What happened this week in the Crypto markets?

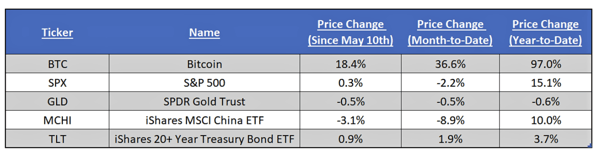

Another week of crypto gains, and equity losses

The S&P 500 lost 2.4% on Monday, its biggest one-day loss since January, after Trump raised Chinese tariffs on $200bn worth of goods and China fired back with $60 bn of their own against US imports. Asian equities similarly lost almost 4%. While global equities recovered slightly by week-end, clawing back some of the early week’s losses, the one-day move on Monday set the tone for the “risk assets” vs “safe havens” debate. Not surprisingly, gold rallied, US Treasuries rallied (now almost back to the 2019 low yield), and the VIX soared.

What may be surprising, however, is that crypto also rallied last week, with Bitcoin rising 14% week-over-week, and many other well known digital currencies and utility tokens rising 20-30%.

Bitcoin (and all of crypto) continue to outperform all asset classes

Is Bitcoin a Risk-Asset or a Safe-Haven?

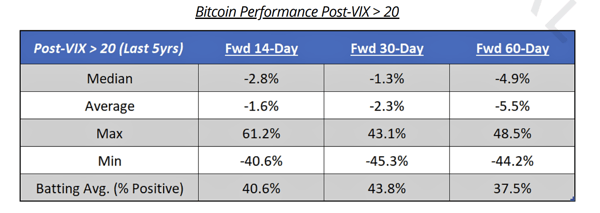

We talk at length about how crypto as an asset class remains completely uncorrelated to all other asset classes. This makes it a great portfolio diversifier by reducing overall portfolio risk while simultaneously giving investors a chance to achieve outsized returns. That said, we've seen this play out in the past where crypto ignores equity / rate volatility for short periods of time while the crypto community rejoices, only to watch crypto ultimately trade down swiftly weeks/months later. In fact, our friends at Delphi Digital just corroborated this statement further with some timely and insightful data:

"Over the last five years, bitcoin has lost roughly 2.3% and 5.5%, on average, in the 30 and 60 days following a jump above 20 for the VIX".

So is Bitcoin a risk-asset or a safe haven? The answer may actually be both.

First, let’s examine the obvious. Bitcoin and other digital assets are still not widely used as they were designed. Adoption is growing, but we’re a long way from the velocity issues that kick in when something turns into money and is spent/received so frequently that prices stabilize. As of now, all digital assets including Bitcoin remain speculative risk-assets that, one day in the future, may become a store of value or a medium of exchange if enough people speculate on them today. Viewing Bitcoin and other digital assets as “early-stage technologies” helps rationalize and contextualize the outsized returns produced year-to-date, and potentially in the future. There should be little doubt that these assets are risk-assets.

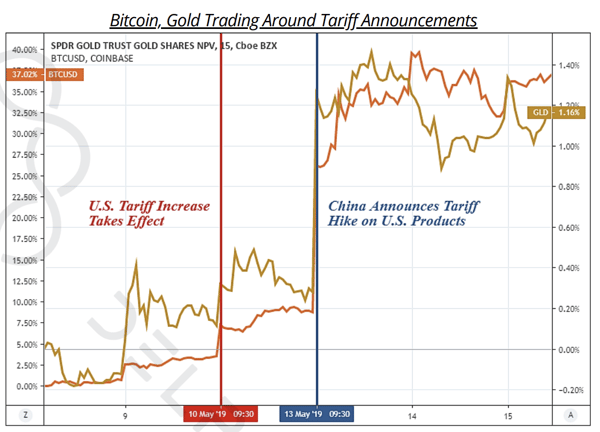

The less obvious is that, if crypto does keep rallying in the face of equity declines, then it becomes plausible that some digital assets are not only uncorrelated to other asset classes, but now act as a hedge against the global market itself. It’s WAY too early to say this definitely of course, as a small bout of volatility is not the true test of a safe haven nor are the markets even remotely stressed enough right now to warrant a true “flight to quality” rally. But much of this year’s crypto rally can be traced back to the absurdity of Fed Chairman Powell’s decision to reverse course, the Modern Monetary Theory (MMT) narrative that is creating further political uncertainty and instability, and the actions of corrupt governments across the world. With that backdrop, it’s not unreasonable to think that Bitcoin’s spike last week was caused by further political interference. Again, our friends at Delphi Digital provide data to support this argument, showing that both Gold and Bitcoin spiked at the same time following last week’s tariff news.

Both Bitcoin and Gold spiked following Tariff announcements

There will of course be people who throw water on this notion. But those who argue that Bitcoin is too volatile to be a safe-haven, or reference the 70% declines in 2018, are missing the larger point. Many confuse what a “safe-haven” really is. A safe-haven investment is not an asset that never goes down; a safe-haven is an investment that is expected to retain or increase in value during times of market turbulence. More literally, “Safe Haven” is defined as “a place of refuge or security”. US treasuries lose substantial value when rates rise, but few argue that US Treasuries aren’t a safe-haven. Similarly, protecting your assets against macro factors and corrupt, overleveraged governments is a form of safe haven as well.

