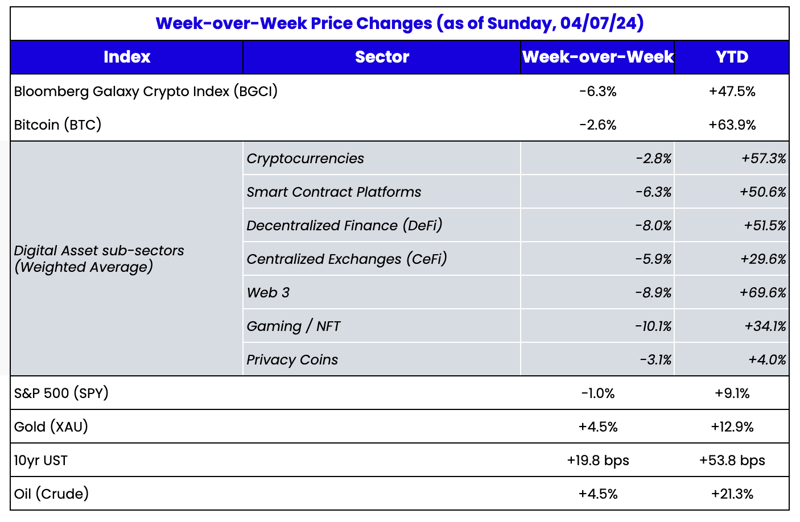

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari

An Interview with Sasha Fleyshman, Arca Portfolio Manager

When we launched Arca six years ago, we put together an eclectic group of eager investment minds, without a clear understanding of which skill sets would ultimately shine. Not only did our team evolve their skills, but the market evolved, and over time, many of our portfolio members gravitated towards specific areas of expertise and interest. You’ve heard from me many times over the past six years, but over that time, many of you have also heard from others from Arca who have completely different and unique perspectives on the market.

Sasha Fleyshman has been with Arca since its inception. He graduated from an undergraduate program with a chemistry degree and immediately started working his way through Arca, from trade operations to trading to portfolio management. Today, Sasha is one of the foremost experts on NFTs and blockchain gaming. Recently, we picked his brain on the NFT space.

Can you offer a macro view of the NFT space? What’s happened to the NFT space, generally speaking, that makes it more interesting and financially appealing today than it was last year?

Fleyshman: NFTs have had a rough stretch over the last 12-24 months. Whereas previously, the attrition/atrophy in the market could be attributed to a broader risk-off stance coupled with NFTs being seen as a “down the risk curve” asset, we are in a risk-on environment currently. NFTs have not caught any attention in this new market environment due to a confluence of factors:

- Most current NFT projects are hollow shells of value, similar to the dot-com bubble. 95%+ of them offer zero terminal value, and the other 5% are being swept up in this negative sentiment.

- The growth of memecoins has severely constricted the available capital pathways that would typically be pointed at the sector. Many argue that memecoins are NFTs without the fluff and with more liquidity - and who can blame them? When you compare a product that promised value but never delivered to a product that doesn’t promise anything other than social coordination, what is the difference, really?

