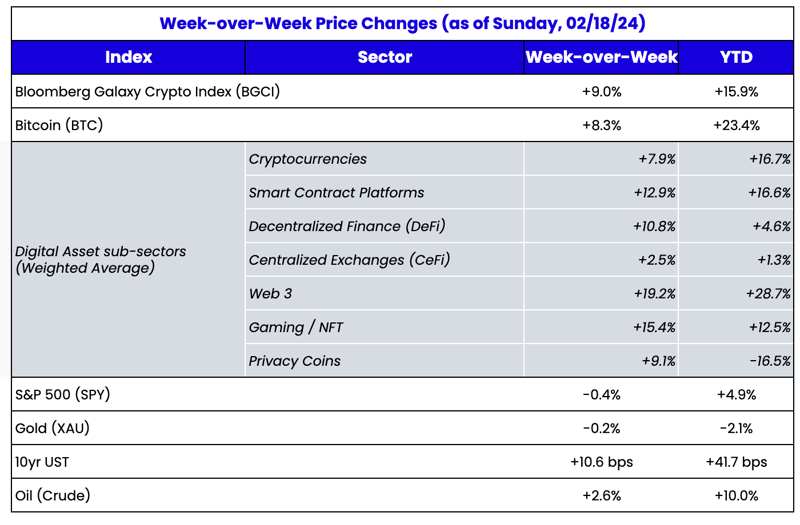

Source: TradingView, CNBC, Bloomberg, Messari

2 of 3 Major Hurdles

Continued momentum last week pushed the total digital assets market capitalization above $2 trillion, a milestone last seen in March 2022. Much of last week’s move higher can be attributed to Ethereum (ETH), which outperformed both BTC and SOL - a relative value move that has not occurred much since 2022.

