What happened this week in the Digital Assets markets

What happened this week in the Digital Assets markets

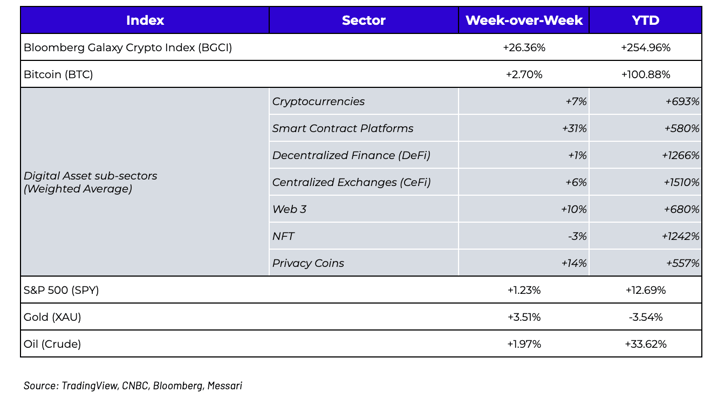

Week-over-Week Price Changes (as of Sunday, 5/09/21)

Inflation, the Economy and Rates that Can Never Actually Rise

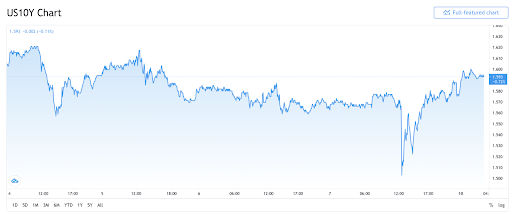

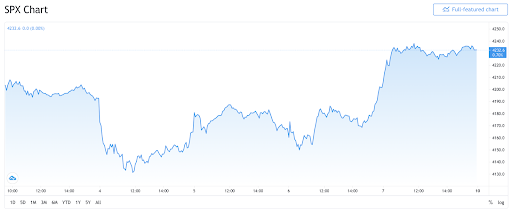

On Tuesday, U.S. Secretary of the Treasury, Janet Yellen, spooked global markets when she indicated that rates may have to rise to keep the economy from overheating. Stocks fell, the VIX rose, and digital assets fell… in fact the only thing that didn’t move on the big rates “news” was...rates (Treasury yields were unchanged). Only a few days later, a sobering April jobs report came out and it was a sizable disappointment amid a recent string of encouraging data, which had been indicating that the economy was recovering nicely. The employment data caused the 10-year Treasury yield to fall 10 basis points before recovering, but yields stayed just low enough to propel US equities to yet another new all-time-high.

This is really all you need to know about investing right now. The market is looking for any data that gives the Fed an excuse to avoid raising rates. The inflation signaling was viewed as a bluff, but the employment data was real.

Source: TradingView

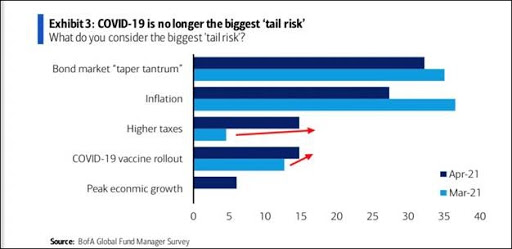

Now, inflation itself is not a bluff. In fact, it is top of mind. According to the Bank of America Global Fund Manager survey, COVID-19 is now only the third-biggest 'tail risk' behind "higher than expected inflation" and "a tantrum in the bond market". Almost 93% expect rising inflation in the next 12 months — the highest percentage of respondents to identify this as the biggest “tail risk” since May 2004. Further, the number of mentions of “inflation” during earnings calls has more than tripled year-over-year, the biggest jump since 2004. Even Warren Buffett and Sam Zell are now ringing the inflation alarm.

Of course, the Fed itself will tell you otherwise.

And this is important. How can rates rise when every country on the planet has accumulated massive quantities of debt over the past year? As Deutsche Bank wrote in a weekly note regarding defaults, “the only way overall levels of debt are sustainable is if government real yields stay consistently negative for multiple years or even decades. Perhaps the most pragmatic way out is inflation plus financial repression, meaning real yields go even deeper into negative yield territory in the years ahead.”

And herein lies the conundrum. Central bankers have backed themselves into a corner, as they cannot actually raise rates in any meaningful way or this would immediately bankrupt governments around the world due to an inability to service debts. And they can’t (or won’t) acknowledge that they’ve created a monster they have no control over.

