What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 8/23/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

-0.8%

|

+60%

|

|

Bloomberg Galaxy Crypto Index

|

-6.3%

|

+92%

|

|

S&P 500

|

+0.7%

|

+5%

|

|

Gold (XAU)

|

-0.2%

|

+27%

|

|

Oil (Brent)

|

+0.6%

|

-31%

|

Source: TradingView, CNBC, Bloomberg

The K-Shaped Recovery Widens the Wealth Inequality Gap

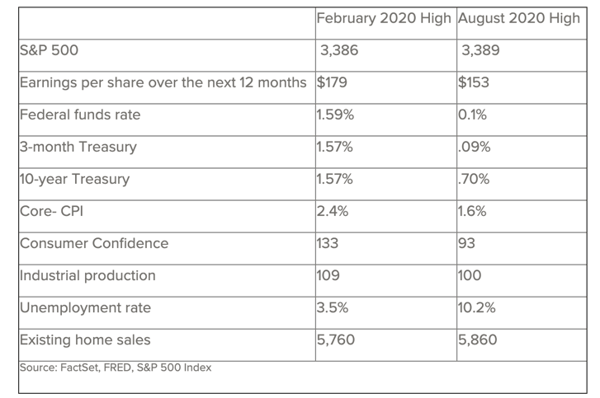

Before we get to the digital assets market (which stalled last week for the first time in five weeks), let’s take a moment to marvel at what might be the most incredible equity bull run the market has ever seen. According to Edward Jones, since 1956, it typically takes four years on average for stocks to recover from a trough to a new record high, but last week’s record high in the S&P 500 was reached in just six months after the March low.

Peeling back the onion, while the S&P 500 looks the same now as it did in February, the corporate and economic fundamentals that typically drive stock returns are quite different. Said another way, this is not the playbook anyone would have written for reaching new highs. Even those of us who held the opinion that stocks won’t go down until 3Q and 4Q earnings never imagined the market would reach new highs.

Source: Edward Jones

Five months ago, just about every investor was forced to pick a side -- expect either a V-shaped recovery, or a horrible depression. As usual, the extremists got it wrong. Emily Barrett of Bloomberg summed this up nicely, saying that the recovery has actually been K-shaped, which partially explains why the stock market has recovered so quickly despite incredibly lumpy and contradicting economic data:

“The idea behind the letter K is that some people and companies have managed to get through the health crisis in good shape, while many others are suffering. K-shaped economic and market data show a widening gap between the comparatively privileged -- for instance, those with jobs they can readily do from home -- and the disenfranchised. This divergence is wretched in part because it raises the risk that those in charge of the rescue effort will call it off when headline numbers are looking better. For instance, the urgency of another $1-trillion-plus stimulus package was apparently harder to grasp with payrolls numbers beating expectations. The Covid-19-exacerbated gap between the privileged and the rest is a depressingly pervasive pattern, and it’s reflected in the bond market.

This week, high-grade issuance reached $1.346 trillion year-to-date, smashing the full-year record set in 2017. Over the past three months, A-listers like Amazon, Alphabet and now Apple have each secured the lowest borrowing costs in history, or got close to them, for monster deals. Meanwhile, New York’s MTA just turned to the Fed for affordable funding. Unequal access to the corporate bond market puts the U.S. recovery at risk. Disparities have always existed in the bond market, but more banks have tightened standards on lending to small businesses than at any time since 2009, and the stakes are higher than ever now, amid warnings of record corporate defaults and bankruptcies. The painful and long-term implications of a K-shaped recovery are kryptonite to the Fed, which has faced widespread accusations of exacerbating inequality in its response to the global financial crisis.”

Wealth inequality is one of the “Big Factors” that is shaping our world, now and in the future. Everything from politics, to Brexit and Occupy Wall Street, to the recent global riots are fueled by people who are essentially saying, “I don’t care how bad the alternative is, we want something new.” Monetary inflation explains a substantial portion of the wealth gap, as does capital formation solely rewarding equity holders over customers. Sound money like Bitcoin may fix the inflation problem, by restoring fiscal and monetary discipline and ultimately rebuilding the middle class. Meanwhile, democratized capital formation via digital assets that reward community and network users instead of equity owners may fix the equity-holder problem.

Under this pretense, it’s not surprising that digital assets are growing so quickly. Democratizing finance helps to eliminate the wealth gap, slowly but importantly. It helps reward builders and community members and early evangelists, not just inflation-protected equity holders.Everywhere you look, you see growth and adoption.

The Elite are Being Forced to Use a New Playbook

Naturally, the elite shunned digital assets for as long as humanly possible -- but they are coming around now, quickly. If you can’t beat ‘em, join ‘em.

Warren Buffett recently dumped airline and financial stocks and bought a gold miner stock. This of course made headlines. Perhaps the headlines should have read, “Old playbooks no longer work”. This is not unique to Mr. Buffett… go down the list and you’ll see leaders in every niche of the capital markets now trying something new:

- Asset Managers: Paul Tudor Jones and Renaissance Technologies are now involved with Bitcoin

- Investment Banks: Goldman Sachs makes big hire on their digital assets team and JP Morgan begins banking Coinbase and Gemini

- Public Companies: Microstrategy announces the first corporate finance Bitcoin cash management strategy

- Private Companies: Atari and Reddit experiment with issuing digital assets to bootstrap growth and reward users

- Governments: Numerous countries are working on their own Central Bank Digital Currencies (CBDCs), while the IMF just issued an explanatory video about cryptocurrencies

- Old guards: Former Prudential CEO changes his tune on Bitcoin, and now turns bullish

And it’s not just Bitcoin. “Cryptocurrency” is an outdated term, and simply does not include the bulk of the thriving digital asset universe. While 2017 famously brought ICO scams and useless, poorly constructed tokens that were trying to piggyback on Bitcoin’s and Ethereum’s success, 2020 has brought “Pass-Thru” tokens, which are arguably the most dynamic investment structure ever created. Companies can now pass through revenues, profits, user growth and rewards all in one investment vehicle. These quasi-equity / quasi-utility features allow companies to reward their customers with equity-like returns, while also giving their customers discounts and heavy incentives to use their products and evangelize on their behalf. There will undoubtedly be a public company in the near future that recognizes this flexible and non-dilutive addition to the capital structure, and issues their own pass-thru token.

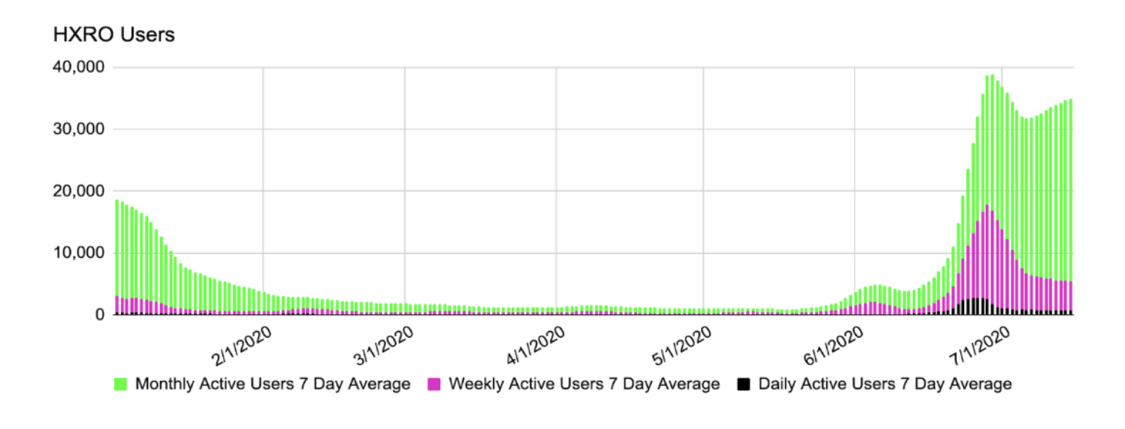

HXRO: A Great and Unique example of Pass-Thru Tokens

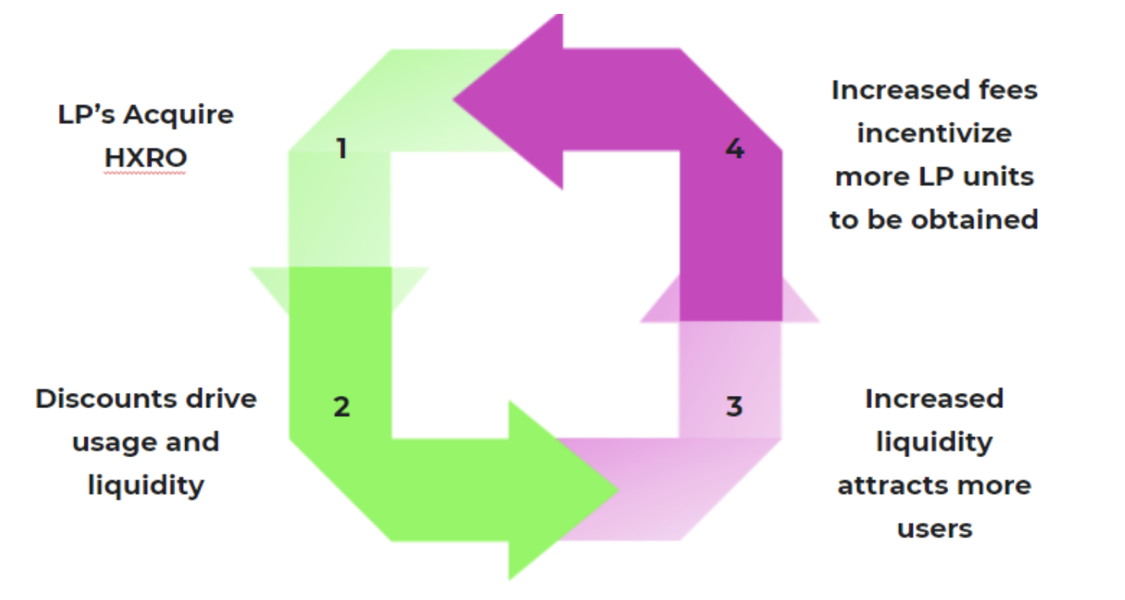

The evolution of token design continues at an alarming and exciting pace. Perhaps no token demonstrates the creative “pass-thru” flexibility better than that of Hxro (HXRO). HXRO is a new type of crypto derivatives exchange platform that offers a simple way to express a view on price, and trade digital assets. But forget about Hxro’s product for a second -- their token design can work for any company that is trying to grow customers and reward them for being early adopters.

Using a page out of the old Taxi Medallion model or CME seat license model, HXRO has created a “liquidity producer pool (LPP)”, whereby owning a “seat at the table” is crucial to unlocking financial gains. In order to claim an LPP unit, an LP must stake a minimum of 250,000 HXRO tokens for a one-year term. In exchange for a full LPP unit, the LP will unlock fee discounts and rebates on HXRO’s platform as well as earn a pro-rata share of 1/3 of net network transaction fees spent by users on the platform.

Essentially, the LPP model helps bootstrap the entire HXRO ecosystem. Their biggest customers become their biggest token holders, who then become their biggest quasi-equity owners, who in turn are incentivized to become even bigger customers. This explosion in growth is expected to attract more users, some of whom also become quasi-equity holders, and the pattern repeats again and again and again.

This type of innovative token design is what is leading to such explosive growth for many digital asset companies, and it is just one of many new, exciting token structures. This is why we constantly compare digital assets to the bond market -- each token has its own unique properties and attributes much like the different structures, maturities, coupons and covenants in the bond market. And in many cases, companies are now issuing tokens AFTER raising equity and achieving product market fit. It’s the reverse of 2017. In 2017, companies had no plans and just chased the hot money, only to fall flat and return little utility or financial gain to their token holders. In 2020, companies are rewarding their users with tokens that are well designed and may lead to both greater utility and wealth creation.

It also makes you wonder why there are still no investment bankers in digital assets. Investment bankers, in theory, get paid to come up with creative capital solutions for companies, yet they continue to saddle companies with more and more standard unpayable debt and dilutive equity capital. Meanwhile, what we see as the best capital formation and bootstrapping growth mechanism in history is occurring organically unbeknownst to them.

We wrote a few weeks ago that Amazon Prime should have been a tokenized asset. The idea that an ownable asset can be both a utility and an investment at the same time can change the course of investing, and company formation as we know it. It’s not a fluke that this equality-enhancing financing mechanism is exploding at the same time that the traditional capital markets are leaving every-day citizens behind.

The elite are no longer in charge in a fast-growing market. While many are coming over, they will simply be regular participants just like everyone else.

Notable Movers and Shakers

This week was a trader’s paradise: Bitcoin’s sinusoidal price action gave rise to a choppy market that evaded the attention of investors. Whereas Bitcoin went up 5% in the beginning of the week, it then fell 9% before settling at -2% (Bitcoin dominance had its first positive week in two months, finishing up 1.5%). Opportunities were to be had elsewhere, however, with a few notable events that stood out:

- OMG Network (OMG), months removed from announcing that their Plasma solution (MoreVP) was deployed on Mainnet, integrated USDT Wednesday onto their value-transfer layer in an effort to “reduce confirmation times delivering faster payments while fees will be reduced without compromising on-chain security.” The token reacted well to the news, finishing the week up 128%.

- Yearn Finance (YFI) released a new prototype for tokenized insurance on Monday following the recent success of Nexus Mutual. In the last seven days, there have been: proposals to change governance, over $1B of Total Value Locked (TVL) being reached, increased metric visibility, multiple instances of intra-sector collaboration, and a better understanding of what YFI offers Decentralized Finance (DeFi) in general. This translated over qtoken finishing the week up 88%, aided by the recent listing on Binance.

What We’re Reading this Week

In a video interview last week, George Ball, the former Prudential CEO and current chief executive of investment firm Sanders Morris Harris, revealed his bullish stance on Bitcoin. He mentioned that he’d always been an opponent of Bitcoin, cryptocurrencies and blockchain in general, but recent federal stimulus has raised alarms that the market might be in irreversible trouble. Ball also predicts the increased Bitcoin buying will begin after Labor Day and will be driven by activity on platforms such as RobinHood, as many have taken up day trading during the pandemic. Regardless, Ball’s stance on Bitcoin bolsters the digital assets market’s legitimacy and adds to the growing number of traditional investors endorsing the space.

While the USPS’s woes have been all over the mainstream media headlines the last few weeks. an important patent is potentially being overlooked. The USPS published a patent last week that describes a blockchain-based mail-in voting system aimed at making mail-in voting more reliable. The system would consist of a registered voter receiving a unique “computer-readable code” in the mail tied to their identity that then confirms the correct ballot information. The submitted information would separate the voter’s ID from votes, ensuring anonymity and confirming accurate vote count. The idea of blockchain-based voting systems are not new and have been piloted in a few cases. This year’s election and the Covid-19 pandemic may propel the adoption of these systems as voters stay home from the polls, although it is unclear if they will be used in the upcoming election.

Last week, Expobank, a Russian commercial bank, issued the country’s first crypto-backed personal loan. The loan was issued to a businessman backed by WAVES tokens. Although the value of the loan was not disclosed, the bank stated that the loan was “precedent-setting for both the legal and banking communities”. Expobank supposedly consulted with lawyers prior to processing the loan to determine that WAVES were considered “other property” and not payment tokens. The country recently issued a ban, set to go into effect in January 2021, on cryptocurrencies used as payments. Regardless, the issuance of the loan is another way that digital assets are beginning to bridge the traditional financial world with the digital one.

Last week, Archax became the first digital securities exchange to be granted a license from the UK’s Financial Conduct Authority (FCA) to carry out business as a multilateral trading facility (MTF) exchange, a broker and a cash and asset custodian. The registration with the FCA will be mandatory for all companies working in the digital assets space beginning January 2021. Archax will be focused on servicing the institutional market and offering digital securities (defined as tokenized stocks or bonds) with 35 issuances in its pipeline.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency