What happened this week in the Crypto markets?

Bitcoin Still Acting as a Leading Indicator

With the exception of oil, risk assets continue to advance unabated. It’s as if we’ve already had both a recession and a recovery in the past 6 weeks, before either event has actually occurred. Once again, Bitcoin acted as a leading indicator for US stocks, rising modestly the week before and setting the stage for an equally modest rally in equities. We mentioned last week that global risk managers have no excuse not to monitor Bitcoin -- but at this point, they are now blatantly ignoring important signals if they are not paying serious attention to the US markets.

| Week Ending |

3/15/20 |

3/22/20 |

3/29/20 |

4/05/20 |

4/12/20 |

4/19/20 |

| S&P 500 |

-9% |

-15% |

+10% |

-2% |

+12% |

+3% |

| Bitcoin |

-34% |

+11% |

Unched |

+13% |

+2% |

+3% |

| Gold |

-8% |

-2% |

+9% |

Unched |

+4% |

Unched |

| Oil |

-33% |

-28% |

Unched |

+25% |

-9% |

-11% |

Source: CNBC, TradingView, CoinMarketcap

For a minute, let’s forget about the enormous return potential of Bitcoin and the recovery of other digital asset prices. Instead, let’s focus on its importance in the global financial ecosystem. The frequently discussed narratives may or may not come true. Is Bitcoin a safe haven? Is it protection against hyperinflation? Is it the currency of the future? Is it the backbone of all financial transactions? Sure, maybe… but what Bitcoin is today is relevant. In the past few years, we’ve seen Fidelity, NYSE, Susquehanna, Two Sigma, Jump Trading, DRW, the CME, Square, Robinhood and many others become powerhouses in Bitcoin trading. We’ve also seen CNBC, Bloomberg, Forbes, the Wall Street Journal and many other media outlets dedicate significant coverage to Bitcoin. We’ve seen the President of the United States, the Federal Reserve, the SEC, the Treasury Secretary and the G-7 discuss Bitcoin.

But that’s, of course, old news. So let’s take a look at what has happened just in the past week.

That last one is the most surprising and exciting. While Renaissance is unlikely to be an outright buyer or seller, preferring instead to focus on trading volatility via their quantitative models, Renaissance offers yet another sizable vote of confidence in Bitcoin’s staying power as an asset class. This industry needs legitimacy more than new buyers. There is plenty of demand already for Bitcoin. But many wealth managers and institutional investors like to follow the leader, and each new legitimate person, fund, or investor that endorses Bitcoin as a tradable or investable asset paves the way for others. The roads are now paved, and open. While few want to be first or last… being first is no longer an issue.

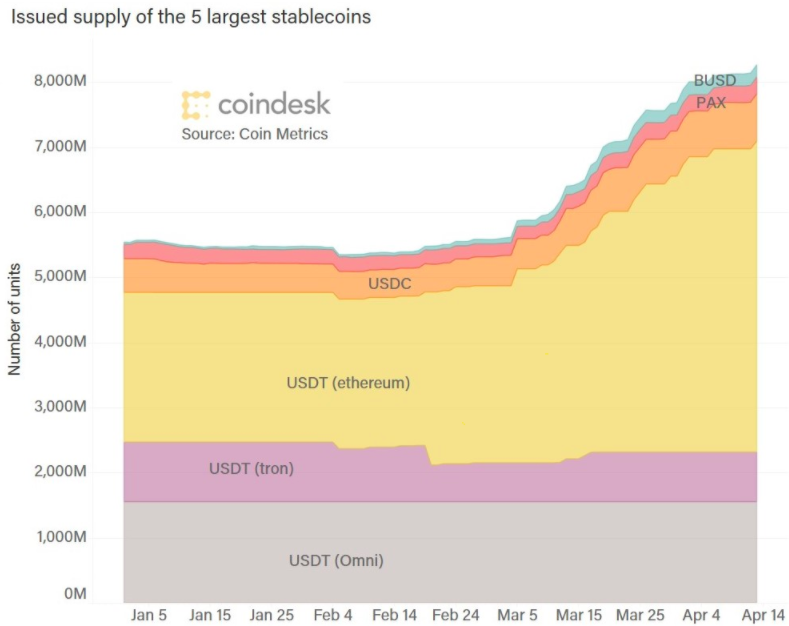

The Rise of “Stablecoins” the Most Stable Cryptocurrency

Bitcoin is the most well-known asset in crypto. Non-currency digital assets (those backed by real assets or issued by cash-flow producing companies) are the most interesting investments in crypto. But “stablecoins” are by far the biggest success story in crypto.

“Stablecoin” is the most commonly used term for a digital asset that is pegged to fiat currencies, most frequently the US Dollar. These tokens can be used as trading pairs on exchanges, or as a medium of exchange outside of the banking and brokerage system. The growth has been tremendous, surpassing $8 billion in combined market capitalization, almost double what it was prior to the Covid-crash. As we learn in early mathematics classes, “the numbers don’t lie”.

For those who have been following the rise of stablecoins over the past few years, this is precisely the behavior one would expect to see: volatile markets usher in a flight to safety (selling other high beta digital assets into stablecoins) and a flight to “dollars” (participants in other countries buying stablecoins as a dollar surrogate, which has become even more important due to the current dollar shortage). Add in the imminent era of zero (or even negative) interest rates and the potential for inflation / recession and we may have a perfect storm translating into continued growth and adoption of stablecoins.

Aside from the incumbents listed above, new entrants are coming. Facebook’s Libra project is back from the dead after the defection of several prominent members, a very public skirmish with the federal government, and scrutiny from the leading oversight bodies. Libra 2.0 has very little of its original DNA, as it is less open and less decentralized and is an attempt to address the regulators’ concerns and to compete with the alternative solutions that continue to emerge. Central Bank Digital Currencies (CBDC) are on their way too, led by China’s upcoming launch of their DCEP token. This has become such a hot topic that the G20 Financial Stability Board (FSB) last week reported their concerns and proposed regulations to the G20. (See “What We’re Reading” section for story links and a more comprehensive breakdown of the various announcements last week).

The guidance coming out of the G20 Financial Stability Board focuses on ”systemic threats to the global financial system” should stablecoins be ”widely adopted”. One of the key tenets of the guidance from the FSB is that it's ”inevitable that stablecoins will integrate into mainstream potentially integrating with the current service providers”. It seems the FSB is trying to get ahead of this by requesting their member countries act now with legislation and supervision, and will be issuing guidance in October of 2020.

In the meantime, stablecoins give crypto purveyors something important to focus on besides price.

VCs Need to Learn How to Become Distressed Buyers… Quickly

Venture capital funds were the first to endorse and invest in digital assets, for a variety of reasons. In the early days, investing in digital assets seemed to fit the VC profile -- scatter your bets, look 10 years into the future, and hope you hit a few home runs to outweigh the numerous strikeouts. As the digital assets space has matured, having liquid capital markets experience has become far more important, but the VC world still has heavy ties to this space.

Right now, however, VCs have bigger problems than crypto. Not only are they being forced to write down the value of the assets in their portfolios, some may soon learn a painful lesson in the transfer of equity ownership to debt holders via bankruptcy.

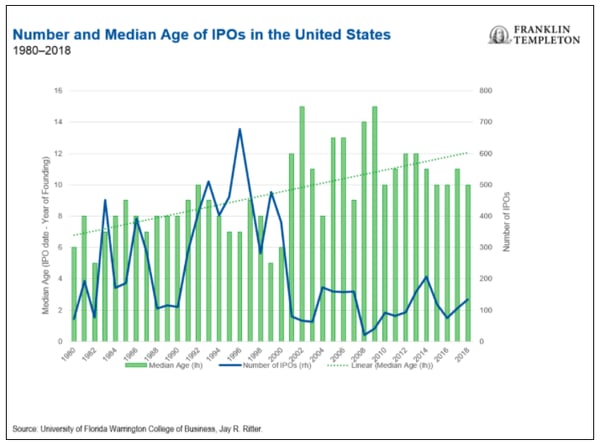

Over the past 15 years, private companies have shown little interest in going public, opting to stay private for far longer as they had unlimited access to enormous late stage rounds of capital from the largest venture investors, and could actually benefit by not IPO’ing too early. Furthermore, many opted to layer on debt before going public. This strategy seemed wise while equity markets were going up indefinitely but is untested during an economic downturn. Not only do some of these companies now have to worry about when (or if) the equity markets will open back up, but some are now raising more debt to offset the lack of revenue and working capital caused by global lockdown.

