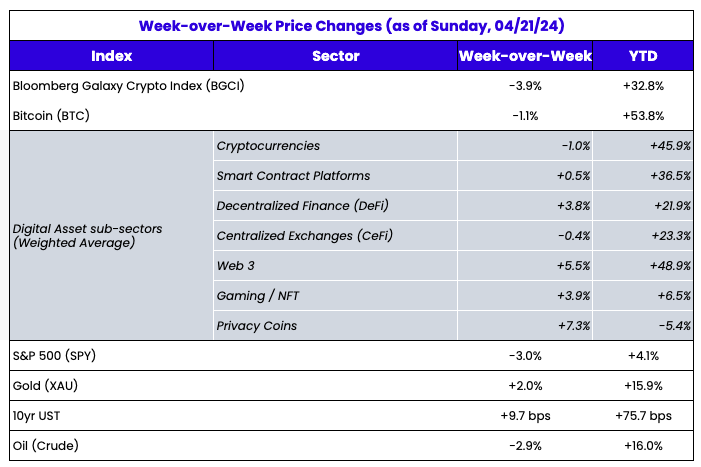

Source: TradingView, CNBC, Bloomberg, Messari

Middle East and Markets

Last week, we mentioned that the conflict in the Middle East was

not a factor that would ultimately drive digital asset prices and that there were other reasons behind the weakness in digital assets prices. Of course, that theory was tested again, as conflicts seemingly increased last week, and digital assets again dumped immediately upon the headline. Did we change our opinion?

Nope. We will reiterate that the conflict in the Middle East has no bearing on the direction of digital asset prices. I suggest short-term traders should ignore the conflict. There is little resistance right now, so a Middle East conflict headline is as good of a trigger as any to start selling, and it is working, though we were not shocked that it retraced. But, sometime soon, the market will be bullish once again. And those traders trained to sell on “war news” will get hurt because it won’t work. The Middle East conflict is a trigger in determining asset prices, but not a real factor.

So that begs the question…what is a driving factor of prices? Perhaps Bitcoin halving.

A Pre-Halving Analysis

Before the halving, many of our LPs and partners asked our opinion on what would happen when Bitcoin halved this week. Recall that Bitcoin’s block subsidy (the number of newly issued bitcoins paid to the miner of each block) decreased from 6.25 BTC to 3.125 BTC over the weekend. Consequently, the daily issuance of new bitcoins has decreased from ~900 BTC to ~450 BTC, lowering bitcoin’s annualized inflation to 0.85%. The halving is a programmed event on Bitcoin that occurs every 210,000 blocks, or approximately every four years. Bitcoin will undergo 30 more halvings over the next 100+ years.

The halving has typically been seen as the biggest BTC catalyst every 4 years. However, that is likely a false narrative, or at least incorrect from a timing standpoint. The halving in supply emission is a derivative effect and usually presents itself many months later. The rate of supply emission change each halving has gone down, which will eventually affect the supply/demand curve, but usually not immediately.

We have only had 4 Bitcoin halvings to date, and an N=4 event (really, N=3 because 2012 was too small) doesn't give much room for projection/extrapolation. And this halving, specifically, is very different than the ones prior for a variety of reasons:

- The Blackrock ETF has provided a significant bullish tailwind for the asset via inflows and interest, which will continue once they turn on the marketing spigot.

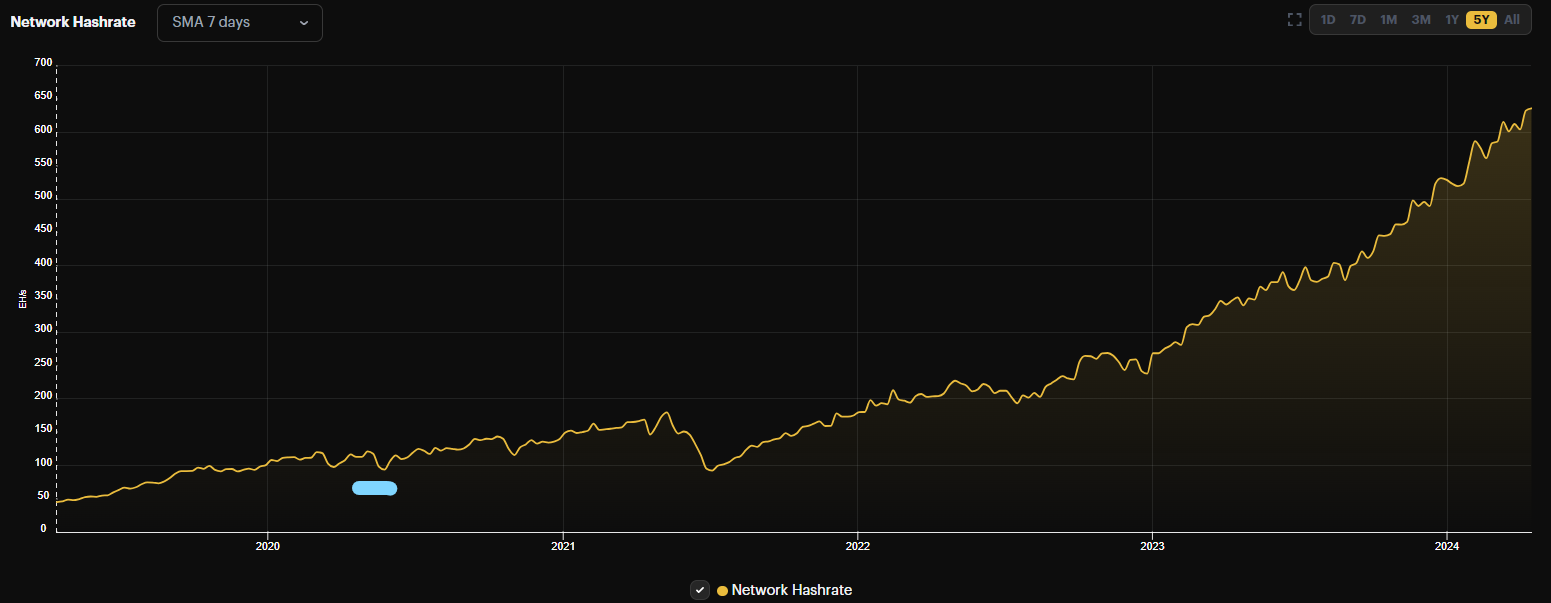

- Bitcoin miners are the most aggressive and consistent sellers of Bitcoin, but they are much more sophisticated today than in previous cycles. Many of the largest miners are now publicly traded companies, with investors, balance sheet disclosures, and mandates to protect capital. This cycle, we have seen this play out in real-time, as miners have been aggressively selling for the past few months. This is a significant break away from previous mining behavior, where miners tended to hold onto BTC pre-halving to crunch supply and sell it later after the halving.

- Miners now have a perfect avenue to sell, using Blackrock's create/redeem process to effectively sell their balance sheet at market price with limited difficulties. This order of magnitude is better for them than taking coins to exchange and praying that the market is in favor - the slip used to be rather severe in 2020.

Jubilee is an event coinciding with the Bitcoin halving, which upgrades the BTC core protocol to allow for PSBT/UTXO-based tokenization on the platform (codename; Runes). This has taken the space by storm in the past few weeks, as pre-Runes are trading at 50-150x multiples of where they were in February. For example, look at the price of $PUPS, the predominant pre-Rune asset. It went from $3.72 ($37 million market cap) on April 3, 2024 (10 days ago) to $38 ($375 million market cap). The effects of the pre-Runes trading frenzy have been felt in the mempool (the open bazaar of transactions that are waiting for a miner/pool to include them), with fees going from as low as 7 sats/byte to as high as 150 sats/byte (anecdotal observation). The increase in fees benefits the miners and is the long-term vision of Bitcoin, where the block rewards (see: subsidies) are effectively replaced by fees as the network becomes increasingly used.

In conclusion, nobody knows what will happen, and anyone who says they do in an absolute fashion is not being honest with themselves or the people they tell. Our best guess is that this is still a bullish event, and even more so due to:

- Miners selling “into the halving” to ETF products, as opposed to after (reduced headwind post-halving)

- Jubilee/Runes/Ordinals have provided an extra tailwind that Bitcoin has never had before (more turnover, throughput, fees, activity, etc)

- The Blackrock ETF in itself is a tailwind (at least, for the next 6-18 months - it can easily become a headwind if redemptions pick up)

- More eyeballs on BTC in general - traditional equity firms looking at Bitcoin mining stocks and valuing them in their way, crypto native folks bullish on Bitcoin as an asset seemingly immune to any further regulatory capture, etc

The most we can do is show up daily, watch as the above unfolds, and think of second and third-order effects.

So… that’s great, but what has happened in the three days so far post-halving?

The Bitcoin halving went smoothly this weekend, with

ViaBTC finding/mining the Halving block 840,000. However, the interesting takeaway is what has happened to the fee market.

Before the halving, fees were ~60-90 sat/vbyte. On the Halving block,

fees jumped to ~200 sat/vbyte, and have since ballooned to as high as 2900 sat/vbyte (as of this writing). ViaBTC made 3.125 BTC for solving the block (in subsidy block rewards), but made another 37.626 BTC in transaction fees, a significant increase in the fee rate (12x the subsidy!). This can wholly be attributed to the creation of Runes, which began on block 840,000. The etching of Runes (in chronological order) was seen as an ode to provenance, and the fee market for both etching (creating) and minting (basically buying) has skyrocketed.

This will be something to watch, with fees as a percentage of overall block rewards shooting higher. According to Galaxy Digital, over the 15 years Bitcoin has operated, fees have never comprised more than 12% of miner revenue (and that year, 2017, was an outlier; 3-6% has been the norm for several years). The immediate takeaway is that this is a huge boon to the mining industry, with top mining stocks squarely in the purview now. The BTC mining sector saw solid outperformance in the back half of last week. CLSK saw the largest outperformance, up 13% WoW, while CIFR was the largest underperformer, down 1% WoW. Hashprice declined from $116 to $104 due to the decline in BTC price.

It is also important to note that during the previous bull run, the hash price grew to ~$400 per PH/s. This was due to BTC price growth and mining rig shortages.

The second-order effect would be to monitor whether the fee market remains high over the next few days/weeks. This would be a direct KPI for the success of the BRC20--> Runes migration, activation, and the eventual follow-through of Bitcoin L2 / DeFi projects that enter the fold and participate in the action via service provider mechanics.

Overall, this was a very active halving event and one that stands out as unique from any other. The addition of Runes into the fold has created a new independent variable that has affected the immediate outcome, which has been higher fees and higher activity but no degradation to the flow of the chain itself.