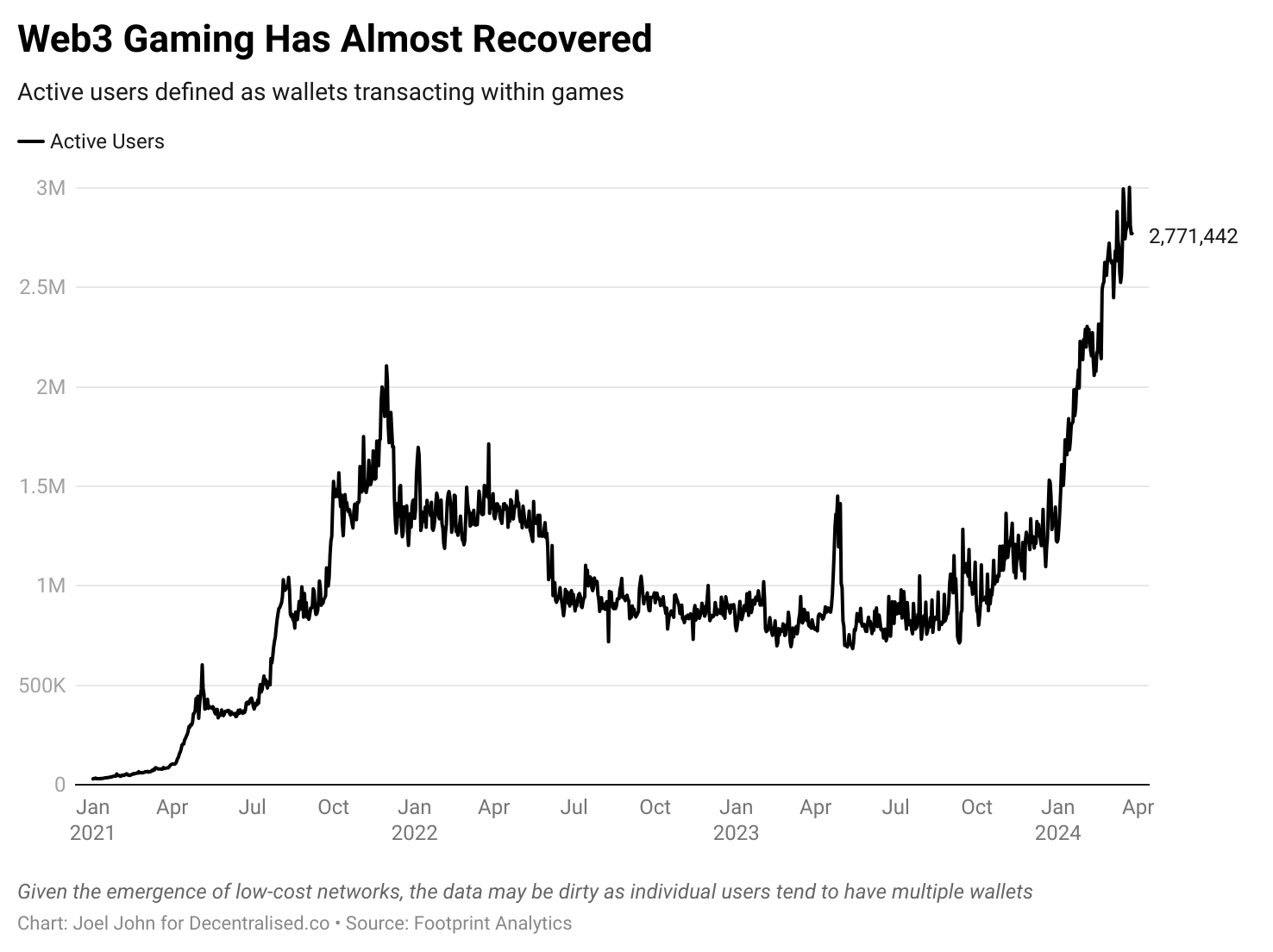

- The NFTs of the old guard that WILL survive and thrive (at least, in my opinion) are either those that are considered to be scarce crown jewel assets (see: CryptoPunks, Fidenzas, Autoglyphs, etc) or assets that provide productive value (in-game assets, pass through/cash flow assets, single purpose assets). For the former, that is late-stage cycle activity (I do believe we will see a late-stage re-rate of these NFTs as money rotates); for the latter, we need products that have natural product/market fit (I believe gaming will experience a significant boon starting Q3 2024 and lasting well into 2026 - as such, those assets should start to accrue value).

What is not being spoken about, is the growth of NFTs on other chains. Solana and Bitcoin NFTs are gaining market share, with 3 out of the top 10 NFTs by market cap that includes Bitcoin Ordinals (Ordinals = NFTs, in layman's terms). This is a game of “chicken or egg”. NFTs have proof of product/market fit as both incentive vehicles and coordination tools, and the technology and infrastructure underpinning NFTS have been validated by which value can be transferred across an immutable, public, decentralized ledger. What NFTs have NOT done, to reiterate, is follow-through. RWAs are promising but years away. Gaming is promising but requires a zero-to-one iteration (again, I believe that happens shortly). Collectibles need to find some tangible productive value to ascribe to assets, or they will continue to dilute themselves into oblivion.

We are seeing some of the follow-through happen - some of the better capitalized projects are trying to create games, metaverses, apparel, anime, horizontal business lines, etc. However, these projects have bad sentiment attached to them because the market created inflated valuation models for these assets and re-rated them, and then re-pegged their viability to their high water mark. Many of these assets still trade at above their issuance price, but that matters not to the participants who were late adopters of the 2021 cycle and bought at the temporarily inflated valuations.

In this sense, NFTs are on the ropes. In every other sense, NFTs are better now than they ever were before. Infrastructure is an order of magnitude better for UX/UI, safety, transference, cost, provenance, etc. New initiatives we are seeing whispered around are fundamentally better than the first iteration. In the world of venture capital, our job is not to look at the present but to look at both the past and future. We see what they have done in the past, and we see what they CAN potentially do in the future. At present, most people have lost that message.

Can you offer detailed NFT/Gaming KPIs showing signs of bullish tendencies?

Fleyshman: Sure, amongst others, here are a few data points we recently found interesting.

What happened to Web 2 adoption of Web 3?

Web2 companies have largely failed at implementing crypto models into their systems because many had bad representation, received bad advice, and had lackluster execution due to being an ancillary part of their business. Facebook rebranded to Meta and flopped on its release because it didn’t bother to ask anyone who actually participates professionally in this space what would and wouldn’t work. Hubris from incumbent traditional companies will always leave them on the outskirts, potentially very bullish for crypto-native companies that grow organically. We believe that the winners will be born natively, not ported over from traditional companies.

We’ll circle back with Sasha later in the year to discuss some of these bigger ideas and thoughts. As Arca continues to grow, we’ll periodically add a few new voices to our weekly musings to give digital asset investors and enthusiasts a more well-rounded perspective. If there are certain areas of the market that you want to learn more about, contact the Arca team, and we’ll try to prioritize your questions.