The “Bitcoin Safe Haven Asset” just may be in transition as a reality for investment as we speak.

The Trend is Your Friend

Unpacking last week’s move in crypto further, while the large week-over-week and YTD returns are again extraordinary, there is good reason to believe that this can and will continue (albeit not in a straight line). As our friends at Bitooda recently said in a research note: “The bears have lost, and dips are to be bought until proven otherwise. Rising volume during the past rallies indicate that there is fresh capital being committed rather than a simple short-squeeze followed by momentum chasers. This is supportive of the change in sentiment.”

On point, following the huge rally the previous week, Bitcoin wasted no time last week as it pushed past $7000 and right to $8000 on Monday. Plenty of other crypto-assets followed suit, many of which hadn't rallied at all until this past week (XRP +27% and XLM +37% for example). In fact, this was the first week since April 1st where BTC actually UNDERPERFORMED the rest of the market. Naturally, we did see another 10%+ intra-week drawdown (late Thursday night), to remind us that this asset class is still not for the faint of heart and needs to be actively managed, but this sell-off was once again gobbled up quickly, and the market spent the weekend climbing right back towards $8000.

Every dip is being bought -- the Trend is Your Friend (until it isn’t).

Notable Movers and Shakers

In a week rife with news due to Consensus, the cryptocurrency space as a whole saw a +17% increase in market capitalization. As noted earlier, last week was differentiated in the fact that Bitcoin finally underperformed the market, allowing for individual projects to catch the spotlight:

- NewEconomyMovement (XEM) put on a stunning display, posting returns that leave some jaws on the floor (+62%). As with the rest of the space, some of this movement can be attributed to the “rising tide lifts all boats” mentality, but there was isolated fundamentals on full display: NEM took full advantage of the media blitzkrieg last week and announced their progress towards their Catapult upgrade, a much awaited 2.0 to their core protocol.

- ChainLink (LINK) continues to make impressive strides, finishing last week up 49%. At Consensus, CEO Sergey Nazarov announced that ChainLink will launch on the Ethereum Mainnet on May 30th. This project has been noticeably quiet with regards to marketing, as Sergey noted that there was nothing yet to market. This long awaited mainnet will continue to whip up a frenzy among supporters and we could be hearing much more from the Chainlink team in the near future.

- Ripple (XRP) finished the week up 27%, although at one point that figure was as high as +52.5%. The xRapid product, the XRP-powered cross border payments solution, launched in Argentina and Brazil (joining Mexico and the Philippines). Also of note Coinbase has enabled XRP trading for customers in New York (which has its own implications), and German stock exchange Börsse Stuttgart added a XRP Exchange Traded Note (ETN).

What We’re Reading this Week

The Spedn app, which launched at Consensus last week, will allow users to shop with their cryptocurrency at retailers like Crate and Barrel, Nordstrom, and Whole Foods. The project, a collaboration between Flexa and crypto-exchange Gemini, uses existing digital scanner systems like Apple Pay, in which a user scans a barcode from their phone to pay for items. Spedn supports Bitcoin, Bitcoin Cash, Ethereum and Gemini Dollars (a stabletoken). This is unique in that the merchants themselves don’t have to do anything differently to accept crypto as payment -- Flexa acts as a middleman to allow for seamless conversion.

Katie Haun of a16z’s Crypto Fund shared her thoughts on the Kik ICO and the SEC recent enforcement actions. Previously a federal prosecutor with the SEC, FBI and Treasury, Haun details the process by which the SEC decides to pursue an enforcement action and issue a Wells Notice as well as exploring potential outcomes for Kik.

This presentation from Circle Research, originally presented by Ria Bhutoria at Consensus last week, discusses the data problem prevalent in crypto. While many might believe that all data in crypto is public and free, Circle discusses the drawbacks of open data highlighting issues with data comprehensibility, integrity and accessibility. Making sense of all the data in the space is one of the major challenges that may be preventing institutional capital from entering.

Last week, Microsoft launched a decentralized identity tool on the Bitcoin blockchain. The goal is to allow users to share information about their identity, for example proving ownership of private keys. This is a big move towards decentralized identity, but more importantly it is significant that Microsoft has chosen to put resources behind building open-source tools like this based on the Bitcoin blockchain.

Last week a group of 50+ traders known as CORA met to discuss creating a “white list” for the OTC trading market. The current trading and OTC landscape lacks any kind of guidelines or standardization for KYC, documentation, and trade settlement, a result of the early-stage nature of the market. The group, which includes Jump Trading, Galaxy Digital and DRW’s Cumberland, aim to provide more professionalism and standardization in the industry, which will hopefully attract more traditional Wall Street groups to crypto.

A study from Chainanalysis last week found that 376 people own one-third of the existing Ethereum supply and 448 people own 20% of all Bitcoin. Besides the massive disparity in ownership, the research looked into whether these “whales” had any impact on price. Surprisingly, they found that assets in these wallets were hardly moved to exchanges and if moved, caused only a small amount of short-term market volatility.

In a tweet last week, Russell Okung of the LA Chargers and head of the NFL Players Association requested to be paid in Bitcoin. Crypto Twitter was all over Okung (we recommend checking out all the comments) and since then his feed has contained many tweets indicating to us that Okung has gone down the rabbit hole.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

call us now at (424) 289-8068.

.jpg)