Source: Coingecko

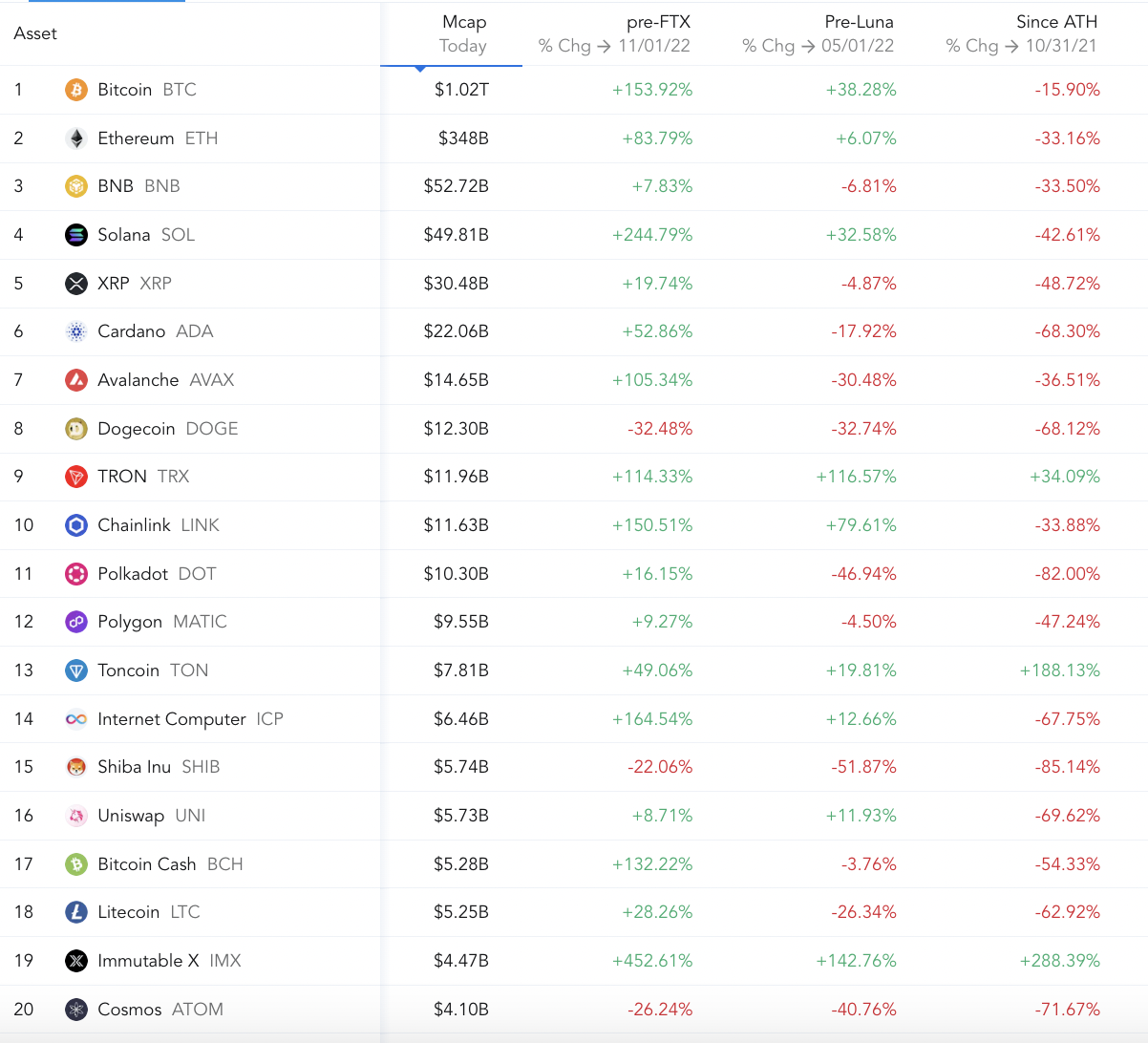

In fact, following the February advance and ETH’s move higher, a significant number of tokens, including BTC, SOL, and now ETH, are above pre-Luna collapse levels (May 2022). Recall, earlier this year,

we discussed a few major hurdles that the digital assets market needs to clear before retracing to new highs:

- November 1, 2022: Prior to the downfall of FTX (Nov 8) and a further cascade of defaults from DCG/Genesis and others, followed by a period of window dressing where anything owned by TradFi was sold indiscriminately into year-end (SOL, GBTC, COIN, etc).

- May 1st, 2022: Prior to the deleveraging / bankruptcy cycle beginning with Terra/Luna’s demise (May 11), and the subsequent defaults from Three Arrows Capital, Celsius, BlockFi and more.

- October 2021: Give or take, this marked the all-time high for the majority of the market.

More than half of the tokens in our coverage universe are now comfortably above their pre-FTX levels. This includes most of the Top 50 by market cap, with a few exceptions (DOGE, ATOM, ALGO). And now, after ETH finally broke out of its slumber, roughly ¼ of the tokens in our coverage universe are trading higher than they were before Terra/Luna collapsed in May 2022. This is a much more difficult hurdle to overcome, given the amount of leverage in the system that was unwound during this time period. With 3 of the largest tokens in the market reclaiming this level, it’s a good sign for continued strength toward the ultimate goal of reclaiming all-time highs, which only a handful of tokens in the market have achieved.

Source: Top 20 by market capitalization and returns since various milestones / Messari