Source: Franklin Templeton

Airbnb for example just tapped the bond markets not once, but twice, in the past few weeks, with both an unsecured bond deal and a secured loan. The amount of debt placed on the balance sheet is very little compared to the large (but declining) equity valuation, but companies with no revenue, no profits and high working capital needs can go from having a strong balance sheet to a weak balance sheet in short order. And a quick look at the investors in the bond and loan deals should make equity investors pretty nervous…distressed investing titans Apollo, Silver Lake and Oaktree certainly have no qualms about taking the equity in a restructuring. Companies like Robinhood, WeWork, and others are probably not too far behind AirBNB. Meanwhile Motif Investing already shut down despite raising $125 million in venture funding over the past 10 years.

The Private Equity world knows this playbook very well. For example, Envision Healthcare was taken private by KKR in 2018, investing $3 billion of equity and layering on $7 billion in debt during the LBO. Now that profitable elective surgeries have dried up due to Covid-19, this debt is now down 50-80 pts, and the equity is likely worthless, causing Envision to explore a restructuring. But KKR will likely emerge with a significant chunk of the reorg equity post restructuring, because they will buy the secured debt at deep discounts. The gains on the new unlevered reorg equity may one day surpass the initial loss on their existing equity contribution.

The venture capital community needs to start thinking like private equity investors, even if their portfolio companies may be 6-18 months away from giant bankruptcies. Huge private equity valuations can be erased in a heartbeat as debt covenants are breached, interest payments are missed, and once strong companies are forced into receivership.

Given the strong ties between venture capital investors and crypto, could we see non-dilutive capital raises in the form of digital assets acting as a bridge to profitability over the next few years instead of layering on debt and forcing restructurings? It’s certainly a possibility. One of the biggest frustrations from the crypto investing community is that there have been very few new digital assets to buy, as ICOs are dead and bankers have not been very creative with token offerings. These VC-backed companies should get more creative, and if they do, crypto investors will likely be waiting with cash to deploy.

If not, VCs better learn how to lead secured loan deals.

What We’re Reading this Week

A report from the Financial Stability Board (FSB), which coordinates rules for the G20 economies, last week recommended that stablecoins be regulated with a unified global approach. Although the report is likely in reaction to Facebook’s Libra, the report names stablecoins USDT, USDC, TUSD, PAX and DAI. The report also highlights the global macroeconomic impact of allowing stablecoins to continue operating in a grey area of the market and the need to regulate them in a uniform way. We will likely see these recommendations slowly implemented over the coming years as the G20 countries coordinate a regulatory framework for these assets.

Facebook’s Libra project broke a months’ long silence last week announcing it was still working on its blockchain-based payments system and had made some adjustments to the overall product vision. Detailed in a newly released white paper, Libra will now issue a number of currency-pegged assets, such as USD or GBP, in addition to its Libra (LBR) token. Spokespeople for Libra have also reiterated their intention to abide by all existing regulations and are seeking a payments license from the Swiss regulator and plan to register with FinCEN and intend to launch at the end of 2020. Despite this, there are still some within Congress that oppose Libra and do not see its recent changes as sufficient.

Full Steam Ahead for China’s Blockchain Ambitions

According to Grayscale’s quarterly report, the firm recorded inflows of $503.7mm into its investment products making it the strongest quarter ever, despite the broad crypto market sell-off in March. The Bitcoin Trust, which also became an SEC reporting company in January, received the bulk (77%) of the new assets. The majority (46.5%) of inflows are reportedly from multi-strat investors and about 90% of inflows come from hedge funds. The continued growth of the Grayscale products indicates continued investor appetite for digital assets which will likely continue in the current macro environment.

Blockchain startup Bloom announced it had partnered with Transunion to bring consumer credit data to blockchain. Bloom, which focuses on allowing consumers control over their data, previously launched a mobile app that included an identity monitoring feature, notifying users when their data has been leaked. The newest version will now include credit monitoring through Transunion. Bloom uses a blockchain-based ID system for users to take control of their identity and information, although they decided to remove blockchain from their marketing early on to avoid user confusion. Despite this, Bloom is applying blockchain to yet another issue faced in the increasingly digitized world.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)