What happened this week in the Crypto markets?

What happened this week in the Crypto markets?

The Most Hated Crypto Rally Presses On

As investors, there is a lot going on in the digital assets space besides just Bitcoin, but as broad market sentiment is concerned, Bitcoin continues to be the most important in this crypto rally. It is the largest digital asset by 7-fold, the most universally well known, and the most relevant from a global macro standpoint. This is not too dissimilar from equities, where MSFT, the FAANG stocks, and TSLA dominate global stock indexes, sentiment, and financial news coverage, while many equity investors quietly find significant alpha in undercovered stocks like SHOP, SNAP and AMD.

Bitcoin rallied a very respectable 7% last week, bringing MTD gains to almost 20%, and YTD gains to +7%. In fact, Bitcoin has now gained 6 weeks in a row since rising over 100% after falling a shocking and terrifying 34% in a single week ending March 15th. This recovery has been impressive no matter how you slice it --- compared to Gold (+2% WTD, +8% MTD, +14% YTD) and US equities (-1% WTD, +8% MTD, -12% YTD), and certainly compared to oil (-∞ WTD, -23% MTD, -70% YTD) … more on oil later.

But the largest digital currency took a backseat last week to non-currency digital assets. Many small cap tokens rallied as much as 20-40% last week, as the market witnessed the first signs of greenshoots since January’s explosive start. Platforms and protocols outpaced Bitcoin, led by Tezos (XTZ +20%), Stellar (XLM +24%), Algorand (+17%) and Cardano (ADA +29%). Certain DeFi tokens once again showed strength after a rough few months, led by Kyber (KNC +49%) and 0x (ZRX +20%). Infrastructure and scaling solutions like Matic (MATIC +19%) and Cosmos (ATOM +16%) rebounded after terrible starts to 2020, and application tokens were a mixed bag, with a few success stories like Enjin in the gaming sector (ENJ +42%).

While the jury is still out on the long-term value accretion of many of these “alt-coins”, there is one big difference between last week’s rally and the ones we’ve seen previously. Crypto is known for having frantic fits and starts, often producing wild and unsustainable gains. But historically, these outsized gains are often caused by levered longs in the futures market, and incredibly bullish retail sentiment, which pushes the prices in illiquid markets to unsustainable levels as traders think about nothing but upside. April’s gains are notable, however, because it might be the most hated rally crypto has ever experienced.

3 Metrics Causing Crypto Investors To Hold Off

We’ve been measuring three metrics since mid-March, all of which indicate that many crypto investors are sitting on the sidelines right now:

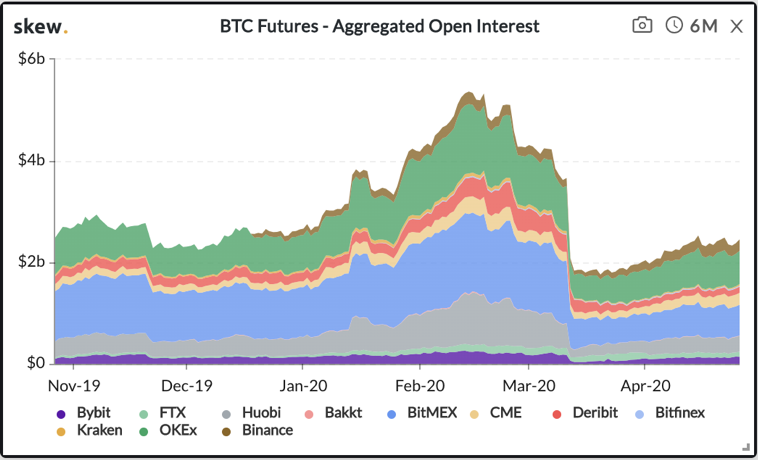

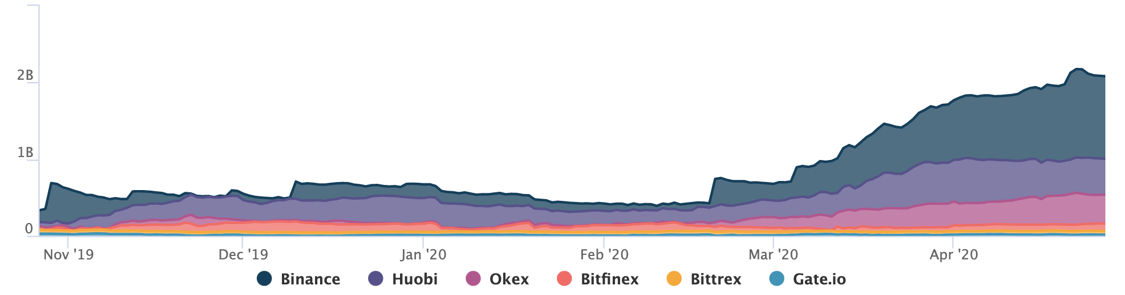

- Leverage -- which has been sucked out of the system after the early March margin call fiasco. Typically leverage rises when investors expect gains, but with leverage still near all-time lows, we haven’t even seen peak buying yet (low leverage also means less liquidation sell-offs, which is why Bitcoin has risen so steadily).

