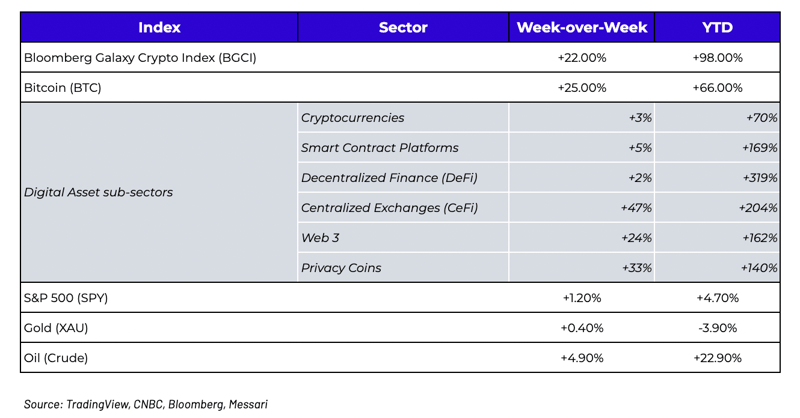

What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 2/14/21)

How many times can bitcoin rally on the same news?

It turns out...quite a few. Last week, bitcoin rallied multiple times throughout the week, ultimately gaining 25%, as a plethora of “new” announcements about increased adoption sent bitcoin incrementally higher. In fact, it may have been the heaviest news week on record.

- Tesla announced a $1.5 bn purchase of bitcoin from its Treasury

- BNY Mellon and Deutsche Bank revealed crypto custody plans

- Mastercard announced support of “select cryptocurrencies”

- Morgan Stanley said they are considering investing in bitcoin, and JP Morgan announced that they would consider trading it if client demand increased

- The mayor of Miami announced that Miami is exploring paying workers and collecting taxes in bitcoin

- Twitter and Uber announced they were considering adding bitcoin to their balance sheets

The last few announcements weren’t even announcements -- they were announcements about possible future announcements. These bitcoin soundbytes have been coming fast and furiously since early 2020 when Paul Tudor Jones first made it socially acceptable to talk about bitcoin publicly, and the floodgates have been open ever since with major announcements coming from asset managers, insurance companies, corporate treasury departments, FinTech companies, legacy financial institutions, celebrities and government officials. While some of these announcements have been very well thought out (like those from Paul Tudor Jones, Microstrategy and Ray Dalio), the more recent ones can be summarized as follows:

“We don’t know much about bitcoin or cryptocurrencies or digital assets, and we certainly don’t have anything new to add, but we are getting involved now because everyone wants us to, and now that we are, we’ll write the exact same opinion research piece that everyone else has written, and then we’ll go on CNBC or Bloomberg and talk about our newfound expertise.”

That’s not even meant to be demeaning. There simply isn’t that much new to say about bitcoin at this point -- it’s an incredibly complex technology with an incredibly simple investment thesis. In totality, of course, all of these announcements matter a great deal. We’ve gone from “the institutions are coming” to “the institutions are here”. But at this point, each and every scenario for new adoption should already be baked into the market price. Markets are driven by expectations, not reality, and at this point it should be 100% expected that more “adoption announcements” are on their way. And per the law of diminishing returns, each incremental announcement should have an incrementally lesser effect… but in reality, the opposite is happening. Each incremental announcement is causing even more excitement.

Take Tesla for example. Bitcoin has now rallied three different times on Elon Musk / Tesla related bitcoin news -- when Musk first tweeted about bitcoin in December, when he changed his Twitter profile to “#bitcoin” a few weeks ago, and ultimately when the Tesla 10-K revealed that Tesla had purchased $1.5 billion of bitcoin. This is certainly not insignificant news -- but it also doesn’t create a material change of opinion for most investors. If your base case was that no other corporate treasury departments would ever buy bitcoin, you’d be crazy and already very wrong before this news came out. If your base case was that every corporate treasury department would buy bitcoin, then Tesla’s announcement is just N = 1, and it wouldn’t change your view materially. Therefore, the only significant news here is that the media and retail love everything related to Elon Musk and bitcoin. It’s certainly a marginal net positive, but it mostly just validates whatever thesis most everyone already had, rather than introduce a new data point.

Bitcoin price action following three (arrows) significant Elon Musk / Tesla related Bitcoin announcements

.png?width=512&name=unnamed%20(54).png) Source: TradingView / Arca Estimates

Source: TradingView / Arca Estimates

This may just end up being the year of announcements, where the market decides that each new data point is important even if it ultimately changes nothing. We see this in more traditional markets too, usually during bull markets when analysts and traders are just looking for any excuse to take positions higher. Equity and rates markets often react each time a Fed governor speaks, even if the individuals simply reiterate what was already said at a previous FOMC meeting. Similarly, when a company pre-announces earnings and then ultimately releases actual earnings weeks later, you often get a response to both events even if it should have already been priced in.

The only new news here is that public companies will do whatever it takes to make their stock prices go higher, asset managers will do whatever it takes to attract new investors, and financial institutions will do whatever it takes to attract and retain customers. As such, these announcements are not going to stop, because they are working. Back in August 2020, we wrote:

“...corporate finance departments are always paying attention to what their competitors are doing, and what drives their stock prices higher. With that in mind, a small business intelligence company, Microstrategy, announced last week that it purchased 21,454 bitcoin as part of its capital allocation strategy (~$250 million). The purchase was done in an effort to “maximize long-term value for shareholders”. MSTR stock jumped 20% following the announcement last week, most likely leading to long weekends for junior employees at corporate finance departments around the world as they furiously research bitcoin. Remember back in 2017 when companies would go out of their way to mention “blockchain” on earnings calls even with no knowledge or intention of how to actually use blockchain, simply because the market was rewarding companies for being ahead of the technology curve? Get ready for bitcoin redux.”

The future has become the present.

The Wall Street rush will expand beyond bitcoin to other categories of digital assets

When Teslacoin? This is actually a great question.

.png?width=418&name=unnamed%20(55).png)

As the old golf saying goes, “Drive for show, putt for dough”. The same can now be said about bitcoin versus other digital assets. Bitcoin gets all the headlines, while other digital assets often make investors and companies all of the money. We love bitcoin, but again, it's a very simple thesis with a limited future evolution. But outside of cryptocurrencies, the rest of the digital assets space is breaking down barriers left and right. We’ve been on record many times saying that the three other types of digital assets (platforms, asset-backed tokens, and pass-thru tokens) are the greatest capital formation and customer bootstrapping mechanism ever created. We’ve discussed the ESG angle and the customer incentive angle, amongst plenty of other writeups and speeches explaining why every company in the world will eventually have a pass-thru token and/or asset-backed token in its capital structure.

In the last section, we suggested that none of these newfound bitcoin reports or theses add any actual value. But as large banks, brokers, custodians and asset managers get more comfortable in the digital assets world, they will start having a positive effect. It just won’t have anything to do with bitcoin or cryptocurrency.

Prediction time! After finally learning about bitcoin and cryptocurrencies in 2020, Wall Street and Institutional Investors will begin to learn about other types of digital assets, and this will come in stages:

Stage 1: Research coverage and M&A of bitcoin related companies

Investment banks and broker/dealers are scrambling right now to "cover bitcoin'' as fast as they can. There is money to be made trading bitcoin and bitcoin tracking stocks, as well as M&A fees, and the Street wants their piece of the pie. Unfortunately, Wall Street is not set up to trade bitcoin directly, so they have to find other ways to insert themselves into the money grab. At first, this will mean writing research on publicly traded companies and trusts that directly or indirectly track bitcoin (BITW, GBTC, GLXY CN, VYGR, HUT, SI, EQOS, MSTR, and of course the upcoming Coinbase direct listing). There has been a huge infrastructure push around bitcoin, and a handful of large companies have grown from bitcoin’s success. While this is a start, it’s a very limited pool of securities to focus on, and doesn’t come close to fully encapsulating all of the growth of this industry (more on that below). Second, this really isn’t much of a value-add service as those who want bitcoin exposure can now get it directly pretty easily. Most of these stocks essentially trade like bitcoin tracking stocks, regardless of whether or not their profits are directly tied to bitcoin’s price, making any research less impactful.

Stage 2: Investing and writing research on the other types of digital assets

So let’s move beyond bitcoin. Wall Street is great at repackaging and tweaking the same basic structures over and over again. Fortunately, this has already happened in digital assets, but most of the world doesn’t know these investable instruments exist. In 2021, banks and broker/dealers will begin to discover the three other types of digital assets besides “cryptocurrencies” -- and these offer much more flexibility and potential than bitcoin. The amount of business that will come from these structures will dwarf any bitcoin or bitcoin-like trading fees. Once these other types of digital assets enter the vernacular, it’s off to the races in terms of structuring deals.

The four main types of digital assets are:

- Cryptocurrencies / Money - Examples: bitcoin, Tether, USDC.

While there are some competitors to bitcoin, it’s very unlikely that any of them will dethrone the king when it comes to investment dollars. That said, the growth in stablecoins has been phenomenal.

- Decentralized protocols and platforms - Examples: Ethereum, Polkadot, Flow, Tezos, Cardano, EOS.

These are base layer foundations for applications built on blockchain technology, much like HTTP, TCP/IP and SMTP protocols which eventually enabled internet and email applications. For those less tech savvy, think of platforms as the IOS App Store that power all applications that run on Apple’s software.

- Asset-backed tokens - Examples: GnosisDAO (GNO), Nexus Mutual (NXM), Spencer Dinwiddie’s SD26 token backed by his NBA salary, Arca’s own tokenized ‘40 ActUS Treasury Fund, ArCoin

Asset-backed tokens are tokens backed by equity, debt, hard assets or recurring income streams. Just like ETFs paved the way for lower fees and increased liquidity for any investable asset, blockchain-based products will increase transactions, reduce middleman, and open the door to new investable assets and structures.

- Pass-Thru Tokens - Examples: HXRO, BNB, FTT, CHZ, AXS, UNI, SUSHI and hundreds of others

Pass-Thru tokens are hybrid securities -- part loyalty reward program, and part quasi-equity instrument. These are often issued by companies to bootstrap company growth and incentivize customers. Often, revenue and profits are passed directly to tokenholders via dividends, rewards or buybacks. This is analogous to combining the Amazon Prime customer (rewards) with the Amazon shareholder (economic gain), so that users of a company’s product are financially incentivized as well.

Stage 3: Underwriting tokens, as non-native crypto companies begin to issue tokens

Protocols and platforms by themselves are not “bankable”, but companies that issue asset-backed tokens and pass-thru tokens on top of these protocols will have banking needs. We believe that every company with a retail customer base will eventually have a pass-thru token in their capital structure, from Starbucks and Delta, to Tesla and Amazon, to your local mom-and-pop restaurant, barbershop and gym. The faster investment banks learn about this type of digital asset, the faster they will help small and medium-sized companies bring well-structured tokens to market. This is similar to the private placement market from 20 years ago, which started small, but now has over $1 trillion in outstanding debt and equity. Granted, there are still regulatory uncertainties, but these will begin to diminish as precedent is created from large companies who are willing to push the envelope.

A lot has changed since the 2017 ICO tokens were issued by loosely formed companies and entities purely as early stage venture-like fundraising mechanisms.. The new batch of 2020+ tokens are all about aligning incentives amongst stakeholders (founders, developers, customers, liquidity providers and investors), and digital assets have become the single best capital formation and customer bootstrapping vehicle for fostering this growth. The best token designs will be those that incentivize customers to take a risk in adopting new platforms and services before the value proposition fully emerges, and these early adopters will be rewarded via increased token prices that have future value based on how much token holders contribute to the company’s growth.

What’s Driving Token Prices?

While the numbers are impressive (of the Top 100 by market cap: 25 finished up 50%+, 57 finished up 25%+, and only 10 assets finished down), there is arguably more telling anecdotal data. Bitcoin (and digital assets as a whole) have been discussed in every facet of our lives right now, from group chats to phone calls to the grocery store to the dinner table. As with 2017, the vast majority of the discussion (un)surprisingly revolves around assets not named Bitcoin. Everyone has heard of Bitcoin at this point, but the interest is spilling over to the rest of this space. The best word to describe what is driving token prices as of late is intrigue - and there is quite a bit of it at the moment.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency