First, we have to understand the role of the Fed. The Fed was formed in 1913 as an answer to the periodic financial panics that occurred regularly. Today, the Fed has the twin mandates of maximizing employment and keeping prices stable. To achieve these goals, it has policy tools; the main ones being the setting of short-term interest rates at the discount window and the ability to conduct open market operations, which just means the buying or selling of government securities to increase or decrease the money supply. It is supposed to be apolitical and not reactive to the markets; only having its dual mandates in mind when formulating policy.

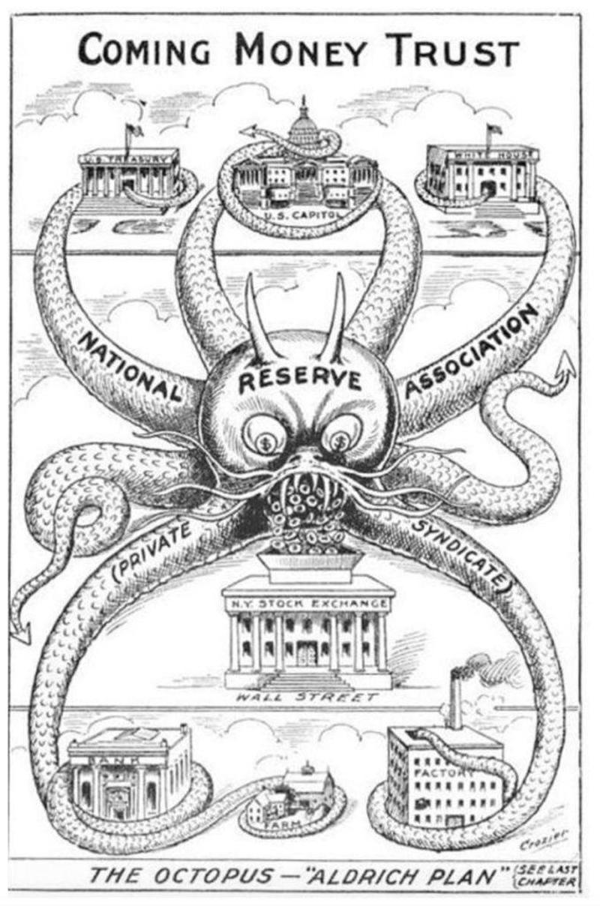

U.S. Money versus Corporation Currency (1912) Alfred Owen Crozier

U.S. Money versus Corporation Currency (1912) Alfred Owen Crozier

Interestingly, for an entity that has so much control over the direction of the economy, the general public has a very limited understanding and knowledge of the Fed. One wonders if this is a bug or a feature?

Since the financial crisis, the Fed has embarked on what has been termed “extraordinary monetary policy.” These were emergency policies deemed necessary to prevent the economy from collapsing into a 1930s-like depression. These actions included keeping short-term interest rates near 0% and a constant expansion of the Fed balance sheet through bond buying. In addition to that, the Fed began really using its most potent tool, communication of policy, to affect change in the behavior of market participants. All of this was supposed to end with the normalization of economic conditions.

Nearly a decade after the crisis, with an allegedly booming economy, monetary policy has still not returned to pre-crisis levels. The Fed started its tightening cycle under previous Fed chair Janet Yellen and was continued by Jay Powell when he assumed the role of chairman in February of 2018. His actions were seen as more aggressive as the tightening was on “autopilot,” which spooked the market at the end of 2018. Equities sold off violently and the white house ratcheted up political pressure on the chairman. At this point, Jay Powell indicated that he was considering changing course.

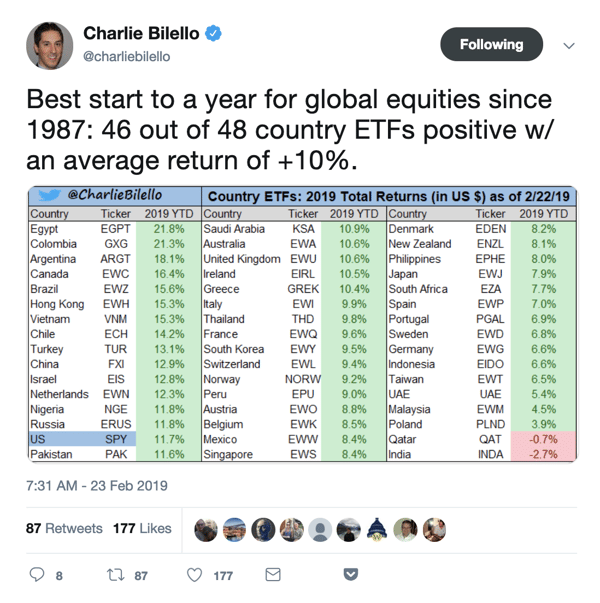

From that moment, the equity markets reversed, having their best run in 20 years, all on the statements of one man. The only thing that remained to be determined was the extent of the capitulation. Yesterday, we got our answer: Total and complete. Moving from 4 rate hikes in 2019, to zero and an almost immediate halt to Fed balance sheet reduction. But, according to Jay, everything is still peachy with the economy. How can both of these things be true?

Let's look at what this means for Bitcoin and crypto assets. Bitcoin was born out of the financial crisis of 2008. The problem that Bitcoin addressed was a lack of trust in banks in general and central banks more specifically. Satoshi Nakamoto, the mysterious and still unknown creator of Bitcoin, said:

The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve.

This problem of the creators and safeguarders of money acting contrary to your interests is what Bitcoin was designed solve for. From the moment it came into existence, the energy driving its adoption and value was the idea that these institutions of finance and banking could not be trusted. The capitulation and historically fast about-face by Powell only further strengthens that narrative. The fig-leaf of Fed independence and market agnosticism has been ripped off.

As such, what I find most interesting about this event wasn’t Powell’s boilerplate, bureaucratic propaganda about how the economy’s doing fine and how much central bankers love average Americans, but why he and the institution he heads felt a need to do this now.

There’s no doubt something has the Fed spooked otherwise Powell never would have done this. One factor is they know the economic ground’s starting to shift beneath them, and they need to push a particular narrative ahead of time so central bankers can once again do as they please when “the time to act” arrives.

It is important to realize how unusual and extraordinary an appearance like this is. It is a tell that some tectonic plates are shifting. The confirmation of this was the Fed action on Wednesday, being way more accommodative than almost anybody thought was possible.

Clearly, the Fed is considering things outside of employment and inflation and the goal is to affect asset prices for other reasons.

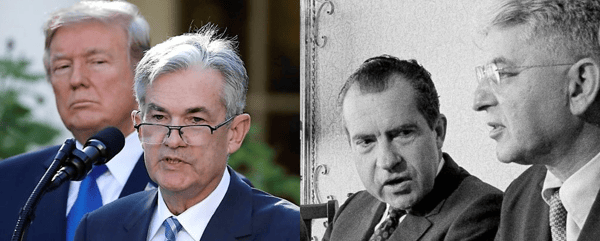

The public has always suspected that political pressure has been brought to bear on the Fed. I discuss that in this earlier piece, What’s Truth Worth? . The current occupant of the Oval Office has been incredibly vocal about wanting more accommodative policy. This pressure has been public and well-documented.

But this is not the first time we have seen this type of presidential pressure. Nixon also pressured his Fed Chairman, Arthur Burns, which only came to light with the breaking of the Watergate Scandal and the discovery of Nixon’s secret taping system. Ben Hunt does a good job making the connection:

In 1971, Richard Nixon had a problem. The US economy was pretty strong and the Fed wanted to tighten. But Nixon had an election to win in 18 months, and he needed loose monetary policy to do that. Also, the global economy wasn’t that strong, and the rest of the world needed an expanding supply of dollars and an expanding US trade deficit to keep its motor running. Nixon didn’t really care about that, but a lot of his oligarch cronies did.

So Nixon alternately bullied and cajoled and threatened and rewarded his hand-picked Federal Reserve Chair, Arthur Burns, to do the right thing and keep the money spigot open … wide open. Complaints about too much liquidity sloshing around were “bullshit”, and so what if they were running the economy hot? Good lord, man, imagine who would take over the White House in 1972 if he were defeated! Imagine the insane fiscal spending policies that those Democrats would push on the country if he lost!

Donald Trump has EXACTLY the same problem.

Donald Trump has found EXACTLY the same solution.

The point here is less about Trump exerting pressure, and more the fact that politicians of any political affiliation will bend economic policy to their bidding. Hunter S. Thompson identified some of the problems with the imperial presidency when looking at Nixon that still ring true today:

We’ve come to a point where every four years this national fever rises up — this hunger for the Saviour, the White Knight, the Man on Horseback — and whoever wins becomes so immensely powerful, like Nixon is now, that when you vote for President today you’re talking about giving a man dictatorial power for four years. I think it might be better to have the President sort of like the King of England — or the Queen — and have the real business of the presidency conducted by… a City Manager-type, a Prime Minister, somebody who’s directly answerable to Congress, rather than a person who moves all his friends into the White House and does whatever he wants for four years. The whole framework of the presidency is getting out of hand. It’s come to the point where you almost can’t run unless you can cause people to salivate and whip each other with big sticks. You almost have to be a rock star to get the kind of fever you need to survive in American politics.

The abruptness and severity of Powell’s actions today speak to the existence of greater systemic pressure and risk than people realize. Mike Krieger again:

The recent global slowdown and concurrent central banker panic is proof we’ve arrived at a very important inflection point....As such, every person in the world needs to understand what the Fed and other central banks did during the last crisis, and what they plan on doing the next time around (more of the same and worse). If you judge an economy based on stock market performance and aggregate GDP, you might think the Fed did a great job over the past decade, but if you judge it based how we’ve turned an entire generation of young people into debt slaves, arrived at levels of inequality unseen since just before the Great Depression and catalyzed an explosion of populist politics throughout the western world, you might be ready to grab a pitchfork.

This is the inflection point and the thesis of out of control governments, unaccountable central banks and a disproportionately wealthy elite is upon us. This was the environment crypto was designed to address. If an uncontrollable, unalterable, independent currency were to take hold, it is hard to imagine a set of circumstances more favorable for that to occur.

This is the time to make crypto a part of your portfolio and take it seriously.