discounts on trading fees if they own the token. The Exchange also uses a portion of all revenues to buyback (or “burn”) tokens, creating constant demand and limiting supply. Thus, the token is part “investment” based on growth of Huobi’s revenue, and part “utility” in the sense that you can use the Huobi token like “reward points” for discounts and other benefits.

But the Huobi token also has unique governance features. When Huobi is deciding which new tokens to list on their Exchange for trading, they list 2 projects on their website, and Huobi token holders can vote on the project they want to see on Huobi, with priority given proportionally based on how many Huobi tokens each voter owns. If you vote for the winning project, upon listing of that project’s token on the Huobi exchange, you have the right to buy that new token at a large discount. The Huobi tokens that are collected in the voting process are subsequently burned. This is actually a brilliant use case for a token. It incentives their community to own the Huobi tokens, while also guaranteeing that companies that list on their Exchange have initial demand and a community of supporters.

We highlight this because it is a great demonstration of how flexible token structures are, given they can be programmed to do literally anything. And also because we too were confused at first, even though our team spends every second of every day thinking about investments in digital assets. A company can utilize a token to grow their business even if they also have shareholders fighting over the same revenue and profits. Huobi has created customer incentives in the form of discounts, voting, network effect and share in profits.

Everything that is new and different is hard to process at first, but eventually the lightbulb goes off. And when it does, it can be enlightening.

Notable Movers and Shakers

This week was by and large Bitcoin dominated - the ebb and flow of the broader market matching its movements. The most important headlines were pertinent to Bitcoin infrastructure, reemphasizing the rift widening between Bitcoin and the rest of the digital asset space:

- Formerly known as trueDigital, Tassat has announced a pivot towards Bitcoin derivative trading and institutional payments markets.

- The same day that Bakkt announced that its Bitcoin deposits had officially opened, close to $1b worth of Bitcoin moved on-chain. Rumors has it that these two events are correlated. This movement was well documented and analyzed but the true nature of the event has yet to be determined.

What We’re Reading this Week

In this op-ed, Coindesk’s Noelle Acheson discusses the proliferation of the idea that institutional investors, when they enter crypto, will start the next bull run. Many believe that institutional adoption will begin with more regulatory clarity or better infrastructure, but Acheson argues that institutions are actually waiting for retail interest to kick in. As a large portion of institutions manage retail funds, they therefore need interest from their retail base to indicate interest in the asset class. At the end of the day, crypto is still a small niche, but servicing both institutions and retail will be critical for adoption.

Modern Monetary Theory (MMT) has received a lot of notice in recent years, mostly at the hands of Stephanie Kelton, the senior economic advisor to presidential candidate Bernie Sanders. MMT is the theory that governments should print more money to pay for large expensive programs as long as they control for inflation. The article traces the origins of MMT as well as Kelton’s discovery and subsequent support of the theory. However, MMT has dangerous implications if not properly administered, and when powerful individuals speak about theories such as these, it further pushes the need for inflation and censorship resistant assets.

Stablecoin creator Paxos launched the first gold-backed digital asset last week, an asset that was approved by the New York Department of Financial Services (NYDFS) to offer Pax Gold (PAXG). Each PAX Gold represents one troy ounce of London Good Delivery gold. The purpose of PAXG is to make gold portable and transferable without the regular burdens accustomed with gaining exposure to the asset. The token is also redeemable for the physical gold that represents it.

Twitter CEO Jack Dorsey is the latest to be hit by “SIM swapping”, the newest cybercrime to make the rounds. SIM swapping is when hackers take control of an individual’s phone number and can then take over their email, social and sometimes cryptocurrency accounts. The crime has become increasingly popular and recent targets include celebrities and politicians. Hackers recently realized that they could access individual’s cryptocurrency accounts using their cell phone numbers, and unlike traditional bank transfers, crypto transfers cannot be reversed. There is still no concrete data on how many have been affected or what measures can be instituted to stop the hackers permanently, but public awareness of the crime is steadily growing.

The Marshall Islands, which has used the US Dollar as its currency since its independence in 1979, is moving to a cryptocurrency called the Marshallese Sovereign (SOV) to be used alongside the dollar. The country’s Minister-in assistance, David Paul, cited the many benefits of using cryptocurrency including faster transaction speeds and reduced fees. They plan to hard program the currency to create additional supply at a rate of 4% annually, a rate that cannot be modified by the government. The minister touted the importance of the move to blockchain technology for the country and the importance of having a sovereign monetary system for participation in the international finance markets.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)