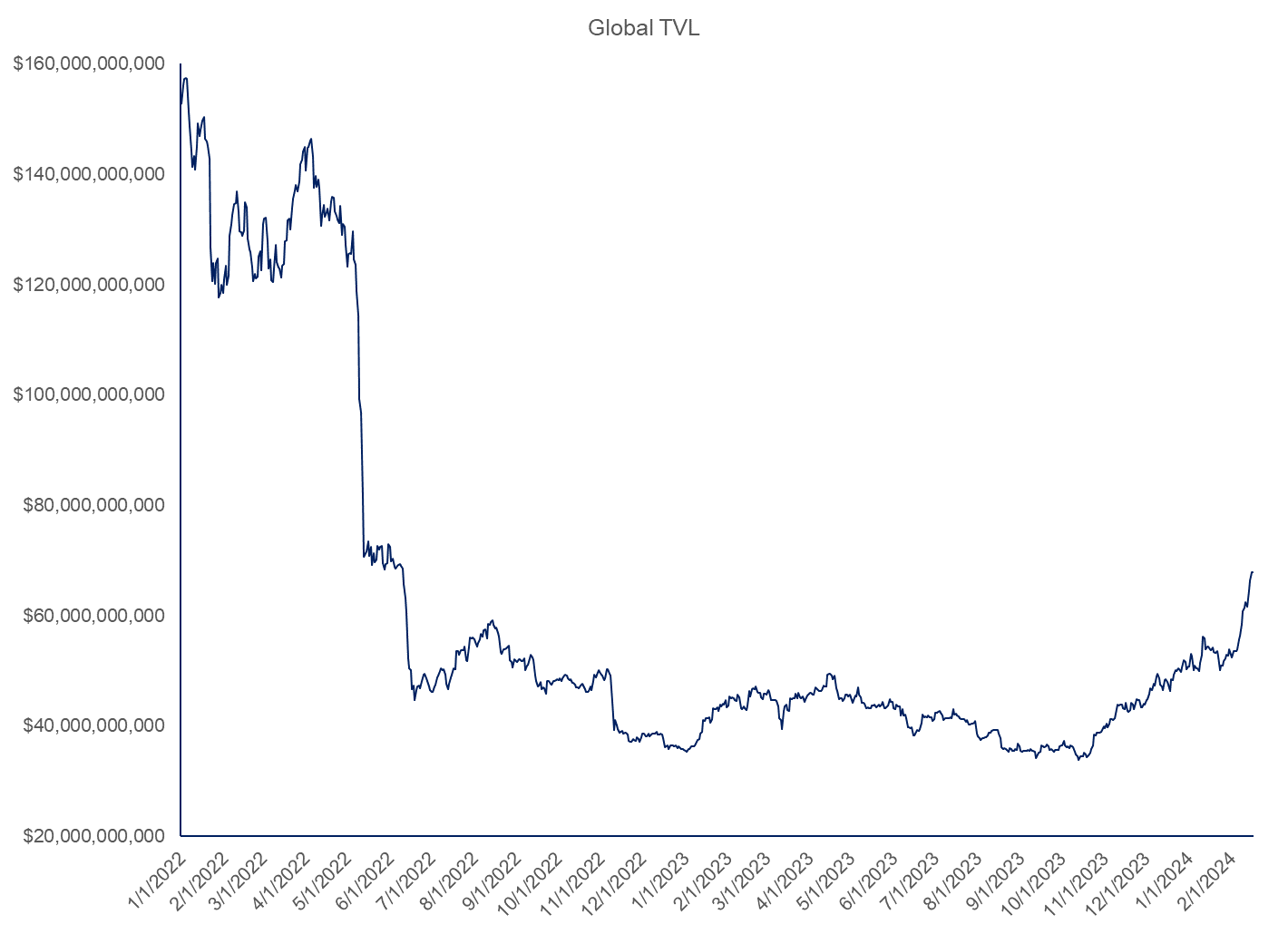

Since the beginning of February, total value locked (TVL) across all chains has started moving higher for the first time since 2021 (up $14.5 billion in the last 2 weeks). A portion of this can be explained by Eigenlayer, the primary re-staking project on Ethereum that enables the rehypothecation of staked Ether to secure other services, which saw its TVL increase from $1.1 billion to $4.3 billion after temporarily lifting deposit caps. However, the rest of the TVL growth has been more diversified. The biggest gainers in the last month in terms of chains have been Ethereum, Solana, and Sui, though the injection into Ethereum is moving the needle globally.

Source: Artemis & Arca Internal Data

While most eyes have been on price and the astounding success of the Bitcoin ETFs, it’s nice to see that other areas of the market are quietly growing as well.

The TradFi takeover

We spent a lot of time

talking about TradFi in our 2024 predictions, specifically that new TradFi entrants were going to focus on Bitcoin and crypto stocks, and that this is the last time you might be able to get unparalleled returns by investing in the rest of the digital assets market before Wall Street found their way into those as well.

We may have underestimated just how excited TradFi is and how little they could invest in besides Bitcoin and crypto stocks. TradFi investors are the new “degens”, pushing volatility and leverage to a whole new level.

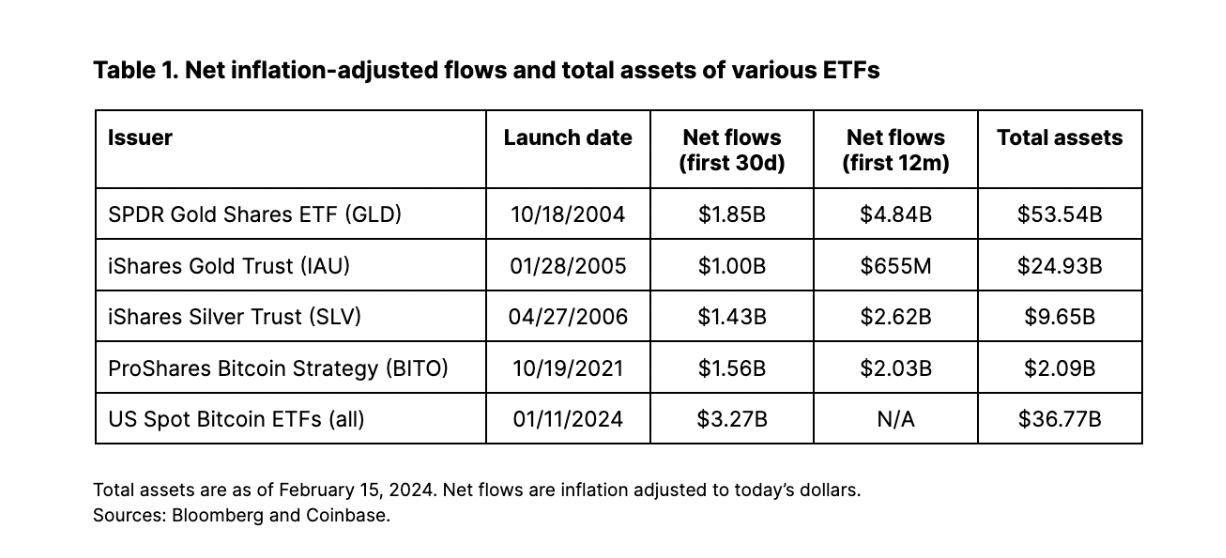

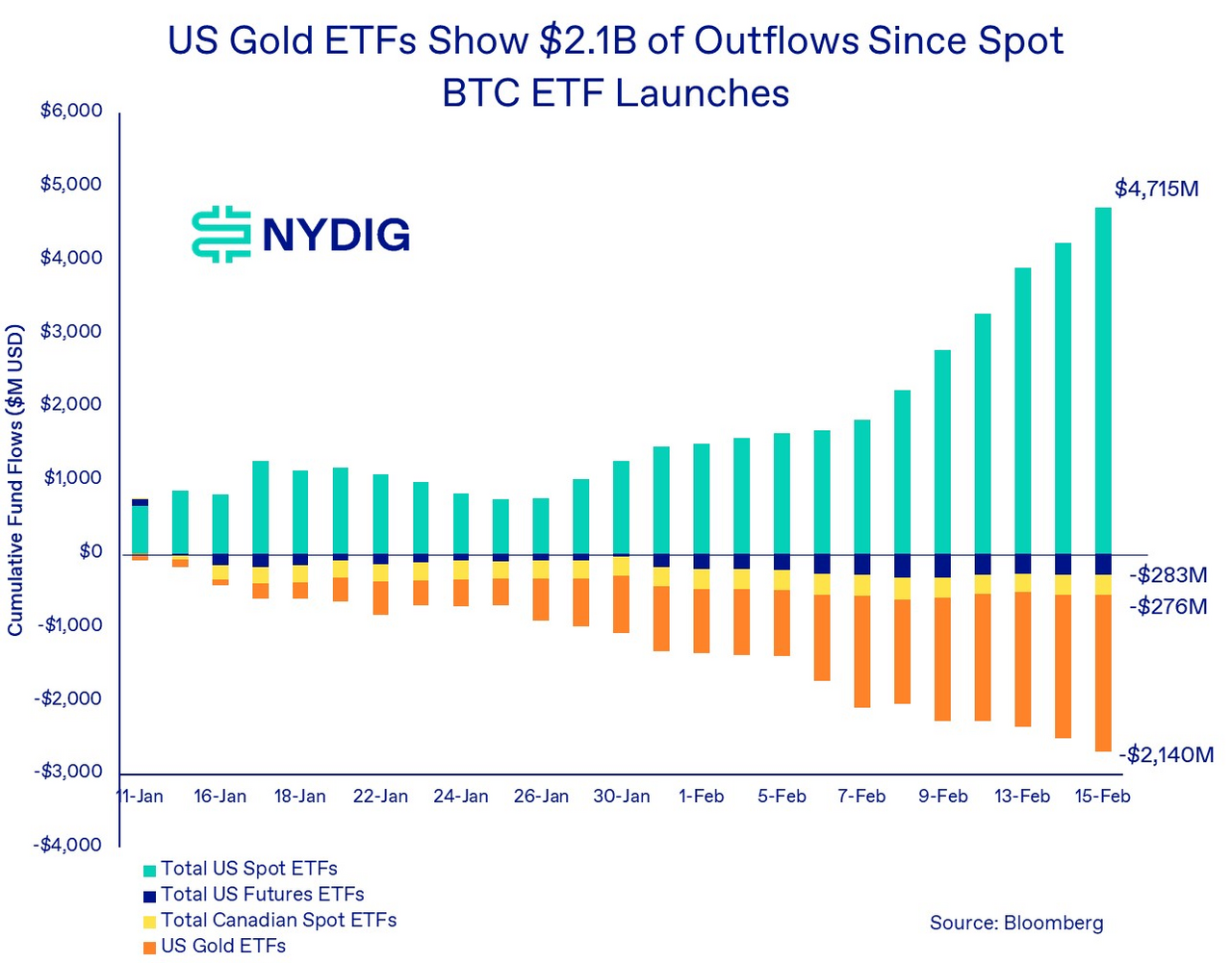

Let’s start with the new Bitcoin ETFs. Not only have the new Bitcoin spot ETFs dwarfed the launches of every other major ETF in terms of volumes and inflows, but they are also cannibalizing all other “inflation-protection” products. The new ETFs are accumulating roughly 10K BTC per day at the current rate, which is over 10x the amount of BTC mined in a given day (post-halving

in April, only 450 BTC will be mined per day so it will move to 20x). That’s a pretty huge demand/supply imbalance if it persists.

Source: NYDIG

Next, let’s look at the TradFi banks. On January 16th,

we wrote:

“Wall Street, to date, has been largely unable to profit off of blockchain’s growth and success. They write research, they trade a few crypto stocks here and there, and earn a few advisory fees on bankruptcies and IPOs, but for the most part have not been able to participate in the profits. The ETF is at least a step in the right direction in terms of focus and attention. And once they get a taste for the excitement and revenue potential, the real growth can begin.”

The new Bitcoin ETFs are only 1 month old, and Wall Street is already trying to

change the rules to participate in the profits. A coalition of bank trade groups called upon the SEC to overturn S.A.B. 121, a March 2022 guidance that effectively prohibits banks from holding crypto assets. Banks are being shut out of traditional ETF roles due to custody and holding rules and are asking the SEC to exclude ETFs from the broad crypto umbrella. They want a piece of the profits. Even the most sinister DAOs don’t try to change the rules this fast.

