What happened this week in the Crypto markets?

A Crypto Bull Case without Hyperbole

Frequent readers of “That’s Our Two Satoshis” know that we often make comparisons to the High Yield bond market and Equity markets, and last week one of our four rationales for the ascent of crypto prices was that “Global Debt & Equity Markets are in a death spiral”.

One of our readers, a multi-family office manager with over $1 billion in AUM, responded with the following (paraphrased):

I don’t think it is correct to be bearish or neutral on equities. I hope we’re as lucky as the bear thesis to buy equities at better prices. In every industry, we are witnessing exponential breakthroughs. An infrastructure bill is coming. Wages are going up. The world is getting wealthier -- and they want Coke, iphones, Levi’s and Instagram. In the next 5 years, 4 billion people are coming on the internet for the first time, which is obviously less valuable than the first 4 billion, but think of the new vitality. The space industry is going to explode and will create multiple trillion dollar companies. BTW -- this is all bullish for Crypto too.

First, we LOVE feedback; please keep it coming. Education is a 2-way street, and no one is an expert in this space yet. Second, this is 100% accurate. While the “Crypto is completely uncorrelated to other asset classes” narrative is incredibly important for asset allocation decisions into crypto, that doesn’t mean that we are celebrating, nor expecting, a complete meltdown in equities. It’s possible, sure. The risks are incredibly high and growing, and many crypto advocates have lost all faith in an equity market that is propped up by debt, buybacks and central bank moral hazard. But it is not the base-case, nor is it necessary to validate the crypto thesis. The 1Q19 US GDP number was revised downward last week, but it was still the biggest 1Q GDP number since 2015, showing the U.S. economy remained resilient against trade and political headwinds. Similarly, 1Q19 earnings finished +1.5% YoY, which is not a great number but is certainly better than most people estimated (consensus was for a 4% decline).

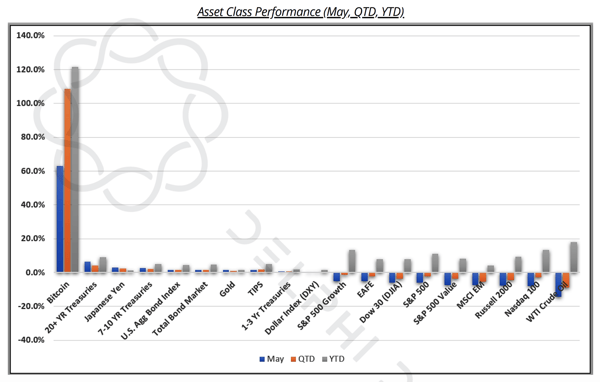

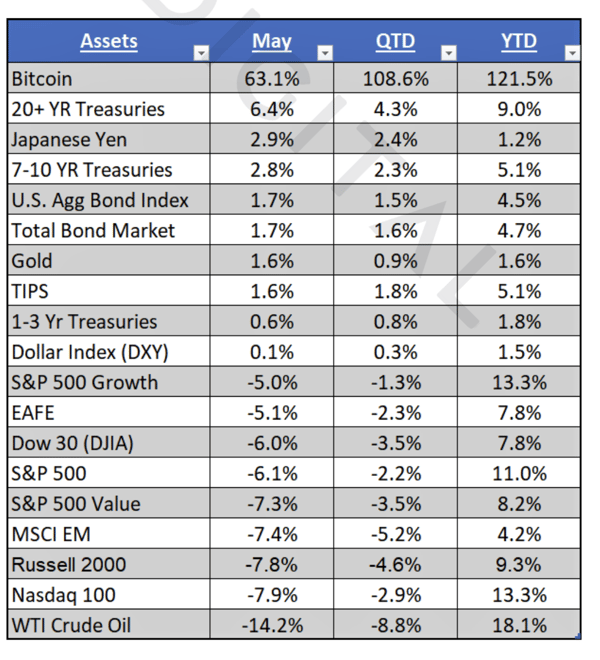

We have noted in the past that Bitcoin may be both a risk asset and a safe-haven. As a risk-asset, the equity bull case above is also wildly bullish for Bitcoin and other digital assets. As technology and infrastructure improve across the globe, digitally native and borderless assets will remain well bid. That said, it’s impossible to ignore the safe-haven aspect, especially right now when Bitcoin just had it’s fourth best month ever, rising over 60% while oil fell 14% and equities dropped 5-10%. Bitcoin has a clear value proposition in the context of experimental monetary and fiscal policies globally.

It is not hyperbole to say that we may be witnessing an asset class that offers the best of both worlds.

Asset Class Performance -- Bitcoin’s Meteoric Rise is Literally off the Chart

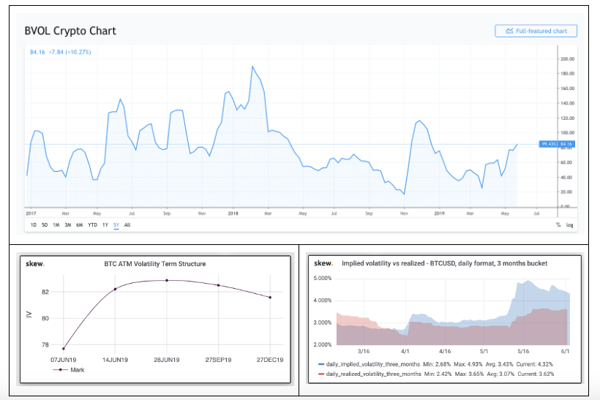

Cryptocurrency Volatility Rising is a Matter of Perspective

Bitcoin is now up over 100% YTD, as are most Digital Asset indexes. But investors know to look at risk-adjusted returns rather than nominal returns. Through May, the Sharpe Ratio for BTC is 3.20% YTD, compared to 0.66% for the S&P 500. Simple math tells you that if BTC is up over 10x compared to US stocks, but the Sharpe Ratio is up only 5x, volatility must be high.

This is of course true. The Bitmex Bitcoin Volatility Index (BVOL) has reached new YTD highs, and implied volatility is exceeding realized volatility by a healthy margin.

Bitcoin Volatility is Rising

Source: Bitmex, Skew, TradingView

At the same time, here are some interesting stats:

- Bitcoin and the overall crypto market have posted gains week-over-week for the past 7 weeks

- Bitcoin and the overall crypto market haven’t had a double-digit weekly decline since January 13th

- Bitcoin hasn’t fallen more than 3% week-over-week since January 13th

- In 16 out of the past 22 weeks, returns have been positive

For traders, crypto has been very volatile. In fact this past week alone, in one single trading day (Thursday), Bitcoin rose from $8700 to $9000, then dropped below $8200, and ultimately finished the day at $8500. Traders witnessed a 10% intra-day move. Meanwhile, the net effect was a pedestrian 2% day-over-day decline.

Perspective matters.

Token Offerings are Getting Very Interesting

Another new crypto protocol is on its way. Algorand, like many before it, is purportedly solving problems of decentralization, scalability, security and speed, as each of the other 20+ past protocols have claimed.

Without opining on the merits of the Algorand deal itself (though we encourage you to listen to this week’s Base Layer podcast to learn more), we want to highlight the structure of the token offering. New ALGO tokens will be offered via a Dutch Auction process, instead of via the more traditional ICO or IEO process. This is an innovative offering technique for an asset that is notoriously difficult to value, as there is no easy way to anchor investors to a “fair value” price. It’s also a bull market maneuver, preying on high demand and low price elasticity. When Google IPO’d in 2004, using a similar Dutch Auction process in lieu of traditional capital markets underwriting, it was viewed as a risky maneuver that if successful might change the way securities are offered in the future. Alas, it was a success for Google, but did little to change the way securities were sold in the future, and didn’t make a dent in the hefty Wall Street fee structure. But it did allow consumers to set the price rather than underwriters, and allowed those who care about Google the most to participate rather than just those with the biggest wallets and greatest access to Wall Street brokers. Similarly, Algorand believes this is the best way to fairly disseminate tokens to the most interested future users and investors.

Perhaps more interestingly, unlike equities and bonds that have explicit hard caps or at least implicit caps in the form of market cap and reasonable use of proceeds, token issuances have no ceiling. As a result, it’s plausible and highly probably that Algorand will end up raising WAY more than they need to finish this project. As such, Algorand is offering to buyback tokens at 90% of the issue price (if the clearing price is $1 or greater) OR $0.10 below issue price (if below $1) exactly 1 year after issuance. Effectively, buyers of ALGOs have a 1-year put option, but the value of that put option is based on the clearing price.

This introduces some interesting game theory dynamics. If you want to own the put, you have to participate in the auction. But some OTC dealers have been offering rights to an ALGO SAFTs token right issued via SAFTs are already outstanding from their initial raise last year, and these tokens do not carry these same put rights. But, you can buy the new ALGOs, sell them immediately, and retain the put for 1 year (the put doesn’t travel to the new buyer in a secondary sale). This may end up looking similar to credit default swaps, where the notion of “cheapest to deliver” comes into play (i.e. if ALGO trades down, those that hold tokens without a put may be able to push the token price higher as they know there will always be a bid from those who still own the put).

Regardless of how this plays out, this is yet another innovative financing option available in the token world, and is part of the reason so many investors are flocking to this space. Creative financing structures, and flexible tokenomics, are a blessing for both issuers and investors.

Notable Movers and Shakers

For those less tapped in to the happenings of the digital asset space, this past week may have looked uneventful - Bitcoin finished the week flat. However, there were two defining aspects of last week: Bitcoin’s volatility on Thursday, and the continuation of altcoin differentiation.

- EOS (EOS) hit the presses hard last week: Block.One announced their social media product “Voice”, Coinbase Earn added EOS to their education program that pays users in EOS to learn about the project, and EOS stakeholders voted to reduce the inflation fee by 80%. What does this translate to? A weekly peak of +24% right up until the June 1st announcement, with the project settling at +10%. Many were left disappointed, with hopes that the large war chest Block.One possesses would be put to use for a more vital product. Nevertheless, products are still being built - this is a step forward, not backwards.

- Monacoin (MONA) had an impressive week (+155%) that left many scratching their heads - what is Monacoin? The best comparison we can draw from is that it is the Japanese equivalent of Dogecoin - a community created coin in the early days of the space - to many it has no use, but the fervent community keeps the project alive. Last week’s move can be attributed to rumors that MONA was listing on CoinCheck - one small step for MONA, one giant step for the Japanese community.

- Projects like Cosmos (ATOM) and Ravencoin (RVN) each saw impressive weekly gains (+40%,+36%), with no evident news to boot. The main correlation that can be drawn here is that both projects were created after the infamous 2017 bull run. By missing the brunt of the bear market, each project has been afforded a “Tabula Rasa” - a clean slate to prove their worth regardless of market sentiment. It will be interesting to see how other projects born in the bear market fare in the coming weeks/months, as market sentiment continues to heat up.

What We’re Reading this Week

Those that find it challenging to purchase Bitcoin online may now only need to walk into their local grocery store to buy some BTC. After a large amount of consumer demand, Coinstar is now offering the ability to purchase BTC at 2,200 locations throughout the U.S. The technology for these kiosks is powered by Coinme, the first state-licensed Bitcoin ATM provider. Access to digital assets is one of the hurdles to widespread adoption and usage, and Coinstar is making it easier for everyday consumers to get their hands on crypto. You can check out if there’s a BTC ATM near you on CoinATM Radar.

Proof of Capital, a blockchain VC firm, released this report covering the remittance market and new technology firms that may usurp current incumbents. Remittances accounted for $550b with an average transaction of just $200; individuals are charged 6.94% in fees totaling $48b a year. The amount of remittances has been steadily growing as the number of migrants has outpaced population growth, leading to increased fees. With billions of dollars transacted through these systems per year, will users still pay such high fees for inefficient services? If solved correctly, the market for frictionless payments goes far beyond remittances with the potential to capture the entire global payments market.

Salesforce announced last week that it has rolled out a blockchain platform offering a plug-and-play solution for its clients to establish their own blockchain ledger. The goal of the initiative is to allow institutions better data sharing with their customers. Among its first client to adopt the technology is Arizona State University who will use the ledger technology to track and share student records. Although many crypto enthusiasts are against private blockchains such as Salesforce’s, the benefits to institutions are obvious for decreasing back-office functions and increasing customer trust. The full blockchain offering will be widely available in 2020.

Last week Yahoo Japan launched Taotao, its crypto trading platform, previously known as BitARG which they acquired last year for a purported $19m. Taotao, which is branded under the Yahoo Japan umbrella, has been approved for a crypto exchange license by the FSA. As a crypto-friendly jurisdiction, Japan is the perfect market for Yahoo to launch its exchange in, additionally, the Yahoo Japan brand will bring new investors into the ecosystem.

Kin, the messaging app which is being investigated by the SEC for its 2017 ICO, launched a legal fund designed to “fight the SEC in court”. The fund is being maintained on Coinbase’s custody platform and contains $5m from Kin. The Kin team has made the concerted decision to fight the SEC’s potential enforcement action head on and force a legal decision in court on the status of cryptocurrencies. While we can’t predict the outcome of Kin’s legal battle, the ramifications of further legal clarity on digital assets would be game-changing.

Ernst & Young’s blockchain product, which runs on Ethereum, is being used to authenticate wines imported from Europe to Asia. The e-commerce platform will be used by hotels, restaurants, cafes and consumers. In addition to tracking authenticity, the platform is also used for logistics and payments. We’ll drink to that!

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

call us now at (424) 289-8068.

.jpg)