What happened this week in the Crypto markets?

Bitcoin rallied another 10% last week; +65% MTD; +135% YTD

Most people who dedicate their careers to blockchain and digital assets come from the technology world. To them, these returns may look normal. The Arca team, however, hails from the traditional financial world. We built our careers on risk profiles that look very different than crypto, where a 10% monthly move was an outlier, let alone weekly, and a 30% yearly move would be the 99th percentile.

So before we get into what is happening in crypto, and why, we understand that these numbers don’t make sense to the majority of investors. Large positive returns scare investors just as much as large negative returns, because the assumption is that the risk one must take to generate these returns is too high to warrant a serious investment.

But it’s important to take a step back and remember that this asset class is tiny. Total Bitcoin wealth is under $150 billion in USD terms, and the entire digital assets industry is less than $300 billion in aggregate -- and these insignificant numbers are where we stand after a 100% rally. For comparison, Apple (AAPL) has a market cap of $823 billion. As such, the smallest of inflows into crypto, or a lack of supply, moves the needle a lot.

As investors contemplate allocating to this space (and make no mistake about it, they are ALL contemplating investments into this space), you have to ask yourself one question: Do you want to move the needle or watch it move?

Four reasons to answer the question “Why is Crypto Going Up?”

1) The inflows into crypto are real. We’ve discussed the positive backdrop for months, but to save time, here is a list of incumbent companies that are now having a direct impact on inflows into digital assets:

- Fidelity

- Nasdaq

- NYSE

- E-Trade, TD Ameritrade, eToro, RobinHood

- IBM

- AT&T

- Starbucks

- JP Morgan

- Samsung

- Facebook

And these behemoths aren’t just influencing investment inflows -- there is an inflow of developers and talented business professionals which is accelerating the pace of innovation. As money flows into this tiny asset class, there is a “buy the dip” mentality that seems to never manifest itself anymore because there is too much demand to generate even the smallest of dips. While few expect crypto to move higher in a straight line, the trend higher is hard to deny simply based on demand outpacing supply by a significant margin.

2) Global Equity & Debt Markets are in a death spiral: The only problem is, the equity and corporate bond markets don’t seem to know it yet. Despite escalations in the trade war rhetoric between the U.S. and China, an inverted yield curve (globally), a fast depreciating Yuan, an unstable leveraged loan market, a wishy-washy Fed, and insanely rich corporate valuations, somehow the S&P 500 index stands less than 5% below all-time highs.

Take our opinions with a grain of salt. Like most people in crypto, global market instability was one of the factors that led us here in the first place. To get a non-crypto focused opinion, here are thoughts collected from Cantor Fitzgerald's recent client notes:

What are upside U.S. equity catalysts? Short of an unexpected monetary policy reversal, we see few catalysts for a continued global equity rally. Global fundamental weakness has continued to emerge with few bright spots changing the trend. U.S. data is as good as it gets and the tailwinds from tax cuts will begin to wear off in the second half. Headwinds from the trade war will persist deep into the second half of the year. - May 16, 2019

Honestly, all we can say right now is ‘come on,’ why would one want to own equity risk here given a pronounced slowdown in global growth, rich valuations in the context of flat earnings growth (at best), and an unraveling of the trade narrative. - May 20, 2019

We think investors ought to seriously consider the possibility that the 35-year equity bull market run, which began after the completion of the Volcker rate hikes, may be over. - May 23, 2019

This narrative by itself might not suggest a year in which equities are +10-15% and crypto is +100%. But only a fraction of investors need to pull a little bit of money out of equities or corporate bonds and deploy some of it into crypto before the dam breaks. And we’re already seeing cracks.

3) China matters a lot more than the US when it comes to crypto. For almost a decade, Kyle Bass of Hayman Capital has been ringing the alarm bells in China. His most recent note to investors details the trouble that China is facing with its own currencies. As Bass states:

Remember when Iceland, Ireland, and Cyprus fell like dominos on the front-end of the European banking crisis? The primary determinant of the sovereign’s failures in each case was the fact that each country had allowed their banking sectors to grow to almost 1,000% of GDP. A small bump in the economic road could cripple the sovereign, forcing it to intervene and save bank depositors. Hong Kong is in as precarious a situation as Iceland, Ireland, and Cyprus were leading up to the crisis. In fact, Hong Kong’s banking system is one of the most levered in the world at approximately 850% of GDP (with 280% of GDP being lent directly into mainland China).

If you are currently a saver with your savings or investments denominated in HKD, why on earth would you not convert to USD and earn an extra return while also avoiding a catastrophic currency devaluation? Investors must pay keen attention to the balances and imbalances that matter and avoid listening to “others” telling them that everything is going to be fine. One only needs to look back at major dislocations in history to learn that the architects and keepers of the sovereign have no incentive to warn investors of the risks.”

Meanwhile, Arthur Hayes of Bitmex goes even deeper into the issues in China, but instead of focusing on the USD as the safe haven, notes that BTC may actually be the safe haven of choice for many Chinese citizens:

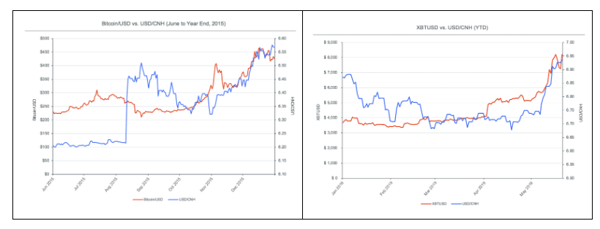

Chinese people have no illusion about what is actually happening. Unlike their American counterparts, ordinary Chinese people do not trust the government. Americans love America. Walk around an American city, and you will see countless people wearing American flag paraphernalia. Walk around a Chinese city, and you are more likely to see a Balenciaga handbag than someone rocking the Chinese flag as a fashion statement. China has devalued and revalued the Yuan multiple times since the early 1980s. This is not lost on the population. The PBOC has kept the Yuan relatively stable since early 2017. They even made moves to actually tighten credit conditions. However, the trade war changed all that, and now they are printing money like it’s 2008. That pressure will build around the exchange rate, and at some point, either the PBOC tightens credit and slows GDP growth, or devalues. Chinese asset holders are not stupid. They see the writing on the wall, and as the CNY has recently crept higher towards the magical 7.00, Bitcoin exited the doldrums and more than doubled.

Bitcoin’s ascent has followed the Yuan’s devaluation closely in 2015 and again today

It’s hard for US Investors to fathom how restrictive capital controls in other countries can be, but China’s capital flight is certainly aiding the crypto rally. As we discussed last week, crypto may actually be a risk-asset and a safe-haven at the same time.

4) Awareness is growing. Warren Buffett famously avoided purchasing equity in many of today’s most profitable and well-known technology platforms (Facebook, Amazon, Netflix, LinkedIn, Google, Twitter, etc) because he couldn’t figure out how to value these new businesses. You couldn’t use traditional cash flow models because these companies had no revenues or even business models in the early days, let alone profits. But as these technology giants grew, so did their business plans. Today, it’s much easier to value these companies, partly because every investor is now keenly aware of them.

Similarly, many passed on digital assets due to the inability (or unwillingness) to think about complex network effects and wealth redistribution amongst users and developers. But people that engage are not only opening up their minds to new technology and value creation, but they are likely opening the minds of several friends and family members too. Almost every crypto enthusiast becomes an evangelist to the non-crypto world.

Last week, two of the three 60 Minutes segments strengthened the view of digital asset supporters, and led to greater awareness and adoption for those that are not already in the ecosystem. The first focused on the rampant money laundering of hundreds of billions of dollars through traditional US and foreign banks, and the second focused on the rise of Bitcoin. These were not meant to be related, but they are completely intertwined. Both led to awareness of the problems with the current banking system, and the next generation solutions.

Scott Purcell, CEO of Prime Trust (a financial services company focused on digital assets), sums it up perfectly in a recent blog post:

Is the market volatility associated with a recovery part of a sustainable upswing as volumes increase and news is digested? Or a sign of blatant market manipulation and a bubble? I have no idea. Regardless, I think this is great for the future of blockchain. The general excitement and good press (not to mention the profits that key industry participants are making) keeps venture capital flowing into the space, which is enabling entrepreneurs to continue working on exciting, industry-changing businesses targeting capital markets, real estate, medicine, and other sectors.

So whatever ultimately becomes of the value of BTC or ETH that someone may have in their IRA or savings account, the future continues to look great for fractionized assets, trading of, and liquidity for, private securities, and data storage/access services we can barely begin to imagine. In this regard, we are very much at the start of a transformative period of time that can only be compared to that of the internet or the industrial revolution.

Notable Movers and Shakers

A rising tide does not always lift all boats, and this was evident last week as the market continued to separate the “haves” from the “have nots”. While Bitcoin rose 9% last week, there was broad divergence among the Top 100 digital assets. Whereas 39 of the Top 100 outperformed Bitcoin, 60 did not - Bitcoin market dominance remained relatively stable at 57%. While some tokens may have moved without rhyme or reason, others moved based on real information and allowed for notable differentiation in the market:

- Bitcoin Satoshi Vision (BSV) experienced a huge spike on Tuesday (+100%) following the news that Craig Wright underwent copyright registration for the Bitcoin whitepaper and original code. By week’s end, the price settled at +67%, making it one of the top movers for the week. It is worth noting that the Copyright Office responded stating that they don’t investigate the validity of claims for a pseudonym's work.

- Unus Sed Leo (LEO), the utility token created by Bitfinex to cover the Tether shortfall (as well as provide functionality to the Bitfinex ecosystem), listed on Monday at $1.00/LEO. Since then, the token has traded up 48%, with corollaries being drawn between LEO and the incumbent BNB token offered by Binance.

- Litecoin (LTC) had a strong second half of the week, finishing up 22% by week’s end. The upcoming halving in August has created a higher established floor for Litecoin, as miners (the biggest sellers of any PoW-mined coin/token) have the largest control of sell-side pressure. With the mining rewards being cut to 12.5 LTC (from 25 LTC), miners may be more hesitant to sell at these levels, as the week low price ($85.23) will soon become unprofitable. Also noteworthy is that Litecoin is consistently in the top-5 in volume in the cryptocurrency space, and has garnered a lot of attention in the last few months.

What We’re Reading this Week

Facebook officially announced that it will be setting up its GlobalCoin initiative in 20 countries by the first quarter of 2020. FB has apparently been meeting with officials at the US Treasury, and Zuckerberg has met with the governor of the Bank of England to discuss feasibility and risks. There are still many questions about how the cryptocurrency’s technology works and how it will be used but the world waits in anticipation as Facebook attempts to pull off this massive pivot.

You read that right - last week crypto startup, Block.One paid out $6.6m to its earliest investors who contributed $100,000, a 6,6567% return. Block.One is most well-known for raising $4b in an ICO for smart contract platform EOS in 2018. The EOS platform launched a little under a year ago but been criticized for not making as much progress as other projects, but has promised a major announcement on June 1.

According to inside sources, the Financial Action Task Force (FATF) could soon require additional information if customers send funds out of exchanges beginning next month. Requirements like these are already present in the banking system: when a customer transfers out assets, the bank must provide the receiving bank with information on that customer and the transaction. Besides all the potential ways users could circumvent such regulations, rules like these place undue burden on customers, defeating the purpose of crypto - to move money seamlessly.

Regulation is Already Hurting Crypto Businesses

Financial services firm, Circle, which raised $250m+ from investors, has had to make some recent changes. Last week, Poloniex, the US-based exchange owned by Circle, announced it was delisting 9 assets, including well-known prediction markets project Augur (REP). A few days later, CEO Jeremy Allaire announced that Circle had laid off 10% of its workforce. Regulatory issues and restrictions were cited in both instances. Many have long been worried about the potential for regulation to stifle innovation, Anthony Pompliano probably summed it up best: "This confirms what I would have assumed — crypto company leadership is not going to wait around for regulatory clarity in the US. They are going to continue building their companies and simply identify jurisdictions that are crypto friendly. Sadly, we are forcing some of our country’s best and brightest to focus their efforts building elsewhere, even though the US is still their desired destination." Fred Wilson of Union Square Ventures reiterated this:

AT&T announced last week that it would allow customers to pay their phone bills in cryptocurrency through the BitPay app. As the first major US mobile carrier to accept cryptocurrency as a payment option, AT&T stated that “we have customers who use cryptocurrency, and we are happy we can offer them a way to pay their bills with the method they prefer.” This has many in crypto excited as we continue to see more mainstream acceptance of crypto as a legitimate payment method.

This piece explores the strategy of playing to one’s strengths over weaknesses through the lens of building a business in the tech world and in crypto. Specifically, protocols need to match their strengths with use cases, instead of attempting to check every perceived box (security, scalability, decentralization). The perceived “weaknesses” of assets like Bitcoin or Ethereum, are simply trade-offs that make for stronger systems that serve very specific use cases that will guarantee their permanence.

Crypto-gaming project, The Abyss, has teamed up with Epic Games, the creator of ‘Fortnite’, to boost game development. Although the exact details are not public, the basic premise is that developers who build games for The Abyss using Epic Games’ Unreal Engine (a game development platform) will receive favorable terms.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

call us now at (424) 289-8068.

.jpg)