What happened this week in the Crypto markets?

Bitcoin STILL Did What it Was Supposed to Do

The crypto markets had a tough week, falling 8% on average. Most of this occurred in an orderly fashion, but there were a few short but violent breaks lower, each of which was immediately bid back up. At one point, the entire market was down over 15%.

Two weeks ago, crypto enthusiasts celebrated when Bitcoin rose 15% during a single week when global turmoil sent equities down almost 4%. At Arca, we even argued that Bitcoin reacted exactly as it was supposed to, serving as a flight to quality asset.

Naturally, this past week had many pundits scratching their heads, as this flight to quality theory was seemingly ripped to shreds when Bitcoin sold off while global equities once again declined. Even a massive selloff in the Argentina stock-market and subsequent declines of the Peso following a surprise election did nothing for the Bitcoin safe-haven narrative.

The extreme magnitude of the moves in Bitcoin, and the resultant volatility, certainly garners headlines and in some cases warrants investor caution. But taking a step back, the direction of Bitcoin both up and down this month has made perfect sense. We started the month right around $10,000, which was somewhat of an equilibrium level after the market finally worked itself out from extreme overbought conditions and excessive leverage that had built up in June and July. And three weeks later, we’re still slightly above $10,000.

So let’s recap the events that took the market up and back down, starting on August 1st.

In the first few days of August, we had 3 macro events that were wildly bullish for the Bitcoin narrative, so it wasn’t surprising to see Bitcoin spike 20% higher:

- A Fed rate cut (symbolic of inflationary monetary policy)

- Trump's announcement of further China tariffs (Trade war)

- The devaluation of the Chinese Yuan below the critical 7.0 level (inducing capital flight)

This past week, however, all 3 of these factors reversed, so naturally, Bitcoin retraced back to where we started the month:

- The Yuan stabilized and China made it very clear that this was going to be an orderly decline

- Trump walked back his tariffs until after the important Christmas shopping season

- Positive economic data (plus a hawkish CPI release) and Powell’s comments suggest future rate cuts may not be imminent.

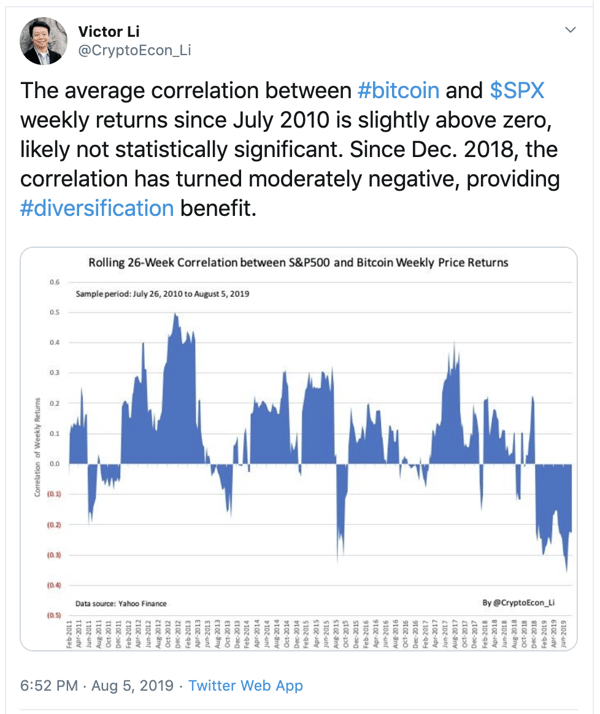

Combine all of this with rising global market volatility, while also recognizing that Bitcoin and the rest of the non-currency digital assets are still risk assets in addition to having certain "flight to quality" and "safe haven" properties, and the moves make perfect sense when viewed through a wider lens. Further, let’s not lose sight of the fact that Bitcoin is not negatively correlated to global markets. In fact, it is perfectly uncorrelated, with just a few periods of negative correlation prevalent only during very specific macro events.

The fact is, Bitcoin is still a tiny asset relative to the rest of the global markets, so it doesn't take much to push Bitcoin one way or the other. The direction matters more than the magnitude, and there may be time delays. While we have no idea if Bitcoin will go higher from here, it does seem safe to say that Bitcoin will remain very well bid and every dip will be bought as long as this global macro instability remains at the forefront (and Bitcoin is currently +3% in August vs equities -3%).

When Will Bitcoin Be a True Macro Hedge?

We argued above that Bitcoin, in some ways, is directionally acting as a macro hedge, albeit imperfect. But it is of course not practical to believe that a large number of global market participants are using Bitcoin in this manner in real-time. Conversely, it is therefore obvious that investors cannot be selling Bitcoin immediately when markets go back to "risk on". As a result, the moves may be more narrative than reality… so far. But this is largely due to the fact that there is very little overlap between the crypto markets and the traditional markets.

- Crypto specific funds have difficulty trading equities and gold, since there are no Prime brokerages in crypto, and most banks won’t allow you to move assets freely between crypto and non-crypto.

- In the traditional world, financial advisors still don’t have easy access to crypto (the Bitcoin ETF was once again delayed), and while macro funds are using BTC futures sparingly, most still don’t have mandates that allow for digital wallets or custody of digital assets.

But this crossover is on its way… sooner than many realize, and when it happens, Bitcoin really will start to exhibit real-time safe-haven and flight to quality behavior. Fidelity Digital Assets is now trading Bitcoin with a select few customers, and virtually every financial institution can onboard with Fidelity immediately. Bakkt (owned by ICE) just got final approval to trade physically settled Bitcoin Futures, giving institutions an end-to-end regulated system approved by the CFTC and NYDFS. Other financial institutions offering crossover appeal include TD Ameritrade, eToro, Robinhood, Square and a host of others.

When old world collides with new world -- narrative becomes reality.

Questioning the Status Quo

David Rosenberg, Chief Strategist at Gluskin Sheff and former Chief Economist at Merrill Lynch, is no stranger to bearish takes. But his latest macro note to clients pointing out the risks caused by stresses in today’s market was notable for a different reason.

Instead of arguing why equity investors are wrong, he challenged equity investors to think about what they may be missing.

Mostly, everyone I speak to lives in the here and now. They seem more interested in telling people how crazy cheap the stock market is and how crazy expensive the Treasury market is, rather than trying to look at the current environment in a historical perspective. Instead of telling people there is no recession, these bulls should be discussing why the markets are busy pricing one in. What do these pundits know that the markets don’t know? We have a bond market in which a quarter of the universe trades at a negative yield. The long bond yield has gone negative in Germany. More than half of the world’s bond market is trading below the Fed funds rate. Investment grade yields, on average, are below zero in the euro area. This is completely abnormal because it reflects an abnormal economic, financial and political backdrop.

With that in mind, let’s assume the rates curve is right and we’re heading towards a global recession. Whether this is a mild recession, or a full blown debt implosion, remains to be seen. Regardless, company revenues would undoubtedly suffer. With that in mind, maybe it’s time for big corporations to question the status quo as well. What if equity and debt structures aren’t the best way to raise capital, and instead, non-dilutive capital with community governance features (as seen in many digital assets) makes more sense? Perhaps selling products to customers with little loyalty to their brand isn’t the best way to grow revenues, and instead, providing utility for their best customers would ultimately attract more capital? Consumer behavior is changing, and companies need to adapt.

Inevitably, if we enter a recession, companies will be doing everything they can to cut costs. But perhaps it would serve them better to think of additional revenue line items, ones that live outside of traditional corporate thinking. In today’s culture of rent vs buy (Uber, AirBNB, etc), companies with similar customers could band together to create experiences instead of products, and use digital assets to create these experiences while simultaneously creating revenue.

As an example, let’s take the outdoor recreation industry. Dick’s Sporting Goods, REI, Bass Pro Shop and countless other mom and pop shops have a common goal of increasing outdoor recreational activities. All of these companies could team up and create an outdoor advocacy group, and issue a joint “Outdoor token”. This token could be sold to all outdoor enthusiasts, be booked as a new line-item of revenue (pro-rata), and could be used for discounts at their stores, exclusive access to trips / parks, and many other VIP-level experiences. As a result, instead of worrying about brand loyalty and stealing from the pie, these companies would work together to grow the pie. Token-holders would be incentivized to purchase more tokens as their experiences increase, creating more revenue for each company issuing the token. And each token-holder immediately becomes an incentivized evangelist, as creating more outdoor enthusiasts creates demand for their tokens (which subsequently increase in price).

There are solutions out there to the political, economic, and financial woes that are here, and building. It’s time to question the status quo.

Notable Movers and Shakers

Bitcoin volatility continues to be a reality (-10% week-over-week), with turbulent worldwide market conditions dictating the narrative. Last week was generally quiet, with a few projects releasing updates:

- Stellar (XLM) redesigned their website and updated their SDK for developers in an attempt to attract developers to build payment applications on their protocol. Remittance tokens such as XLM have suffered over the last year, and this redesign looks to be an attempt to re-attract those who have shied away as of late. The token, however, did not receive any significant boost from this news, falling in line with the market (-10%).

- Flexacoin (FXC) announced in a blog post Tuesday that they have started the process of launching their product in Canada, with full support by the first week of September. With over 7500 merchant locations lined up in Canada, current U.S. users will be able to spend cryptocurrencies across the border without dealing with foreign exchange rates or fees. The market for FXC is quite thin currently, with FXC finishing the week down 2%.

- Beam (BEAM) completed their first scheduled hard fork at block height 321,321 on Thursday. The privacy token is focused on levelling the playing field for miners, and as such uses scheduled hard forks to ‘brick’ Application Specific Integrated Circuit (ASIC) miners that normally take the lion’s share of the mining pool. This hard fork completed successfully, and the price reacted in kind (+28.5%).

What We’re Reading this Week

Will China prevent massive capital outflows with the currency devaluation? That’s Beijing’s latest concern according to the WSJ. After a “botched” devaluation in 2015, when billions of dollars flowed out from China, handling the devaluation this time around needs to be done delicately. Capital flight should prove harder as China has added over 75 capital-control adjustment measures over the last few years. On the flip side, continued international borrowing from Chinese property developers and corporations will suffer from devaluation as their loans are denominated in dollars.

In Blockforce Capital’s July commentary, the firm discusses a theory for why Bitcoin and other cryptocurrencies experience such high levels of volatility. They point to the 24/7 nature of crypto trading as the culprit. While often touted as only having 9 years of trading data, the non-stop trading environment equates to 35 years of trading data to draw when compared to traditional trading hours of equity markets. In addition, it shows that Bitcoin is uncorrelated to the S&P 500 as one would expect volatility to be reduced outside of trading hours, which is not the case.

In a completely unsurprising move from the SEC last week, the applications for rule changes that would allow for a Bitcoin ETF product from Bitwise and VanEck were postponed last week. The new deadline for a decision has been pushed to mid-October. The SEC’s main concern with approving such a product is athe “theft and manipulation on exchanges”.

The Intercontinental Exchange’s subsidiary, Bakkt, has been cleared to launch its platform for physically-settled Bitcoin futures. The exchange has set a launch date of September 23 when it will offer monthly and daily Bitcoin contracts. Bakkt’s launch has been highly anticipated for many months now offering “customers unprecedented regulatory clarity and security alongside a regulated, globally accessible exchange in a market underserved by institutional-grade infrastructure.”

In this data-packed report, Electric Capital provides a comprehensive update of developer activity on open-source crypto projects for the first half of 2019. Overall, the findings show that total developers fell slightly from January to June. This decline comes mostly from projects outside the top 100, indicating that a number of ICOs lost full time developers during this period as funding dried up. Ethereum development stayed roughly the same during the same time period with 18% of all developers in the space working on it. MakerDAO grew by almost 80%, in terms of new full-time developers, while Bitcoin Cash fell 32%.

You read that right. Last week Walmart submitted a patent for an “unmanned aerial vehicle (UAV) blockchain-based coordination system”. The system will capture and transmit a drone’s identifying and flight information in order to preserve data integrity. This is an important feature in coordinating unmanned vehicles.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)