What happened this week in the Crypto markets?

That Was Sudden

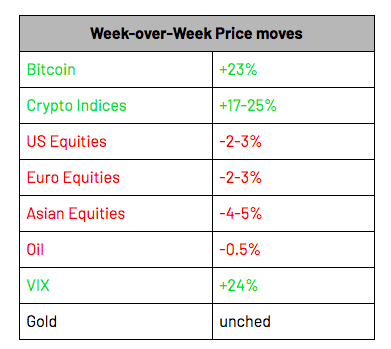

Global equity markets ran into a bit of a buzzsaw for the first time this year, after the U.S. announced it would increase tariffs from 10% to 25% on $200 billion of Chinese imports. So naturally, Bitcoin and the rest of crypto were... +23% week-over-week?

Take a look at the above numbers again.

We’ve been beating the "Crypto is not correlated to any other asset class" drum for awhile now, but even we were shocked by the moves last week, especially in the face of negative crypto-specific news to go along with the equity volatility.

Amidst the march to new year-to-date highs, the crypto rally was actually bookended by two sharp but short-lasting intra-week selloffs. On Tuesday night, the largest crypto exchange in the world suffered a hack, as over 7,000 Bitcoin (~$42mm) was stolen from multiple customer accounts on Binance. Naturally, the crypto market dipped, but this was a surprisingly quick 3% selloff before buying resumed. Later in the week, following another huge spike higher on Saturday morning, crypto once again sold off on Saturday night, this time falling almost 10%. But once again, the dip was gobbled up quickly and the market seems determined to claw back these losses once again.

Watch for more crypto rallies (and specifically a Bitcoin rally) as the market & media continue to heavily weigh in.

Bottled-Up Demand

The financial media scrambled all week to explain why Bitcoin and the rest of crypto was outperforming every other asset class (we were quoted here and here for instance). But for those of us focused on the long-term, none of this (other than the speed of the acceleration) should be a big surprise. It's been building for months.

Recall, the heart of this rally started on April 1st with a one-day 18% BTC rally. Very simply, buyers outweighed sellers, and market makers felt the imbalance pressure so they took their markets higher, which triggered algos, stop losses and liquidations, which only added more fuel to the buying pressure. In other illiquid asset classes like High Yield bonds or Emerging Market equities, this type of a quick burst would last for a few days until the market reached a more balanced equilibrium. What's surprising is that 40+ days later, in the face of a LOT of bad news (Binance hack, Bitfinex/Tether solvency issues, new FinCEN guidance), we've now rallied another 30% and still may not have found that equilibrium yet.

This rally has sustained because the positive events surrounding crypto have outweighed the negative risks for months. More importantly, the negatives are largely one-off “black swan” type events that create tail risk when they occur, but are not persistent (exchange hacks, negative SEC rulings, equity market implosion) whereas the positives are long-term game changing events that lead to sustained growth (improved infrastructure, large financial incumbents entering the space, better UI/UX, inflationary global currencies). Further, in some ways, the political instability is actually fueling the rally further. Everything from the rise of modern monetary theory (MMT), to the Fed's continued manipulation, to increased concerns around capital controls and property seizure are bullish for a non-sovereign, supply-capped digital store of value.

This is what happens when all of the good news is ignored for a full year and gets bottled up. We’re now in a period where all of the bad news is largely ignored and brushed off. However, it’s important to keep some perspective. Even after this rally, the market is just now back to November 2018 levels. Bitcoin may have risen 100% in a few months, but it's still -65% from ATHs (meaning, a 100% rally barely makes a dent in the scheme of last year’s losses).

A Healthy, Yet Violent, Rally

During a week where Bitcoin rallied 23%, it’s important to recognize that there were still plenty of other winners and losers. This was not a broad-based market rally. Many tokens ended the week sharply lower, and remain in deeply negative territory MTD. Binance Coin (BNB), for example, fell 10% last week (before rallying back with the market), a move that makes sense following the Binance hack.

As a result of this bifurcation and dislocation, correlation between digital assets has broken down. These are signs of a healthy and maturing market, even though the overall market is skyrocketing and creating lofty headline numbers that may scare investors as much as excite them.