Source: Skew

Source: Skew

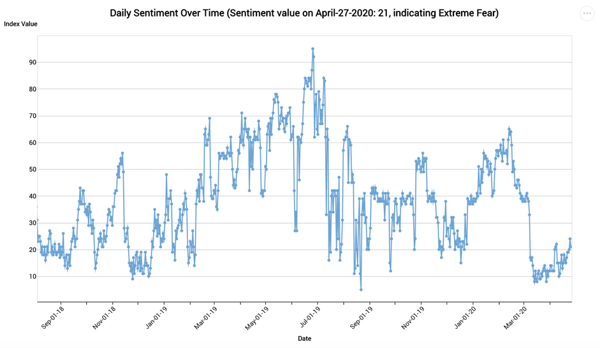

- Sentiment -- crypto market behavior is very emotional, as investors tend to get greedy when the market is rising. But according to the Fear & Greed Index, investor sentiment is still near all-time lows, and has registered “extreme fear” since March 12th despite a 100% rise from the bottom.

Sentiment as Measured by Fear & Greed Index

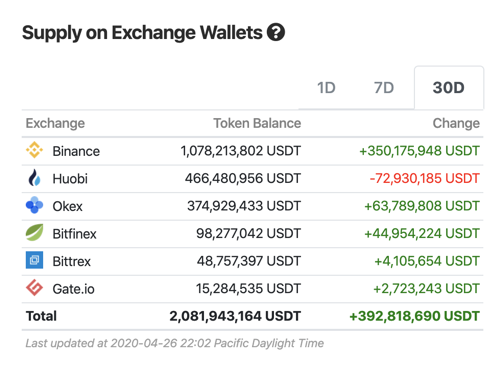

- Cash -- Cash is very easy to measure in crypto, via growth in “stablecoins”. Most of it sits on exchanges with nowhere else to go other than back into other tokens and coins. Stablecoin buildup has never been higher, indicating that an enormous amount of dry powder still has not been spent.

Cash, as Measured by Tether (USDT) Sitting on Exchanges

The global equity market rally from 2009-2019 was often characterized as being “the most hated bull market ever”. Investors were so emotionally scarred by the events of 2008 that many sat out the largest wealth appreciation opportunity of their lifetime, waiting for lower prices that never materialized (many are still waiting).

Similarly, the psychological effects of March’s swoon may now be causing crypto investors to miss out on what could be the start of the largest rally they’ve ever seen, one for which they’ve been waiting years to experience. This rally has been fueled by new money, and a lack of sellers, not euphoria and leverage. The perfect macro storm is now upon us, one about which many crypto investors have dreamt about since entering this asset class. Yet many are still waiting for lower prices that may never materialize.

Bitcoin is a Leading Currency, Outpacing the EUR, GBP and CAD

Back to Bitcoin, while it has underperformed many other digital assets YTD, perhaps it’s time for BTC to graduate from “best of the digital assets” to a more appropriate title of “rising star within global currencies”. Bitcoin, in US dollar terms, is now +7% YTD, outperforming all other fiat currencies including the EUR, GBP, CAD. As pointed out by Coindesk last week:

“The [slightly positive] year-to-date performance really just means it's keeping pace with the U.S. currency, which has become one of the world's most in-demand assets as the coronavirus prompts a flight by investors everywhere into cash. But if Bitcoin were a government-issued currency, it would be one of the world's top performers – beating not only popular emerging-market tenders like the Mexican peso and South Africa's rand, but also advanced-nation stalwarts like the euro, British pound and Canadian dollar.”

While Bitcoin may be a good investment in USD terms -- it may be an even better investment for international investors.

Oil Markets and the Hypocrisy of Bitcoin Detractors

It would be quite difficult to write a weekly market recap and not discuss the oil markets. But by this point, you’ve read and digested everything there is to know about what happened with USO, front-month futures contracts, and negative prices (Arca’s own David Nage recorded an epic podcast with Billy Bailey for Saltstone Capital this week).

From a crypto perspective, however, the oil market implosion just reminds us that there are many skeletons in the traditional market closet, and a lot fewer in digital assets than many believe. Just about every myth about Bitcoin and digital assets needs to be continuously challenged and broken down. The biggest competitor to digital asset investment adoption is the status quo, and we (along with other leaders in this industry) spend an enormous amount of time and energy educating new investors about the truth.

So let’s once again revisit some of the common myths.

- Digital Assets are Too Volatile

Rebuttal -- Oil. Not only has oil now fallen 30% or more in a single day TWICE in the past two months, but it is literally manipulated by the only legal government cartel (OPEC), dupes retail investors with misleading exposure via ETFs like USO, affects trillions of dollars of wealth, and oil companies make up almost 20% of the US High Yield Bond market. Nearly every investor has exposure to oil directly, or indirectly.

- Digital Asset Prices are Manipulated

Rebuttal -- so are most ETFs. Bitcoin ETF proposals continue to get shot down by the SEC, citing market manipulation as one of the many reasons for its dismissal. We already touched on oil ETF manipulation, but now many other ETFs are being manipulated by the Fed's new stimulus packages (directly buying bond ETFs). In fact, State Street is now openly telling clients, "These are the Top 7 ETFs to buy now - because we think the Fed will buy them soon!!" BlackRock, which is quarterbacking Fed purchases, is now able to buy its own ETFs on behalf of the Fed, raising red flags all across the investment world for its lack of transparency and conflict of interest.

- Digital Assets Have No Intrinsic Value

Rebuttal -- neither do stocks or bonds. We've discussed this one at length, but it's worth repeating over and over and over again. Investing is speculation, and March/April 2020 has reminded every investor about how little intrinsic value matters.

If COVID-19 has taught us anything, it’s time to rethink what you believe, and remove some cognitive biases.

Notable Movers and Shakers

While Bitcoin carried significant gains into the new week (+7%), it did not find itself separated from the rest of the market (BTC.D unchanged). There were some significant outperformers, as market darlings were well bid in a “comfortable” market setting. However, some projects had noteworthy moves that are worth mentioning:

- Enjin (ENJ) looks to be the beneficiary of both circumstance and thematic plays, as crypto-based gaming has reportedly taken off since quarantine began. Enjin has been quite active as one of the leading blockchain gaming platforms, announcing a new game, promoting another, updating their token use case for in game purchases, as well as teasing the release of yet another game. The token has responded favorably, finishing the week up 42%.

- Huobi Token (HT) was approved as a compliant crypto asset by the Japanese Financial Services Agency, becoming the first exchange token to receive such designation. With Japan recently tightening its regulations to better define digital assets, the compliance designation should be seen as a positive sign for Huobi’s exchange token. HT will begin trading on Huobi Japan starting in May, joining 25 other compliant tokens that have already been approved. The market reaction itself wasn’t as noteworthy, as HT finished the week up 3%.

What We’re Reading this Week

Last week, Bloomberg published a dedicated report on crypto highlighting Bitcoin’s maturation as an asset and its move towards becoming digital gold. The report also highlights the crypto functions on the Bloomberg Terminal for retrieving a full page of crypto information, displaying a selection of top 20 tokens along with venues for Bitcoin products such as CME and Grayscale. Bloomberg highlights the maturation of the Bitcoin futures market which has reduced the volatility leading to a “taming of the highly speculative bull market”.

According to reports from local news outlets, local governments in the Hubei province held a meeting to discuss the pilot and eventual rollout of the Digital Yuan, called DC/EP. The meeting involved government officials, representatives from the state-owned banks, Ant Financial, Tencent and 19 restaurants/retail shops which plan to participate in the pilot. Although there has been no confirmation on timing for an official launch, numerous reports out of China indicate that a full rollout is coming in the next few months.

A recent project out of IBM’s blockchain unit, Rapid Supplier Connect, is a blockchain-based platform that aims to connect healthcare providers with non-traditional vendors for medical equipment supplies. In a time of widespread shortages of necessary medical equipment, Rapid Supplier Connect offers to reduce the time needed to source and vet new vendors for equipment. There are about 200 companies currently on the platform that are non-traditional makers of medical equipment and therefore wouldn’t otherwise be able to get their equipment to healthcare workers. In addition to IBM’s project, Ernst & Young’s blockchain unit is looking into producing a platform for tracking individuals with COVID-19 antibodies. Blockchain may finally make its way into the mainstream, accelerated by the Coronavirus pandemic.

Where most countries have shied away from advocating strongly for a digital currency plan, the Netherlands has taken the plunge, stating it wants to be the world leader in developing Central Bank Digital Currencies (CBDCs). According to a bulletin posted by the bank last week, the use of cash is declining in the Netherlands and it should provide an alternative method of payment that better suits their citizens’ needs. The bank further stated that central bank-issued money is necessary to preserve trust in a national currency and government, therefore the necessity of issuing a CBDC outweighs any risks.

A real estate portfolio containing $300m of office and hotel properties is set to be tokenized on tZero’s security token platform. To start, $90m worth of properties will be tokenized, representing hotels in Costa Rica and Pennsylvania, and will be available for secondary trading on tZero and issued on the Tezos blockchain. Traditionally, real estate investments have been paper-heavy processes with little to no secondary liquidity. Tokenizing these assets will decrease the paperwork involved in managing these securities while allowing accredited investors to access them for their portfolio.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

Source: Digital Assets Data

Source: Digital Assets Data