What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?

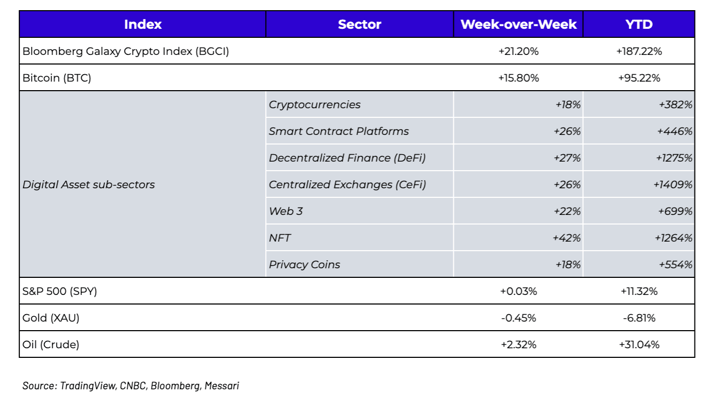

Week-over-Week Price Changes (as of Sunday, 5/02/21)

The Rise of Ethereum (ETH)

The digital assets market caught fire last week, which should come as no surprise to those who tried unsuccessfully to buy the dip a week ago. When there are no sellers, it’s only a matter of time before prices move higher in an effort to find a new equilibrium between sellers and buyers -- and this equilibrium just happened to be 20% or so higher.

There were of course some macro reasons behind the move higher in risky assets -- the Fed kept its benchmark interest rate unchanged at a near-zero level on Wednesday, companies are crushing earnings expectations, and US GDP bounced back to near pre-pandemic levels (Q1 +6.4% annualized), recording its third consecutive quarter of robust growth. But the move higher in digital assets really had nothing to do with macro, or earnings, or even Bitcoin.

There is a real, fundamental, and persistent demand shift happening right now. New investor money has been flowing into digital assets since the 3rd quarter of last year, but the investor goals are changing. A few years ago, allocations to digital assets centered around “can you get me exposure to Bitcoin?”. Roughly nine months ago, it shifted to “Bitcoin has been great; what else can you get me exposure to?” And in the last few months, the investor interest has narrowed even further to “can I specifically diversify away from Bitcoin into Ethereum and other digital assets?” Frequent readers of “That’s Our Two Satoshis” know that we have often talked about the different sectors, different token structures, and the different value drivers amongst digital assets, and therefore the idea of “Bitcoin versus everything” never really made sense to us since the investment thesis for Bitcoin is about purchasing power and inflation whereas investing in other digital assets is about cash flows, yields and customer usage. But Bitcoin always two main advantages for being the main onramp into digital assets:

- Everyone has heard of it, and there are enormous resources and money dedicated solely to onboarding investors into Bitcoin

- The investment thesis is incredibly simple (either you believe in digital gold, or you don’t)

Well, Bitcoin’s stronghold as an onramp for new investors has shown signs of weakness as the market continues to evolve. The price of BTC fell -2% in April, while the price of ETH rose +39%. According to OTC dealers, exchange data and even anecdotal evidence from our own Arca fund flows, it’s clear that this demand for ETH and ERC-20 tokens supporting the applications built on top of Ethereum has been coming from new money into the system, and from a rotation out of BTC into ETH.

Now, the irony is that neither BTC nor ETH are the easiest digital assets to explain to new investors. If I had a “Zoom aha moment” button to pinpoint and timestamp the exact moment when a new investor comes to their first realization that digital assets are the future of investing, stakeholder coordination and customer bootstrapping, it is almost never when describing the two largest digital assets. Bitcoin typically receives a heavily emotional and media-influenced response, Ethereum receives an incredibly confused response, while digital assets that underpin real cash-flow producing businesses (DeFi, CeFi, gaming tokens, sports/entertainment tokens, etc) typically trigger the “aha moment” face. But Ethereum has now crossed the rubicon into the mainstream, and despite the difficulty understanding it, investors of all sorts are finding reasons to add ETH to their portfolios.

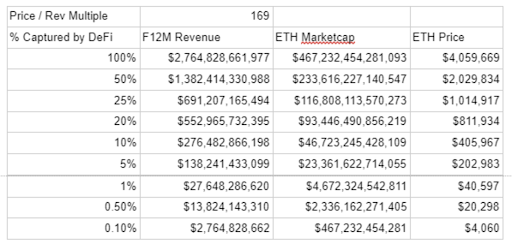

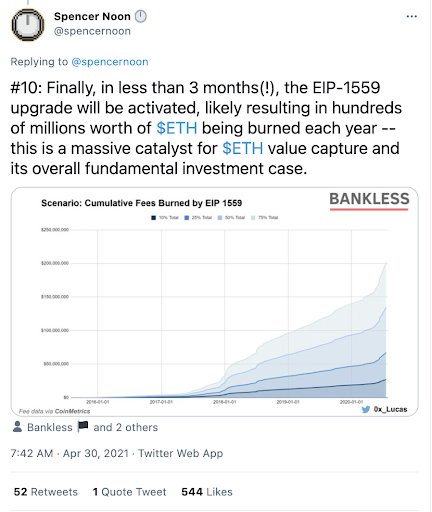

And there is a strong reason for this narrative shift. Spencer Noon gives an incredibly bullish and succinct summary of how Ethereum is flat out dominating the blockchain world. But for investors, it’s the 10th and final tweet that matters most -- for the first time, the ETH token will now capture real economic value off of all of Ethereum’s success.

“Ethereum is a decentralised computer, and compute power costs money. The more useful DeFi applications built on Ethereum become, the more fees will be paid by users escaping the rapacious [Centralized] CeFi platforms. A portion of all fees spent using the trust rent-seeking gatekeepers of the traditional financial economy could in the future accrue to these [decentralized] networks. Let’s assume that Ethereum can capture some percentage of the 5-year average earnings of banks and the big four audit firms. Below is a table depicting a hypothetical scenario where for the next 12 months a certain percentage of revenue is diverted from a centralised to a decentralised service. At 0.50%, the price of ETH, assuming that amount of activity is diverted to its ecosystem, implies a 10x price appreciation from current levels; at 0.10%, the exercise implies a doubling of the ETH price. I am very certain that DeFi can take away at least 0.50% of activity from CeFi.”

Now, Ethereum should not be viewed in a singular vacuum any more than Bitcoin should. There are now thousands of digital assets that offer different risk/reward opportunities, many of which can help investors express different investment themes. But for those still just dipping their toes in, it’s refreshing to see that Mr. Market has at least opened up a second pool.

Aligning Incentives - Coinbase, Skew and JP Morgan

We cite data and charts from Skew all of the time. It is one of the greatest databases and visual representations of digital asset market dynamics available in the market. We were thrilled for the great team at Skew when they announced that Coinbase had acquired their company. Well deserved!

That said, a part of me feels a little burned too.

As a huge Skew fan, a happy and early paying customer, and probably one of their biggest evangelists given we’ve written about Skew and sourced their data hundreds of times in our newsletters, it just stings a little that Skew is moving on and we’ve got nothing to show for it. In the spirit of digital assets and democratization where all stakeholders are supposed to benefit, not just shareholders, I can’t help but to feel a little slighted that a top customer and evangelist like ourselves will receive nothing from this valuable transaction.

Maybe that’s greedy of me. Or maybe this is just another prime example of why tokenization will eventually take over as the primary means of financing projects. We’ve discussed this dynamic previously, where AirBNB and DoorDash created billions of dollars of wealth for their shareholders, while creating nothing of value for the regular people in the ecosystem who drove their success. Meanwhile, Uniswap, the fastest growing decentralized exchange, gave away 400 UNI tokens last year to every single customer who ever used their platform, and with the UNI token now trading north of $40, that is a $16,000 gift to their most important stakeholders. They didn't sell this to customers; they gave it away -- in a related story, Uniswap customers are very sticky even when other platforms pop up that offer similar and even cheaper services. When companies issue tokens to employees and customers and anyone else in the ecosystem that is critical, any acquiring company that doesn’t want to lose all of the acquiree’s employees and customers would need to compensate token holders in some way upon acquisition or risk losing the most important thing they ar

e acquiring. But without this dynamic, Coinbase can buy Skew, a few shareholders make a ton of money, and customers feel… well… like completely unimportant contributors to their success.

Meanwhile, Coinbase wonders why their stock is trading like a bag of hammers since its public debut. They have over 50 million passionate customers who were directly responsible for Coinbase’s success, yet Coinbase now has to find mercenaries on the Nasdaq to buy their stock who don’t care one bit about Coinbase other than its revenue potential, while their customers completely ignore the equity in the company they helped build. This is an alignment problem, one which Brian Armstrong knows and chose to ignore. While they did gift shares to employees at the last minute, they conveniently and intentionally left out customers and other stakeholders.

Jamie Dimon at JP Morgan is one of the biggest beneficiaries of a completely crooked and misaligned financial system, yet he pretends to care about stakeholders even though he caters exclusively to shareholders, while real stakeholders (the cities JP Morgan does business in and the employees and customers) hate everything about JP Morgan.

Digital assets were supposed to be different. Hopefully, a few more companies read this before Coinbase buys them.

What’s Driving Token Prices?

After a bullish week across all digital assets sectors, Sunday evening saw Etherium break out to new highs of $3060 (+27%). Several upcoming catalysts, like EIP-1559, are fueling this rally which blasted through $3000 as if it was an afterthought. EIP-1559 is essentially a proposal to change ETH’s fee structure where transaction fees are burnt instead of paid out to miners - this mechanism will decrease the inflationary nature of the asset, as well as remove overhang due to miner-related selling. Layer 2 protocols like Polygon (MATIC) are also gaining traction, as they offer solutions that run on top of Ethereum to facilitate near-instant transactions through the use of "fraud proofs". DeFi names followed suit with ETH acting as trailblazer:

- AAVE’s (+33%) governance passed a liquidity mining proposal which went into effect on Monday. The program distributes 2,200 staked AAVE (stkAAVE) per day to lenders and borrowers and will go from 4/26 to 7/15. Since their announcement that the proposal passed, the total value locked (TVL) of the protocol jumped $5.04B, a 91% growth.

- The market took strong attention to UNI (+26%) as it finished the week with all time highs of $228B in volumes, 72K liquidity providers and $44M all time traded.

- SUSHI (+24%) is working on updating their tokenomics, which will likely look something similar to CRV's tokenomics where tokens are locked up to increase voting power in governance. This aims to help stifle the overhang related to the token dilution from the ongoing unlock.

- RLY (+20%) announced the launch of their "eco friendly" NFT platform, however they are planning to integrate NFTs closer into a creator's economy (whereas now a lot of these NFTs are fairly separate) with plans to roll out a beta version next month.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency