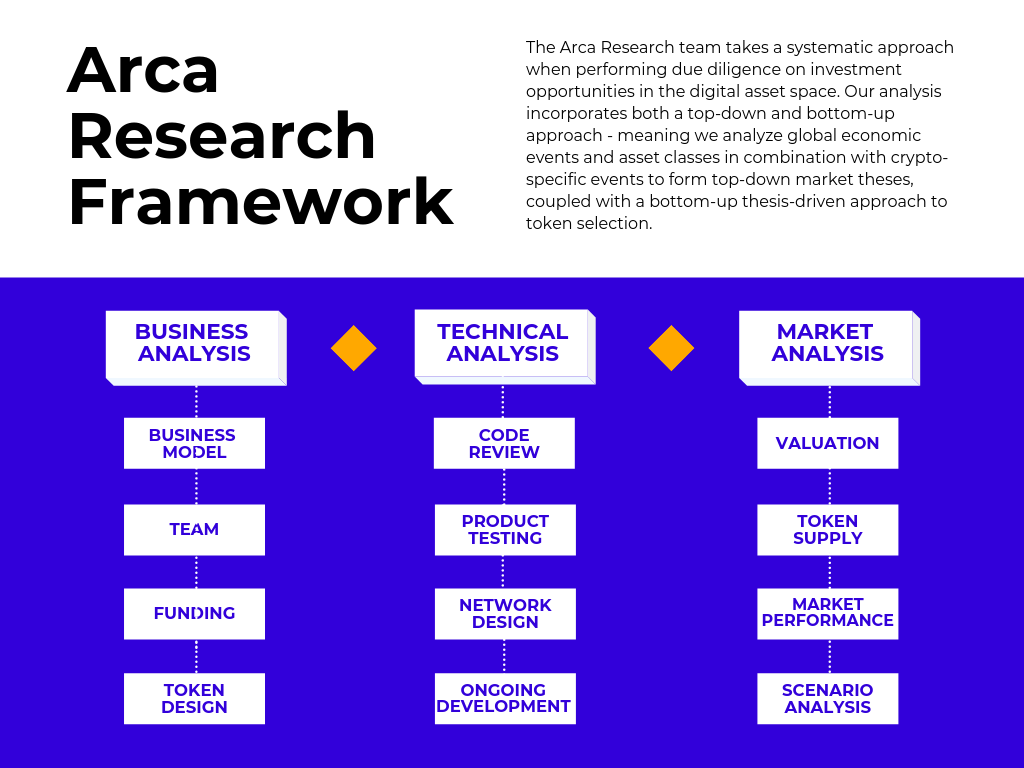

The Arca Research team takes a blended approach to performing due diligence on investment opportunities in digital assets, leveraging our backgrounds in capital markets, equities/credit investing, M&A, venture capital and early-stage technology. Our analysis incorporates both a top-down and bottom-up approach -- meaning we analyze global economic events and digital asset classes in combination with crypto-specific events to form top-down theses, and use a bottom-up thesis-driven approach to token selection.

Top-down Macro Approach

In addition to the deep diligence performed on the actual token, we use a “top-down” approach where we consider all the factors external to a token that could impact price and performance. Macroeconomic factors that impact how digital assets will perform include, but are not limited to, potential trade wars (China), potential real wars (Iran), Brexit, Quantitative Easing, and newly introduced regulations. In addition, while holding these positions, the team monitors macro indicators to ensure we are positioned correctly as conditions change.

Bottom-up Security Selection

A “bottom-up analysis” involves looking at all aspects of the token. We divide our analysis into three components:

- Business Analysis

- Technical Analysis

- Market & Valuation Analysis

Business Analysis

The main purpose in this analysis is to determine if the token solves a real-world problem or pain point that will make it a viable product for years to come. To that end, for each token, we review the team, the business and growth plans, the token’s design and any other factors that will affect the token’s success.

A bit of background: tokens are not organized like traditional corporations and do not represent ownership stakes like equities or liabilities like debt. Instead, each token has unique characteristics that run the gamut from revenue shares, to user rewards/incentives to group governance features. Generally, the creators of a project conceives and launches a token. This project can be backed by a not-for-profit foundation, a completely decentralized set of developers, or an existing for-profit business. Therefore, it is important to understand the structure of the entity behind the token project in addition to evaluating the leadership and business.

Business Model

It is important to understand how the underlying business operates, except in cases where a token project is backed by a decentralized set of individuals (i.e. a band of volunteer workers that freely contribute to the development of blockchains, such as Bitcoin and Ethereum).

- How is the business backing the token structured?

- If the business is not a set of decentralized players, how did the project come together?

- Was it an existing business that chose to pivot into blockchain, or was it a newly created company that had a vision to launch a token?

Existing businesses can generally be bucketed into two groups: thoughtful and tactical pivots and bandwagon pivots. For thoughtful and tactical pivots, a company’s existing business is relatively successful with a robust customer base, and its product is improved by incorporating blockchain technology and a token. Although the execution of this pivot must also be evaluated, in general, an existing user base could theoretically adopt a token, jumpstarting token usage. On the other hand, there are bandwagon pivots: existing businesses that force their business to use blockchain technology and issue a token. Although not as commonly seen as in 2017 and 2018, existing businesses have frequently used the rise of digital assets as a way to raise non-dilutive funding. It was common to publish a white paper and create a token overnight, without considering if blockchain was a strategic fit for the business. The most famous example of this is the Long Island Iced Tea Company, which added “blockchain” to the end of its name, leading many to ask how do blockchain and refreshing beverages intersect?

Team

When reviewing team members and leadership of a project or business, there are a key set of components to review:

- Has the team previously founded a business? Was it successful?

- Has the current team worked together before?

These circumstances are indicative of the ability for a team to work together to bring a product to market and stay successful long term. For example, disputes among the MakerDao founding team led to a spate of bad publicity, as the CTO and CEO disagreed over the direction of the project, with the CTO eventually departing. It’s not always possible to predict, but founder fallout, cited as the number 12 reason startups fail, is a risk that must be considered.

Funding

Knowledge of a project’s funding and stakeholders is also critical to understanding the team’s incentives and the project’s potential growth.

- What was the funding mechanism?

- If the project is backed by a for-profit company, does that company have any outside equity investors?

- Who are these outside investors - friends and family or venture capital firms?

- Did the project receive funding through grants, community contributions or a mechanism such as an Initial Coin Offering (ICO) or Initial Exchange Offering (IEO)?

If capital was previously raised in equity rounds, it could indicate a project is more likely to be successful with future fundraising. It could also indicate that the project is less likely to fail, since these projects have larger groups of stakeholders. Conversely, the existence of equity investors alongside token investors could prove to misalign goals as the equity investors desire the value of the equity to increase, which may not be tied to an increase in the token’s value.

Token Design

Finally, the token itself must be evaluated using a cryptoeconomic analysis. Cryptoeconomics is not a crypto version of economics but it is “the use of incentives and cryptography to design new kinds of systems, applications, and networks” (Source: Coindesk). Some components of this analysis include determining the purpose and necessity of the token in the ecosystem, and if necessary, does it accrue value long term?

- What function does the token serve?

- Is it a store-of-value/currency, a utility, or a security token?

- Does the token make sense and serve a purpose in the ecosystem? And if it is necessary for the ecosystem to function, how does it accrue value long term?

This is the hardest concept to understand when diving into digital assets for the first time as these networks are built using new and unique incentive mechanisms that did not exist prior to the birth of Bitcoin in 2008.

Technical Analysis

Tokens are ultimately technologies, so a technical analysis is critical to understanding the potential future success of an asset. Aside from reviewing the actual code and product, the other considerations include the token network’s design and the engagement and progress of its development team to date.

Code Review

A unique aspect of token projects is that generally most code is built in an “open-source” manner, meaning the project’s code is available to the public. If a project is live and released, the research team will review the code to determine how robust it is and if development progress is being made.

- How secure is the system?

- How robust is the QA testing?

- Have there been past technical issues?

- What coding language is being used?

Coding language is also critical as many of the languages used in the development of token projects are new and untested, thereby increasing the learning curve for new developers.

Product Testing

A review of the final product is just as important as a review of the underlying code. When available, the research team tests out the product with the goal of delivering usability feedback. Not every token has a testable, consumer-facing product. Larger protocols such as Ethereum and EOS have decentralized apps (dapps) built on top of them that can be tested out, allowing the research team to understand the features each blockchain offers. For example, playing CryptoKitties on Ethereum and EOS Knights on EOS offer vastly different experiences as the speed on EOS is much faster providing a smoother user experience. Some questions we ask while testing these products include:

- How easy is it to use?

- What is the lag time?

- Are there too many additional steps to use the blockchain-based product versus a non-blockchain product?

- How does the experience differ from one blockchain to another?

Product testing is crucial as every product described in a deck or white paper sounds great in theory until you experience its slow, clunky user interface which serves as a barrier to adoption.

Network Design

Before beginning, we must categorize where in the technology stack the technology sits. Broadly, these technologies can be divided into protocols, middleware, or applications and the analysis varies depending upon the category of technology. Review of the overall network design aids in the understanding of the different trade-offs each network’s technology offers which ultimately dictates its chances for mainstream adoption.

- What type of consensus mechanism does the network use: Proof-of-Work, Proof-of-Stake, or a Hybrid Model? Each model has its own advantages and disadvantages that affect long term adoption.

- What is the goal of the network: scalability or security? Ethereum is considered slower, however, it is a more secure system as the consensus process is distributed among thousands of nodes. Its competitor, EOS, offers far faster speeds at the cost of security, with the consensus process conducted among only 21 nodes.

- Are there single points of failure within the system? Although Ethereum is decentralized, many applications rely on Infura, a back-end infrastructure service that allows users to easily access Ethereum applications, creating a single point of failure.

Engagement and Ongoing Development

Like any technology, blockchain projects require upgrades and maintenance. This maintenance is usually done by the initial creators of the project and any outside “contributors”. As these projects and their code development is open-source, it is easy for an outsider to peek in on these projects at any time and see what is being worked on and by who. This provides another way to measure a project’s progress and engagement above and beyond what may be publicly reported. It is common to find projects with slick websites and marketing materials, only to find a virtual ghost town upon inspecting their Github repositories. Constant developer engagement is a great tool to measure the health of projects long term.

- What is the quantity of code submitted?

- What is the quality of code submitted?

- What are the number of developers contributing to the project?

- How much code is being contributed by each developer?

- Is the published development roadmap on schedule?

- Are major planned updates being delivered on time?

It’s important to review not just the metrics of each project’s development (number of developers, number of code pushes), but also the quality of what is being released. In many cases, projects will try to game the system by releasing code in smaller amounts to artificially inflate their metrics.

Market and Valuation Analysis

The final part of the analysis considers the valuation, supply and issuance, and market performance of a token in order to create a scenario analysis to assess all the potential outcomes for a token.

Valuation

Cryptoassets are still in their infancy and are therefore hard to value using traditional valuation models. Many of the models in existence are unproven, as they only use a few years of data, and some models have yet to be discovered. Below are a few of the most commonly used methodologies:

*Crypto-specific valuation method.

Each of these methods has advantages as well as shortcomings and some are more appropriate for specific token types. Tokens are unique, similar to corporate bonds. Just like a bond has different coupons, different maturities, different covenants and different features (callable, putable, convertible, warrants, etc), most digital assets have unique features as well, making each analysis different than the last. The DCF analysis is best used for tokens issued by cash-producing companies such as exchange tokens like Binance Coin (BNB) or Unus Sed Leo (LEO). The NVT Ratio may be better when comparing across smart contract platforms such as Ethereum (ETH), EOS (EOS) and NEO (NEO). A Total Addressable Market analysis can be used for tokens that are in the early pre-launch stage or are servicing a sector that is difficult to currently measure.

Token Supply and Issuance

The research team must also analyze a token’s supply and issuance schedule in order to understand how it might impact price.

- Is the token supply fixed to a finite amount? Some tokens, such as Bitcoin, have a fixed supply and issuance schedule, creating scarcity value as there are fixed amount of tokens in existence and the amount of tokens issued decreases over time.

- Is the token supply inflationary? Other tokens, have inflationary mechanics, in which more tokens are issued indefinitely and are awarded in some fashion, usually in PoS networks.

- How are new tokens issued? In mining networks, new tokens are mined (BTC, ETH). In staking networks, new tokens are awarded to users who stake their tokens to secure the network (EOS, NEO).

- Does a token have a burn mechanism? For example, BNB burns tokens and removes them from circulation forever.

- What is the non-technology contingent supply schedule? Supply is also not just limited to the programmatically determined supply in a token network, but also how the supply was originally issued. If a token project raised funds via an ICO, usually the entire supply of tokens are not sold to the public. Only a portion is sold publicly with the remainder “locked” for the founders, team, and early investors and some saved for future community engagement. Understanding these supply schedules is key to projecting out a token’s performance.

Market Performance

Historical market performance is also an indicator of future performance.

- How has the token traded to date?

- Has it traded considerably above the initial issuance price or under it?

- How do certain pieces of news positively or negatively impact price?

- What is its correlation to other assets?

- What is its beta to the market? Its up and down-capture?

Assessing all of these metrics allows research to form a clear picture of how a token might perform within the overall portfolio.

Scenario Analysis

After processing all of the above information, research builds out a scenario analysis that takes findings from across all three pillars (Business, Technology, Market & Valuation) into account. The purpose is to ensure that the portfolio team is well aware of the upside potential, and the downside risks involved with putting on a long term position in that token. The analysis projects out four scenarios for the token:

- Base case

- Upside case

- Downside case

- Armageddon case

Each case is then assigned a percentage likelihood of occurring. The purpose of this exercise is to test out the team’s conviction and identify weak spots or strong points in each token.

Conclusion

Digital assets and token projects are a new asset class and are therefore a constantly-evolving field. We believe that based on the unique features of digital assets, we should use a framework that encompasses the business, technology, and market and valuation. Our goal at Arca is to continue iterating upon our process as the space develops, along with our knowledge and expertise.

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)

.png)

.png)

.png)