So we have real inflationary pressures, but data that says it isn’t here, which keeps the dollar and rates near all-time-lows… and you wonder why both interest and trading in Bitcoin and other digital assets is surging?

Digital Assets Trading Volumes are Surging as the Market Grows Up

And yes, we mean surging. Take any metric you’d like to show how fast this market is growing.

Website traffic? Yep, exchange web traffic at digital asset exchanges hit a 3-year high with 530 million visits in April, only slightly below the January 2018 all-time-high of 532 million. Twitter followers of these exchanges also hit new all-time-highs, surpassing the 2017 peak, with a much more gradual rise this time versus the massive spike we saw four years ago.

The driving force remains the wall of money from traditional finance pouring into digital assets, which is now the fastest of any asset class in the history of the world - a $2.2 trillion rally in just 14 months from barely $100 billion of total market cap last year to over $2.3 trillion today.

Source: QCP / TradingView

Meanwhile, digital assets haven’t so much as hiccuped even as we’ve seen a collapse of all other forms of speculation, which could be due to a massive rotation into this asset class, or simply a prelude of what is to come next for digital assets. Joe Weisenthal of Bloomberg recently wrote:

“...it really feels like crypto is draining all the speculative juice out of the market right now. It's like the gambling crowd is moving on from stocks. It's hard to prove, but you can see call option volume has significantly pulled back and is now sitting near its lowest levels of the year. At the same time, the red-hot names from last year and early this year have gone super quiet. You hardly see anyone talking about ARKK these days. There's a bunch of other stuff like Chamath's SPACs, and Microstrategy that all kind of look similar right now.”

Naturally, we wonder if the digital assets strength will also fade like it has with other markets. It’s certainly possible. But on the other side of speculation and trading is a technology that is permeating every facet of global finance. Our friend Noelle Acheson of Coindesk may have said it best:

The reason this is so difficult to grasp is that it is a truly worldwide phenomenon. In traditional markets, it’s typically easy to pinpoint one or two areas where strength or weakness can be attributed, or a few trends in valuations that investors are focused on. If stocks are slumping, perhaps US equity funds have outflows, and if tech stocks are rallying, perhaps it is due to multiple expansion. But how do you measure a market where each new entrant offers an entirely different collection of assets to trade to an entirely different audience, with an entirely different set of valuation techniques? In addition to market fragmentation, you also have opinion fragmentation. Jesse Proudman of Strix Leviathan recently nailed it when talking about the divergence of opinions on what digital assets are worth:

“Digital assets are a speculative asset class with opaque fundamental value. Opaque fundamental value does not mean no fundamental value. It means most market participants don't share the same valuation model for each asset. The value I place on Bitcoin, and the value you place on Bitcoin are likely very, very different. This is one of the primary reasons why this asset class is so volatile, and why there's so much opportunity for speculation.”

Therefore, pockets of speculation may die down, while other pockets accelerate. As such, the growth in the asset class will likely continue unabated.

What’s Driving Token Prices?

Retail buyers were out in full force last week. The 2017 legacy coins came into vogue again, mainly due to exchange accessibility. This move was a good indicator of retail sentiment as we’ve seen the rotation cycle of BTC-> ETH -> DeFi-> to legacy tokens… ETC +162%, BCH +55%, LTC +43%, BSV +15, XLM +14%, XRP +5%, EOS +64%, ADA +32%, TRX +15% and NEO +8%. These are mostly older proof of work coins which are easily accessible to retail investors in the US via onramps like Paypal, Square, Robinhood and eToro. These movers are indicative of the smaller playbook that retail buyers work with, who are more likely to invest within the scope of the tokens that their exchanges provide when bullish sentiment is running strong.

- SUSHI (+9%) - Saw a move higher as the team released a proposal to update the tokenomics via governance, partnering with Gauntlet for assistance, which provided an incentive for LPs who are in the midst of a multi-month unlock that adds 50% of supply to the market.

- FTT (+11.5%) - Continues to prove itself as an innovator in the digital asset space not only as one of the largest volume exchanges, but one with best in class product variety. FTX launched lumber commodity contracts and saw some relatively solid daily volumes (up to $8M).

- DOGE (+39%) - A much anticipated appearance by Elon Musk on Saturday NIght Live with the expectation that he was going to tout Dogecoin erased an ATH mark of $0.74 and closed the week at $0.53.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency