Many investors in and out of digital assets woke up on May 21st to read this article in Bloomberg. Those not in the digital assets community probably choked on their coffee when they saw close to a 7000% return in just 1 year for Mr. Thiel, Alan Howard and Louis Bacon via their investment in Block.one.

As fellow investors, we congratulate Thiel, Howard, and Bacon because this type of success doesn’t happen often. In the end, they were rewarded for putting their capital at risk and it paid off. Bitcoin’s price resurgence over the last 3-4 months has reignited mainstream media interest in Bitcoin and consequently the rest of the cryptoasset industry (see 60 Minutes); people with no previous knowledge of crypto are starting to look into Pandora’s Box again and their expectations may be skewed by these types of headlines.

Back in 2017, these types of cryptocurrency returns were “normalized” with the crypto ecosystem; activities such as pump and dumps of early pre-sales tokens created significant outsized returns that became expected by those in the community. This caused many retail investors to come in rushing with caviar dreams and champagne wishes after hearing these exorbitant return numbers.

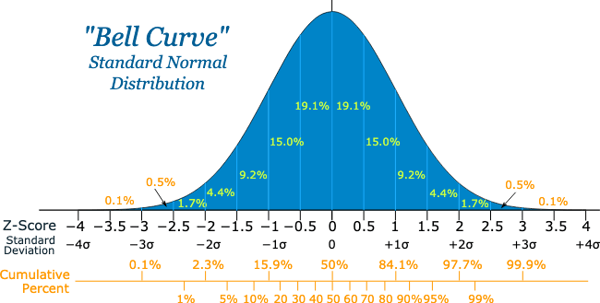

Throughout 2018, those in the digital asset ecosystem came to understand that 6000% returns were the outlier (the 0.5% or 0.1% on both sides of the Bell Curve), not the 19.1% within the Bell Curve that is more of a probabilistic return pattern. After 2017's unsustainable rally that was prolonged into the first quarter of 2018, leading to its subsequent capitulation, it's understandable if some people question this entire space and the returns generated thus far in 2019.

A lot has changed since in just a year's time. During the recent market capitulation the occured these last 4-5 quarters key infrastructure for the digital assets ecosystem was built to support a flourishing market-place that did not exist during the last crypto “bull run”. However, with the many improvements in the space - consolidation of exchanges minimizing arbitrage plays, information services and research providers reducing “information asymmetries”, and additional regulatory oversight - it is expected that return profiles going forward will be moderate compared to 2017.

Overall, the returns made in 2017 and 2018 were on hopes, dreams and white papers. For the past 2-3 quarters the industry has matured, the infrastructure has hardened and returns that are occuring now are built upon more substantial ground.

As Bitcoin is only 10 years old and the majority of other cryptoassets are half that age it’s worthwhile looking at investor expectations in general to see if there are corollaries to more general, traditional markets; hint, there are.

Joshua Kennon at The Balance does a great job discussing the role of expectations of returns from traditional asset classes:

One of the main reasons new investors lose money is because they chase after unrealistic rates of return on their investments, whether they are buying stocks, bonds, mutual funds, real estate, or some other asset class.” This applies to digital assets as well; the 2017 run up of Bitcoin brought along many of the “alt-coins” for the ride, creating unrealistic rates of returns in investors minds. For many first time, new investors, they enter into a position, see it go up and get a bit of irrational exuberance.

These lofty return expectations are not limited to the new digital asset frontier nor to retail investors in traditional markets as Christine Benz from Morningstar alludes to: “It's certainly a mistake to try to predict the market in an effort to determine whether, when, and how much to hold in stocks and other asset classes. Even professional investors have struggled with tactical asset allocation, casting doubt on the ability of individual investors or even financial advisors to outperform strategic asset allocation with the approach.

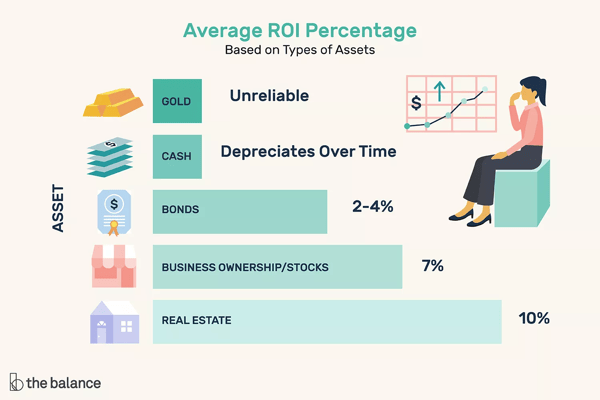

As Benz states: “Investors with very long time horizons of 20 to 30 years or longer can reasonably assume that market returns will run in line with their very long-term historic norms: 8% to 10% for stocks and half that amount for bonds.”

So what are “reasonable expectations of returns” in crypto?

As this is still a new emerging asset class, this question is difficult to answer. The calculations and models associated with P/E took decades to perfect after years of data capture and analysis. Those same types of models and valuations schema are being created today, in real-time - by professionals with finance and technology backgrounds. Ideas around network effect, velocity, sunk cost analysis and much more are being used and tested to find a fair value.

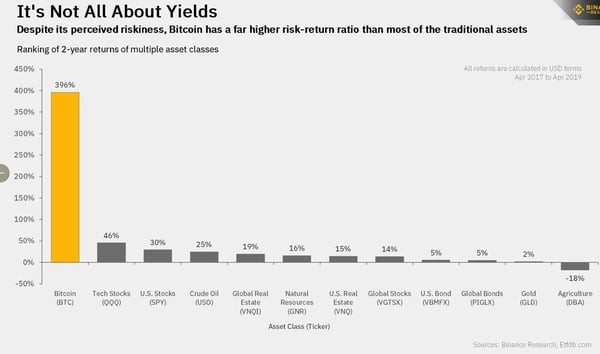

The crypto asset with the most historical data is Bitcoin with its ten years of existence. Research provided by Binance, a cryptocurrency exchange, shows the two-year return profile for Bitcoin hovering around 400%. This outpaces other more “traditional” markets, including the QQQ, one of the best established ETF’s in the world that is heavily focused on the tech sector, by almost 10x. Should this be used as the “expectation”? Hard to say right now.

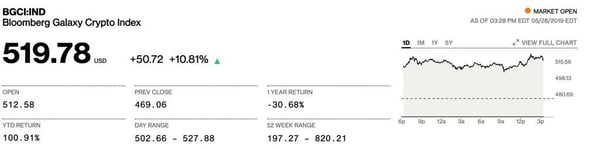

Indexes are attempting to provide benchmarks, such as the Bloomberg Galaxy Crypto Index, attempting to create a standard against which the performance of other cryptoassets and managers can be measured. Two years ago during the 2017 bull run the industry did not have these types of evaluation tools.

As you can see in the chart, the broad-based crypto market has returned close to 100% YTD, lead by the rebound in Bitcoin. Tools like BGCI and their associated performance gives investors a sense of how the broad based market is performing, in effect setting more data driven, proper expectations for their capital allocations.

Conclusion

In the end, we encourage more discovery into digital assets and blockchain technology. We see the positive momentum in this space by both professional and individual investors. Large institutions are building key infrastructure in this space and 185M people, of which 50% are below the age of 30, play Fortnite using digitally native currency called V-Bucks; that demographic is a few years away from having a major impact on our broad based economy and the writing is on the wall.

It is important to manage expectations for those currently, and those beginning to review investing in this asset class. Seeing headlines about 6000% gains in a year would get any person at least somewhat interested in understanding how or why this happened, but providing perspective and rational thinking is critical to the overall growth of the ecosystem as we continue to broaden the base.

To learn more or talk to us about investing in digital assets and cryptocurrency

call us now at (424) 289-8068.