If you have been paying attention to the political environment here in the US (and I won’t fault you if you have looked away for your own sanity), several budgeting and taxation plans have been outlined by the politicians lining up to challenge Donald Trump in 2020. Bernie Sanders floated Free Education, Alexandria Ocasio-Cortez proposed the Green New Deal, and Elizabeth Warren, Cory Booker and Kristin Gillibrand all have their own proposals. The common thread that connects these proposals is that they to rely on Modern Monetary Theory (MMT).

The fact that MMT is gaining traction and broader academic acceptance has implications for the economy, asset prices in general and cryptocurrencies. I will outline the tenets of MMT below, and what it means for the blockchain ecosystem.

Prior to MMT, the two main camps of economic theory could broadly be broken into the Austrians vs the Keynesians. For a fun take on it, check out this Rap Battle between each side’s historic champions, Hayek and Keynes.

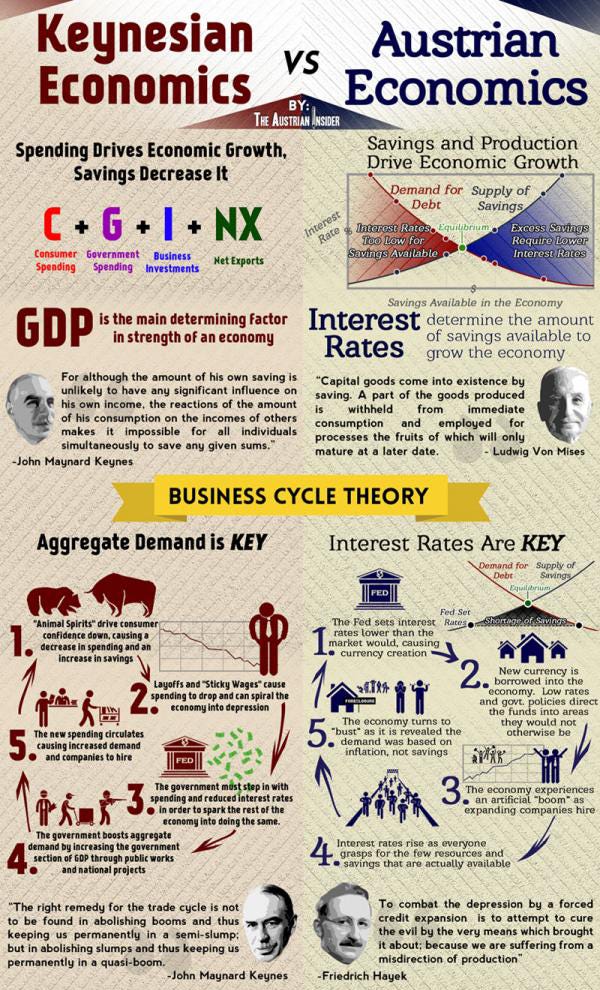

Broadly speaking, Austrians believe the business cycle is unavoidable and interest rates and savings are the most important factors, while Keynesians believe that aggregate demand drives the train and that governments can smooth business cycles by running deficits when appropriate. The infographic below does a good job summarizing the differences:

The debate between Austrians and Keynesians has been raging for decades, with the vast majority of modern central bankers falling into the Keynes camp. This has been the philosophy that has dictated the monetary policy regimes from the intervention during the Great Recession. That environment alone caused great concern about runaway deficits and the inevitable inflation that would accompany it. Even though the acolytes of Keynes advocate an interventionist central bank and running deficits during recessions, they still believe that debt and deficits matter. This brings us to MMT and how its proponents advocate going further than Keynes ever dreamed.

In the most general sense, MMTers believe that debt for sovereigns is different than any other entity’s debt. An independent state can print their own currency, any debt denominated in their own fiat does not really matter. They can always print more and extinguish any debts, no matter the size. The only thing controlling the amount able to be printed is inflation. This post from The MacroTourist does a good job outlining MMT.

One of the most prominent academic voices promoting MMT is Stephanie Kelton from Stony Brook University. If you have the time, I highly recommend you watch her video “But How Will We Pay for It?” In this video, Professor Kelton makes the case that cost should not be considered when governments’ consider what projects they should pursue.

One can debate the merits of each of these economic schools of thought, but it is hard to argue that a government that does not consider cost, like any other entity, will spend more than those that do take cost into consideration. Even before employing MMT, the world is awash in debt and fiat currency. Prominent Keynsians, like Paul Krugman, realize that even though he aligns with MMT on current policy, their disregard of deficits and debt is dangerous and will lead to inflation. In this NYT Op-Ed, Krugman argues about the limits of demand generated through debt, and comes to this conclusion:

But the MMT people are just wrong in believing that the only question you need to ask about the budget deficit is whether it supplies the right amount of aggregate demand; financeability matters too, even with fiat money.

This means inflation is coming; make no mistake about it. Governments are barely constrained even when saying deficits matter. Once the fig leaf of fiscal restraint is removed, the fiat spigots will really be opened up. This is the environment bitcoin was designed to address and makes what was being considered during the financial crisis look like child’s play. This is the time to be accumulating assets that can not be inflated or manipulated.

.png)