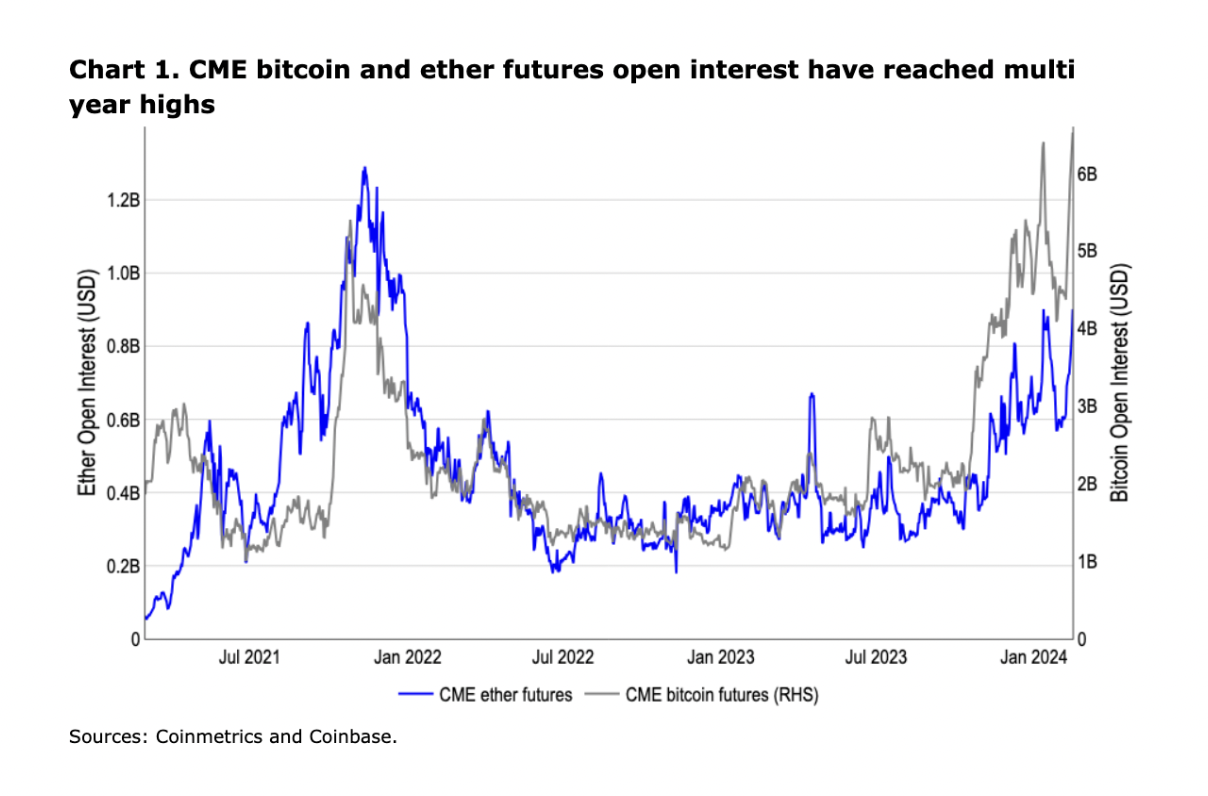

Meanwhile, there are still only a handful of ways for TradFi to invest directly in digital assets, and boy, are they. Open interest on Bitcoin and Ethereum Futures via the CME is back to levels not seen since 2021. Leverage is back, but this time, the “professionals” are pressing the envelope.

Meanwhile, Coinbase (COIN) and Bitcoin mining stocks (MARA, RIOT, CLSK, etc) have exhibited higher trading volumes and volatility this year than most digital assets. COIN alone has doubled, fallen 33%, and increased 50% in the last 3 months. That volatility would make even the most degenerate crypto trader blush. Wall Street can’t get enough of these stocks.

Source: TradingView

The pure amount of people and money in the traditional bank and brokerage system simply dwarfs anything that the digital assets market has experienced to date. Imagine when these TradFi degens with deeper pockets actually start trading tokens.