Looking ahead, this week is Blockchain Week and Consensus, one of the largest crypto conferences of the year. Thinking back to 2017, the market rallied around Consensus when crypto was all hype and no substance. In 2018, Consensus had no real effect at all, as rampant fear drowned out improving fundamentals. We're now heading into 2019’s event with mixed feelings -- which should help separate hype from substance.

Notable Movers and Shakers

In a week that brought back not so distant memories of the 2017 bull run, we again saw Bitcoin outpace the majority of the market (+24%). These rallies in back-to-back weeks have brought Bitcoin into the public spotlight again, but there were sizable, uncorrelated movements within the broader crypto market that went relatively unnoticed.

- Binance Coin (BNB) fell 10% last week before ultimately rallying back to gain 2% last week, despite its exchange being hacked. Early findings indicate that the hack originated from users who were phished, not as a result of a critical failure in the exchange software. To those who find it odd that BNB is up on the week after a negative event, it is worth noting that the main market for BNB is against BTC (~+45%), so while it is up 2% against the dollar, it is down 18% against Bitcoin.

- Chainlink (LINK) finished the week strong (+31%), following two partnerships announcements with Hedera and IOST. Chainlink is a middleware solution, offering decentralized oracle services that have potential applications in both blockchain and non-blockchain based products. With rumors of their mainnet swirling ahead of Consensus, public sentiment has been high as of late.

- Ethereum (ETH) finished the week strong, rising +17%. News broke Monday that the CFTC is ready to approve Ethereum Futures, a positive sign for the space as a whole. This news was quickly overshadowed by Bitcoin’s significant strides but should remain on everyone’s radar as a net positive that offers more credibility to both Ethereum and the blossoming space.

What We’re Reading this Week

Fidelity Investments announced last week that in addition to its custody offering, the wealth management giant will also provide institutional investors the ability to trade Bitcoin through its platform. The focus on institutions sets Fidelity apart from Etrade and Robinhood, brokerages that offer crypto trading to a retail client base. Fidelity implied that the services they are offering are based on their clients needs - indeed this is very bullish for crypto if institutions that are looking for ways to buy, sell and hold Bitcoin.

According to a source from the CFTC, the group is seriously considering allowing the creation of Ethereum futures contracts, similar to the BTC contracts currently offered through CBOE and CME. Adding contracts for Ethereum would theoretically allow institutions to get exposure to Ethereum without having to physically purchase and store the asset. There is also some concern that the CFTC may give them regulatory authority over the Ethereum spot market if such futures markets are approved.

The Financial Crimes Enforcement Network (FinCEN) released guidance last week for companies, dapps and individuals that may be considered money transmitter businesses (MSBs). They describe MSBs as those that “accept and transmit value”, which would require these groups to comply with the Bank Secrecy Act and perform AML/KYC. The implications of this guidance are far reaching and affect wallets, decentralized exchanges and even dapps.

What positive effects could the large number of 2019 tech IPOs have on digital assets? Vision Hill dives into the possibility that with all the new capital distributed to early employees and VCs of these tech behemoths - Uber, Lyft, Slack, WeWork to name a few - some of that capital will end up in digital assets. Only time will tell what the distribution of this new wealth will look like, however, reinvestment in digital assets is highly likely as such a young and developing market.

In conjunction with blockchain platform, OpenCerts, Singapore will become the first country to use blockchain on a national level to issue digital certificates at local schools. The initiative provides graduating students with a cryptographic proof that can be used to verify their school credentials without having to order certified copies directly from the school every time they apply for a job or further education. The project is being hailed as a “practical way” to harness blockchain technology.

Figure, the startup founded by ex-SoFi CEO Mike Cagney, has closed a $1b credit line on the blockchain. The credit line issued by Jeffries will be extended periodically and is secured by Figure’s home equity lines. Figure’s platform facilitates the issuance and funding of home loans all on the blockchain. This credit line is an important step forward in securitizing these types of assets via blockchain technology, massively reducing costs and increasing efficiency.

This was the actual proposal from U.S. Congressman Brad Sherman last week. Ignoring the reasoning for proposing such legislation (crypto circumvents the U.S. dollar’s power internationally), those who understand the basics of crypto know that an outright ban is preposterous, if not impossible. Crypto is decentralized and therefore outside the influence and reach of government entities including the U.S. government, and bans on crypto only stifle innovation.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)